Surgical Sutures Market Research 2035

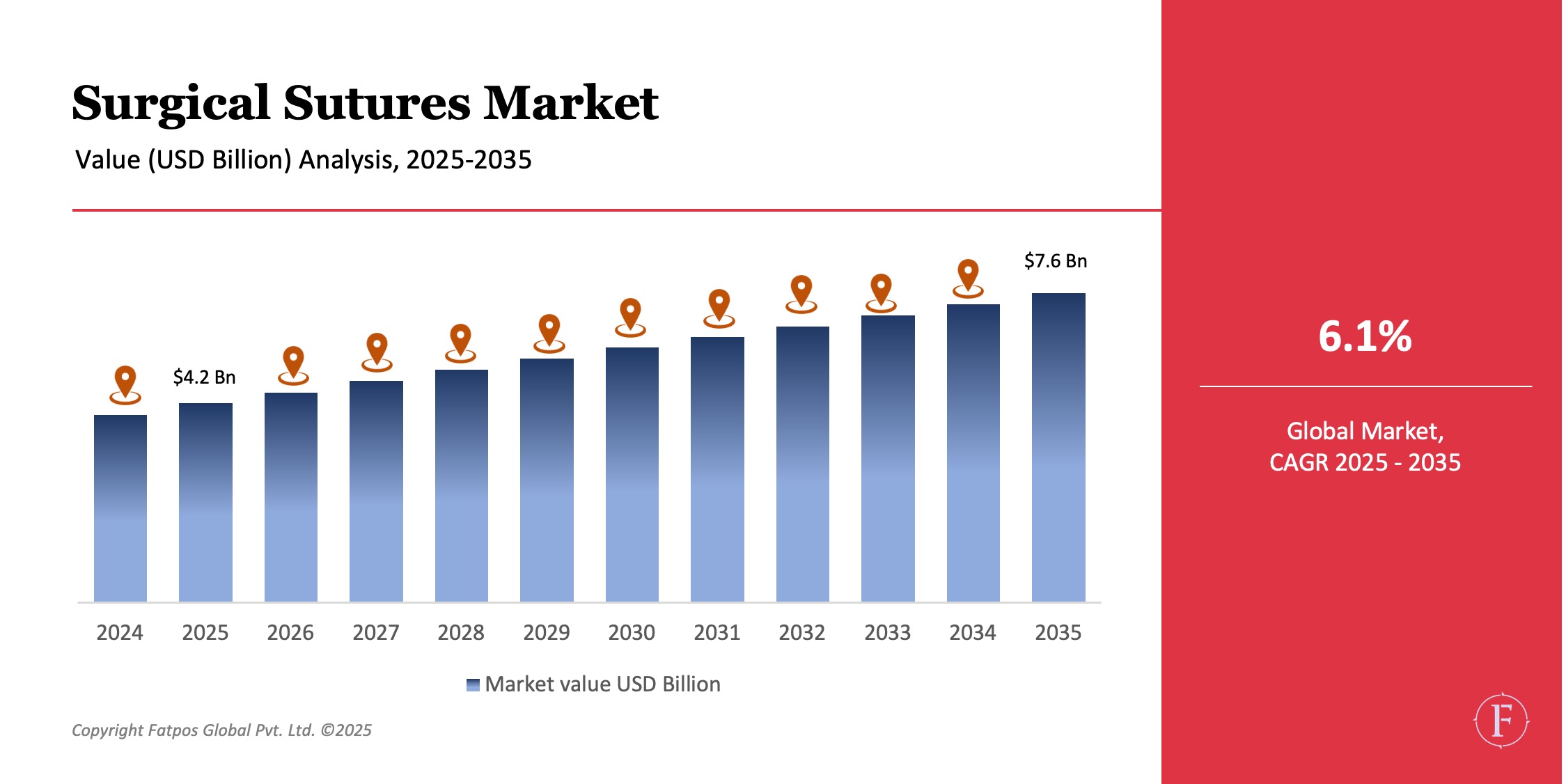

The Surgical Sutures Market Size was valued at USD 4.2 billion in 2025 and is projected to reach USD 7.6 billion by 2035, registering a CAGR of 6.1% during the forecast period. Market growth is primarily driven by the rising number of surgical procedures worldwide, increasing prevalence of chronic diseases, an expanding geriatric population, and continuous advancements in wound-closure technologies.

