Cancer Diagnostics Market Research 2035

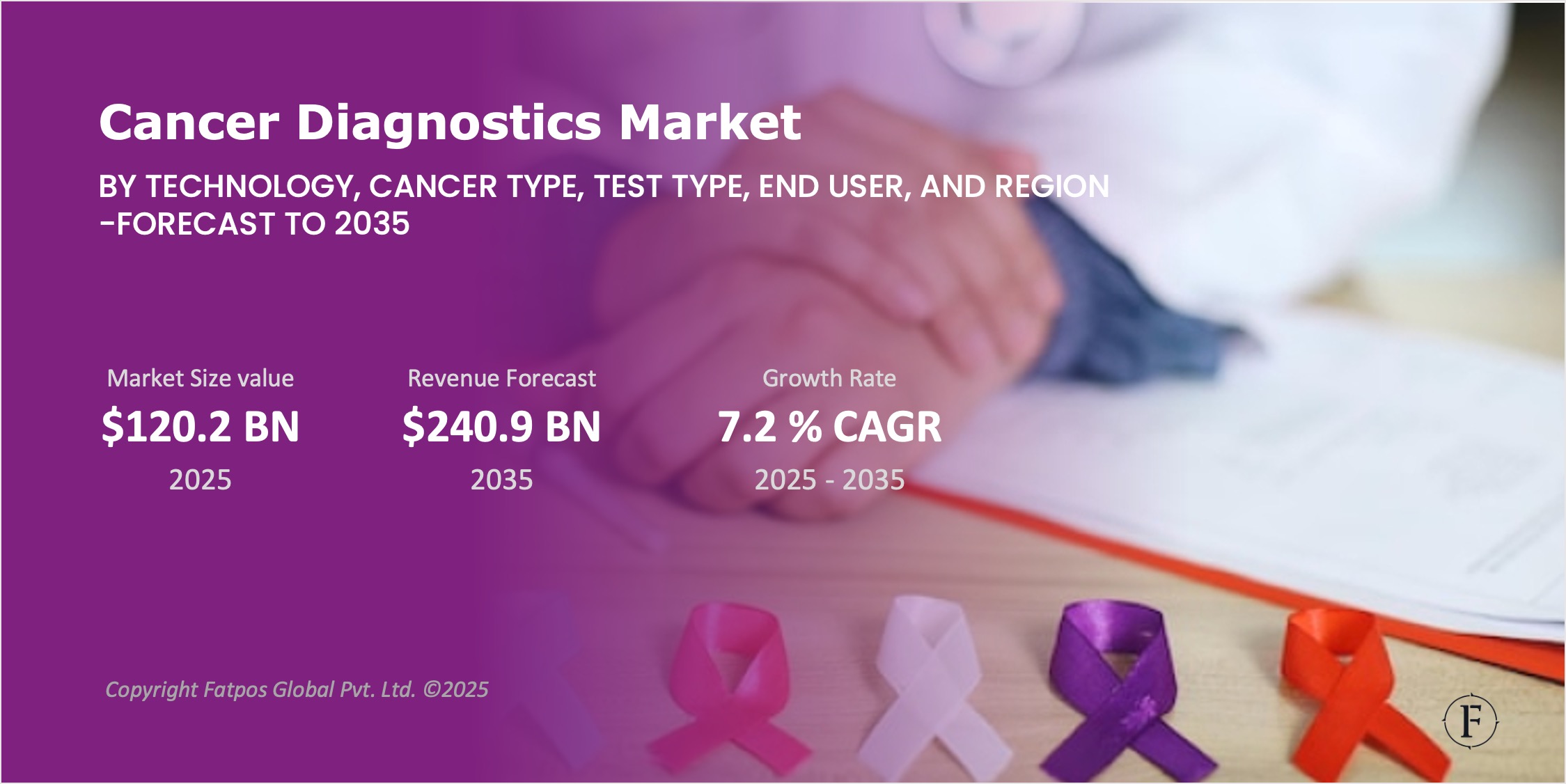

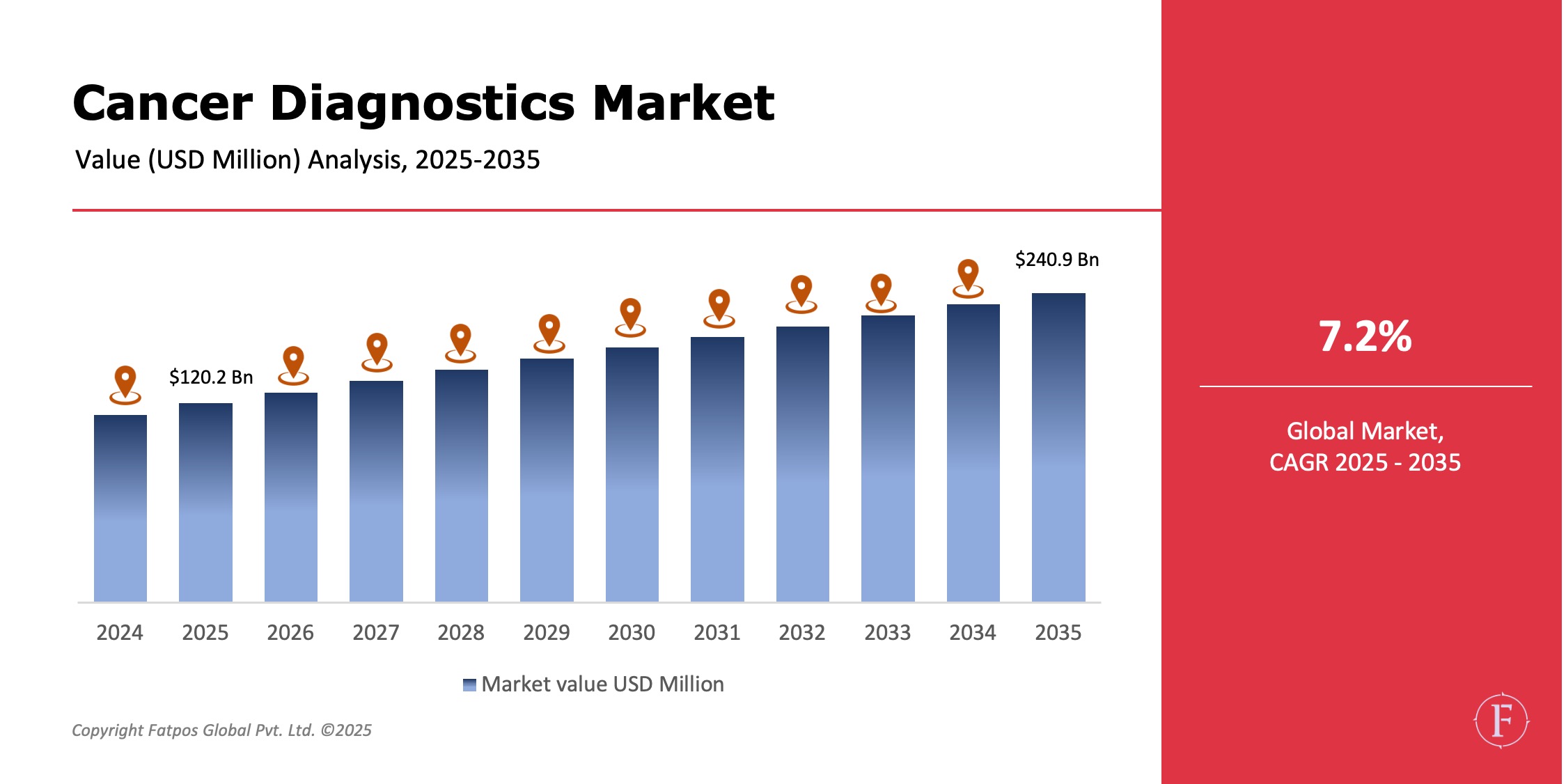

The Global Cancer Diagnostics Market Size was USD 120.2 billion in 2025 and is projected to reach USD 240.9 billion by 2035, registering a CAGR of 7.2%, The market demand arises from rising worldwide cancer incidence, early detection awareness, and advances in molecular assays, imaging, NGS, liquid biopsies, AI analytics and multiplex biomarkers. These technologies enable precise early diagnosis, staging, treatment planning and monitoring, boosting survival rates and cutting costs amid expanding healthcare infrastructure and funding for screening programs.

Product Overview

Cancer diagnostics span imaging (MRI, CT, PET, ultrasound, mammography), molecular tests (PCR, RT-PCR, NGS, FISH, microarray), tissue histopathology via biopsy, biomarker assays (BRCA, PSA), and companion diagnostics for targeted therapies. AI and machine learning integration boosts sensitivity, specificity and throughput, while digital pathology and tele-diagnostics enhance access in remote areas.

AI and machine learning integration dramatically enhances performance: convolutional neural networks detect lung nodules on CT with 95%+ sensitivity, while digital pathology platforms enable whole-slide AI analysis exceeding human pathologists in speed and concordance. Tele-diagnostics and cloud-based platforms democratize access, transmitting slides from rural clinics to expert centers for real-time consultation.

Key Takeaways :

- Cancer diagnostics market projected to grow at ~7.2% CAGR through 2035.

- Molecular diagnostics and imaging modalities lead in adoption due to high accuracy and clinical utility.

- Growing screening and early detection programs boost market demand.

- AI-assisted diagnostics and liquid biopsy are high-growth innovation segments.

- High cancer burden in aging populations drives demand globally.

- Hospitals and diagnostic laboratories remain primary end users.

Market Dynamics

Drivers

Rising global cancer incidence, particularly lung, breast and colorectal types, alongside early screening initiatives and healthcare expansion in developing regions, propel demand. Technological advances in NGS, liquid biopsy and digital pathology support personalized medicine and companion diagnostics for targeted therapies.

Restrictions

High costs of advanced diagnostic tests and equipment limit widespread adoption. Regulatory hurdles and reimbursement constraints in various regions slow market penetration. Limited access to high-end diagnostics persists in low-income areas, hindering early detection efforts.

Opportunities

AI and machine learning enhance image and pathology analytics for greater accuracy. Liquid biopsy and non-invasive tests expand early detection and monitoring capabilities. Tele-diagnostics and remote screening platforms improve access in underserved areas. Public health initiatives and screening programs drive broader adoption.

Challenges

Standardized global guidelines and regulatory harmonization are needed for consistent diagnostic practices. Integrating multi-omics data remains essential for comprehensive diagnostics. Managing data privacy and interoperability across systems poses ongoing hurdles.

Cancer Diagnostics Market Trends

Strong growth in liquid biopsy adoption enables non-invasive early cancer detection and recurrence monitoring through circulating tumor DNA analysis. AI-based image analysis is increasingly applied in radiology and pathology to improve diagnostic speed and accuracy. Multiplex biomarker testing platforms allow simultaneous detection of multiple markers for better precision. Companion diagnostics expand alongside precision oncology drugs, guiding personalized treatment selection. Outsourcing to specialized labs rises as healthcare providers seek expertise and cost efficiencies.

Key Players in the Global Cancer Diagnostics Industry

- Roche Diagnostics

- Abbott Laboratories

- Thermo Fisher Scientific

- Q2 Solutions / Quest Diagnostics

- Siemens Healthineers

- GE Healthcare

- Danaher (Cepheid, Leica Biosystems)

- F. Hoffmann-La Roche Ltd

- Bio-Rad Laboratories

- Hologic, Inc.