Surgical sutures are critical medical devices used to close surgical incisions and traumatic wounds, ensuring tissue approximation, proper healing, and reduced infection risk. Innovations in absorbable materials, antibacterial coatings, and filament designs are improving clinical outcomes and supporting sustained market expansion worldwide.

Product Overview

Surgical sutures remain a fundamental component of surgical care across all medical specialties. Despite the availability of alternative wound-closure products, sutures continue to be widely preferred due to their versatility, precision, and cost-effectiveness.

Absorbable sutures are increasingly used for internal tissue closure, eliminating removal requirements, while non-absorbable sutures remain critical for procedures requiring long-term wound support. The growing number of elective, emergency, and minimally invasive surgeries further strengthens market demand across hospitals and outpatient facilities.

Key Takeaways :

- Surgical Sutures Market expected to grow at ~6.1% CAGR through 2035

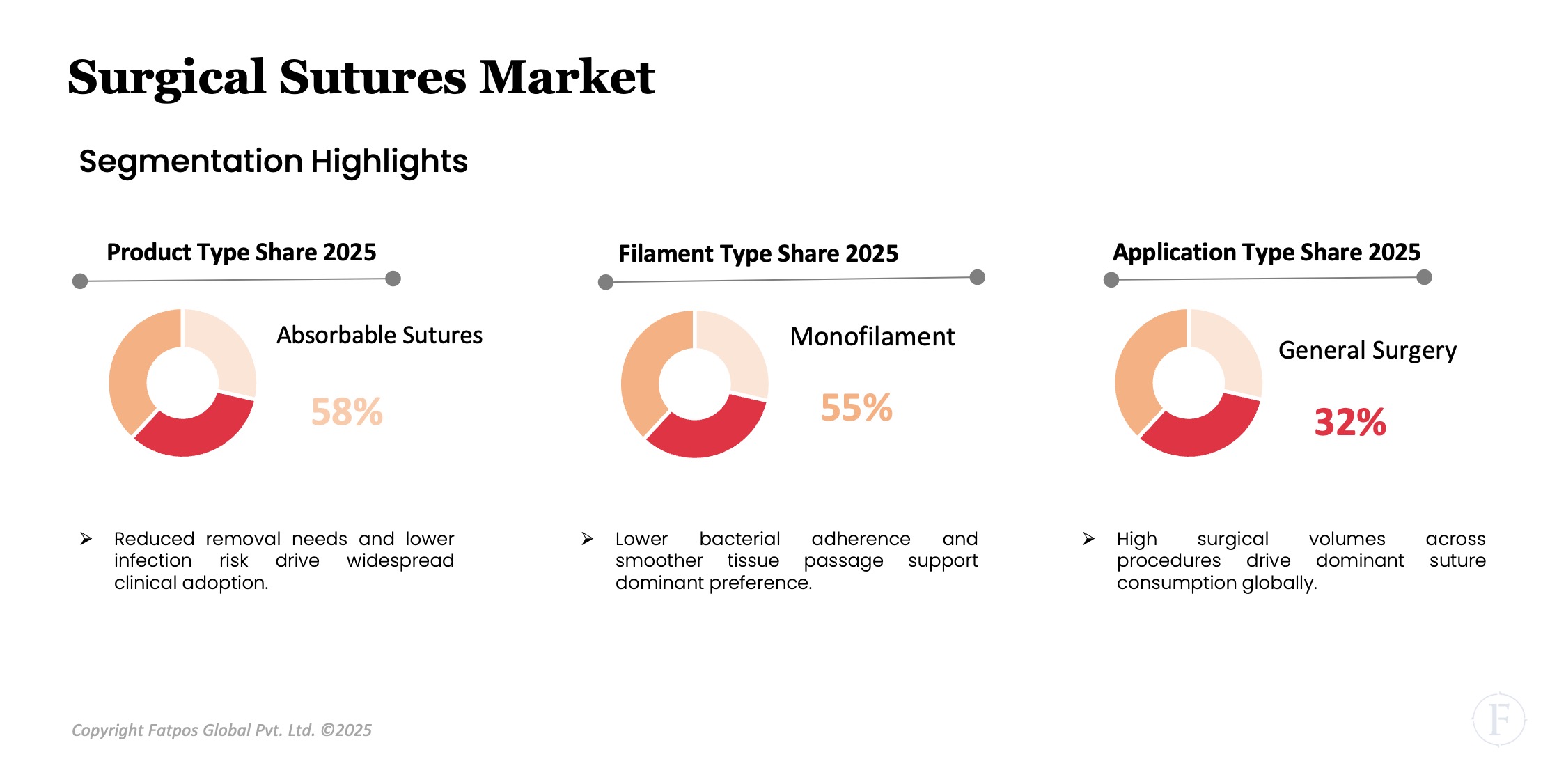

- Absorbable sutures dominate due to reduced post-operative complications

- General surgery represents the largest application segment

- Hospitals remain the primary end users globally

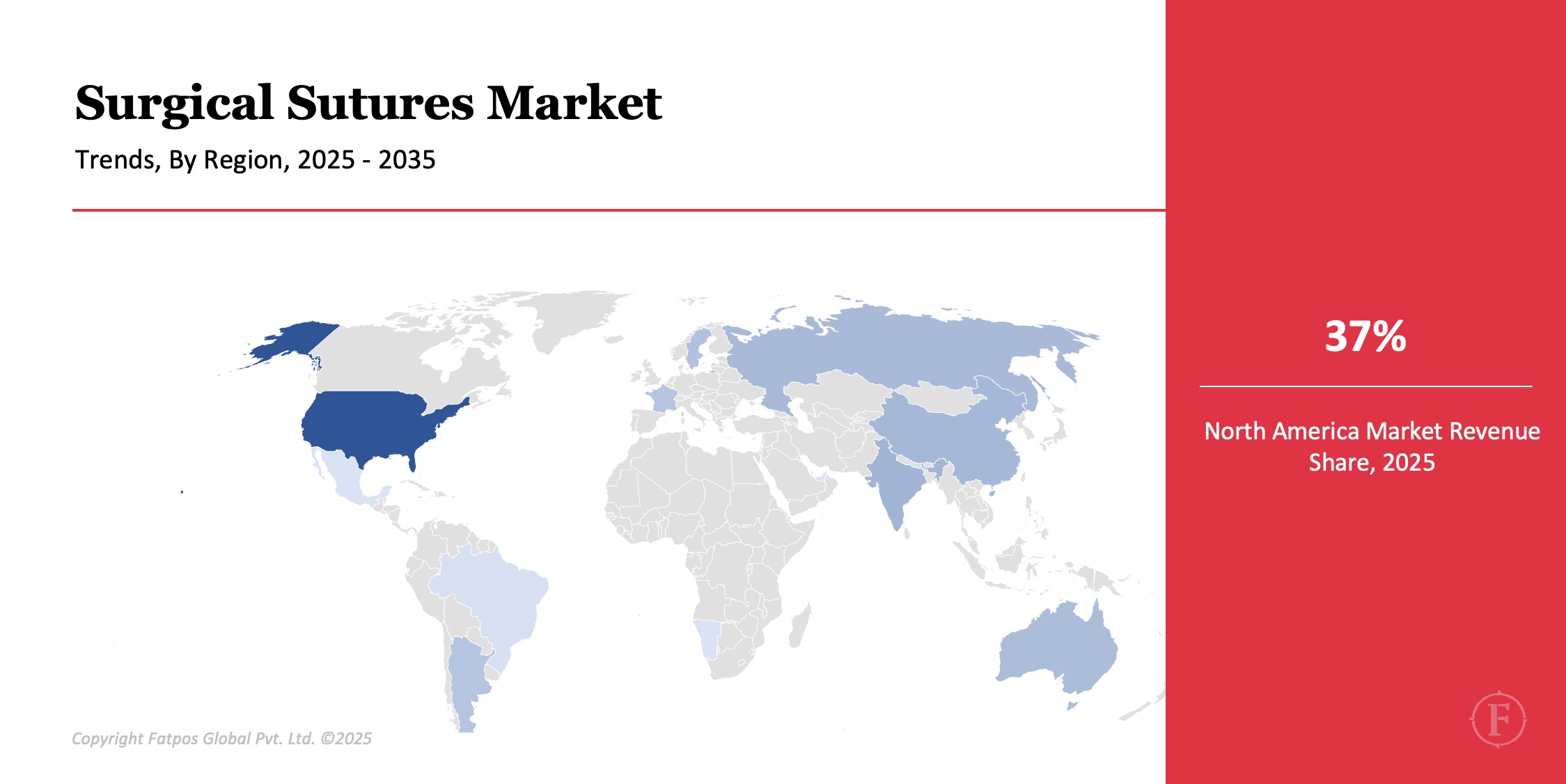

- North America leads market share, while Asia-Pacific shows fastest growth

- Innovation focuses on antibacterial, bioactive, and biodegradable sutures