- Illumina, Inc.

- Guardant Health

- Exact Sciences Corporation

- Myriad Genetics

- Laboratory Corporation of America (Labcorp)

Regional & Country Analysis

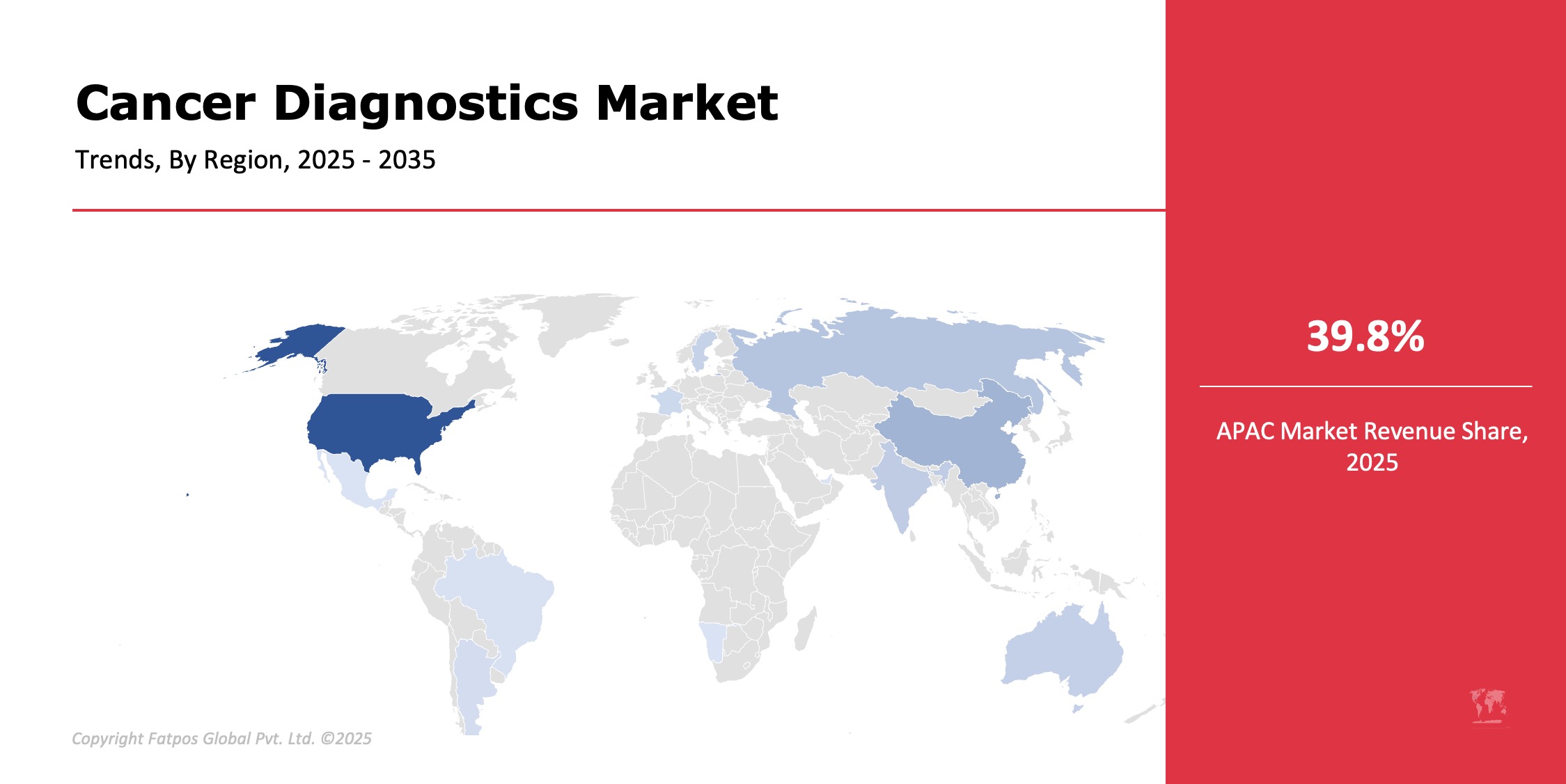

North America commands the largest cancer diagnostics market share, fueled by advanced infrastructure, innovative adoption, robust US/Canada screening and favorable reimbursements. Europe sees strong demand from public health initiatives, aging demographics and specialized tests, led by Western Europe. Asia-Pacific grows fastest amid rising cancer cases, healthcare expansion and government spending in China and India. Latin America advances via awareness and system improvements despite economic gaps, while Middle East & Africa shows early potential through infrastructure investments and disease awareness.