Market Dynamics

Drivers

The surgical sutures market is driven primarily by the increasing volume of surgical procedures worldwide. Rising prevalence of chronic conditions such as cardiovascular diseases, diabetes, obesity, and orthopedic disorders has significantly increased surgical interventions. The growing aging population further contributes to higher demand for surgeries, particularly in developed economies.

Technological advancements in suture materials, including absorbable polymers and antimicrobial coatings, enhance wound healing and reduce infection risks. Expansion of healthcare infrastructure, improved access to surgical care in emerging economies, and the growing adoption of minimally invasive surgeries collectively support sustained global market growth.

Restrictions

Despite steady demand, the market faces restraints from the growing adoption of alternative wound-closure solutions such as surgical staplers, tissue adhesives, and sealants, which offer faster closure times. Risks associated with improper suturing techniques and surgical site infections may limit adoption in certain procedures. Cost constraints within healthcare systems, particularly in developing regions, restrict the use of advanced or premium sutures.

Additionally, stringent regulatory requirements and lengthy product approval processes slow new product launches. Price sensitivity among hospitals and clinics further restricts widespread adoption of technologically advanced sutures.

Opportunities

Significant growth opportunities exist through the development of advanced absorbable sutures, antibacterial coatings, and bioactive materials that accelerate wound healing. Rising demand for cosmetic, laparoscopic, and minimally invasive surgeries creates opportunities for fine, precision-engineered sutures.

Emerging economies with expanding healthcare infrastructure and increasing surgical access present strong growth potential. Growth in medical tourism and ambulatory surgical centers further boosts demand. Future innovations such as smart sutures with drug-delivery and infection-monitoring capabilities offer promising long-term opportunities for market players.

Challenges

The surgical sutures market faces challenges related to maintaining consistent quality, safety, and performance across diverse surgical applications. Ensuring effective infection control while improving tensile strength and biodegradability remains technically complex. Supply chain disruptions and fluctuating raw material costs can impact production efficiency.

Additionally, training healthcare professionals to adopt advanced suturing techniques is essential for optimal outcomes. Competition from alternative wound-closure technologies and pressure to reduce healthcare costs further challenge market growth, requiring continuous innovation and cost optimization by manufacturers.

Surgical Sutures Market Trends

The market is witnessing a strong shift toward absorbable and antibacterial sutures to reduce infection risks and post-surgical complications. Monofilament sutures are increasingly preferred in critical procedures due to improved tissue compatibility. Rising adoption of minimally invasive surgeries is driving demand for finer, high-precision sutures. Sustainability trends are encouraging the use of biodegradable and eco-friendly materials.

Additionally, digital surgical training tools and simulation technologies are improving suturing accuracy and clinical outcomes across hospitals and outpatient facilities.

Key Players in the Global Surgical Sutures Industry

- Johnson & Johnson (Ethicon)

- Medtronic

- Braun Melsungen AG

- Smith & Nephew

- Teleflex Incorporated

- Sutures India Pvt. Ltd.

- Peters Surgical

- Integra LifeSciences

- Conmed Corporation

- Halyard Health

Regional & Country Analysis

North America dominates the surgical sutures market due to advanced healthcare infrastructure, high surgical volumes, and strong adoption of innovative medical devices. Europe follows, supported by rising geriatric population and increasing elective surgeries.

Asia-Pacific is the fastest-growing region, driven by expanding healthcare access, growing medical tourism, and rising surgical procedures in countries such as China and India. Latin America and the Middle East & Africa present emerging opportunities due to improving healthcare systems and increasing investments in surgical facilities.

Segmentation Highlights

By product type, absorbable sutures account for the largest share due to reduced removal requirements and lower infection risks. By filament type, monofilament sutures dominate owing to smooth tissue passage and reduced bacterial adhesion. By application, general surgery leads due to high procedure volumes across hospitals. By end user, hospitals represent the largest segment due to advanced surgical infrastructure and skilled professionals. Regionally, North America holds the highest market share, while Asia-Pacific shows the fastest growth rate.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 7.6 Billion |

|

Market CAGR |

6.1% |

|

By Product Type |

Absorbable Sutures, Non-Absorbable Sutures |

|

By Filament Type |

Monofilament, Multifilament |

|

By Application |

Cardiovascular, Orthopedic, General Surgery, Gynecology, Ophthalmic, Others |

|

By End User |

Hospitals, Ambulatory Surgical Centers, Clinics |

|

By Region |

North America, Europe, Asia-Pacific, Latin America, MEA |

|

Surgical Sutures Market: Key Players |

Johnson & Johnson (Ethicon), Medtronic, B. Braun Melsungen AG, Smith & Nephew, Teleflex Incorporated |

Global Surgical Sutures Industry Instances

- Hospitals increased absorbable suture adoption to reduce post-surgical complications

- Manufacturers launched antibacterial sutures to lower infection risks

- Ambulatory surgical centers expanded outpatient procedures using advanced sutures

- Emerging markets invested in surgical infrastructure boosting suture demand

Analyst Review

As per our Surgical Sutures Market analysis, the market is poised for steady growth through 2035, supported by rising surgical volumes and continuous technological innovation. While competition from alternative wound-closure solutions persists, sutures remain indispensable across surgical disciplines. Companies focusing on advanced materials, infection prevention, and cost-effective solutions are expected to strengthen their market position globally.

Frequently Asked Questions (FAQ):

Surgical sutures are medical devices used to close wounds or surgical incisions, supporting tissue healing and reducing post-operative infection risks across various medical procedures.

Growth is driven by increasing surgical procedures, aging populations, rising chronic diseases, expanding healthcare infrastructure, and continuous advancements in suture materials and technologies.

Absorbable sutures dominate due to convenience, reduced need for removal, lower infection risks, and improved patient recovery outcomes.

Key trends include rising adoption of antibacterial sutures, preference for monofilament sutures, growth in minimally invasive surgeries, and development of biodegradable materials.

North America leads due to advanced healthcare systems, high surgical volumes, and strong adoption of innovative medical devices.

Select License Type

Select License Type