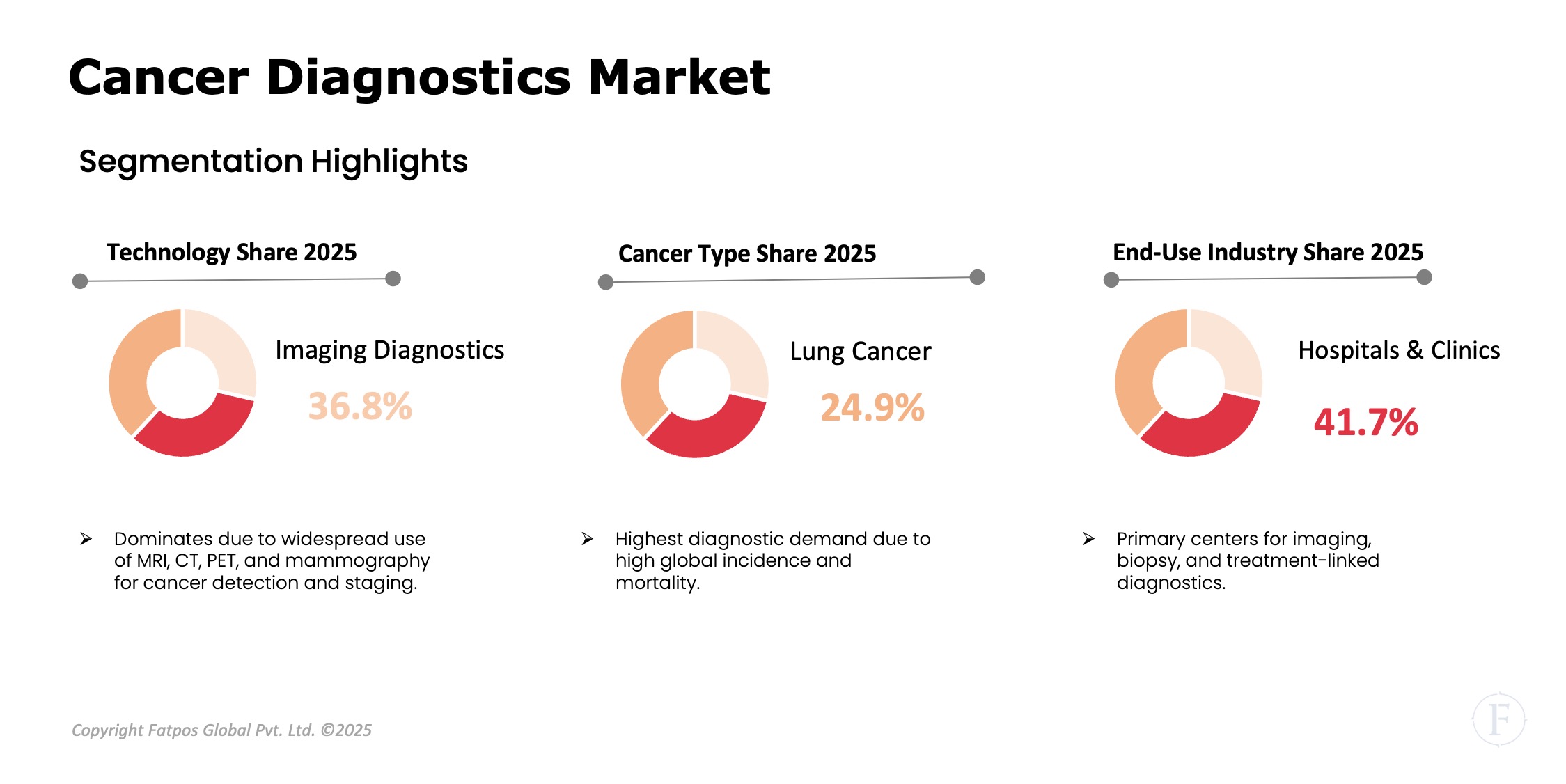

Segmentation Highlights

Molecular diagnostics and imaging technologies lead the cancer diagnostics market due to their essential clinical value and ongoing advances in precision, sensitivity and processing speed. NGS provides detailed genomic profiling to pinpoint actionable mutations guiding targeted therapies, while innovations like low-dose CT for lung screening and contrast-enhanced MRI excel in early lesion detection.

Lung, breast and colorectal cancers account for the largest diagnostic volumes with proven screening methods. Low-dose CT cuts lung cancer mortality by 20% among high-risk smokers, mammography detects 85–90% of breast tumors larger than 1 cm, and colonoscopy identifies over 95% of colorectal polyps.

Hospitals and independent diagnostic labs handle most routine screening, staging and monitoring needs. Academic centers and research institutions pioneer advanced platforms for clinical trials, multi-omics analysis and biomarker development, validating innovations before widespread commercial use.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Cancer Diagnostics Market Forecast Period |

2025–2035 |

|

Cancer Diagnostics Market Size by 2035 |

USD 240.9 billion |

|

Market CAGR |

7.2% |

| By Technology | Imaging Diagnostics, Molecular Diagnostics, Tissue Diagnostics/Histopathology, Biomarker Testing, Companion Diagnostics |

|

By Cancer Type |

Lung, Breast, Colorectal, Prostate, Cervical, Ovarian, Liver & Pancreatic, Others) |

|

By Test Type |

Screening, Early Detection, Prognosis/Monitoring |

|

By End User |

Hospitals & Clinics, Diagnostic Laboratories, Cancer Research Institutes, Ambulatory Care Centers, Academic & Research Organizations |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Key Market Players |

Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Q2 Solutions/Quest Diagnostics, Siemens Healthineers, GE Healthcare |

Global Cancer Diagnostics Industry Instances

- A major oncology center adopted NGS-based panels for broad genomic profiling of solid tumors.

- Multiple hospitals implemented AI-assisted mammography to improve breast cancer screening sensitivity.

- Laboratories expanded liquid biopsy services to monitor recurrence in metastatic cancer patients.

- Diagnostic networks deployed digital pathology platforms to accelerate remote slide analysis.

Analyst Review

As per our Cancer Diagnostics Market analysis report, market is continues to expand with strong demand for early detection, personalized treatment pathways, and real-time monitoring. Technological innovation—especially in molecular diagnostics, AI analytics, and non-invasive testing—is reshaping clinical pathways and improving patient outcomes. While cost and access disparities present challenges, coordinated healthcare investments and public health initiatives are expected to sustain robust long-term growth.

Frequently Asked Questions (FAQ):

The market is expected to reach approximately USD 240.9 billion by 2035.

Molecular diagnostics and imaging diagnostics dominate due to their clinical accuracy and broad applicability.

Lung, breast, and colorectal cancers account for the largest diagnostic demand due to high prevalence.

Hospitals and diagnostic laboratories represent the largest share, followed by cancer research institutes.

Asia-Pacific is the fastest-growing market, driven by expanding healthcare access and rising disease burden.

Select License Type

Select License Type