Satellite Payload Market Research, 2035

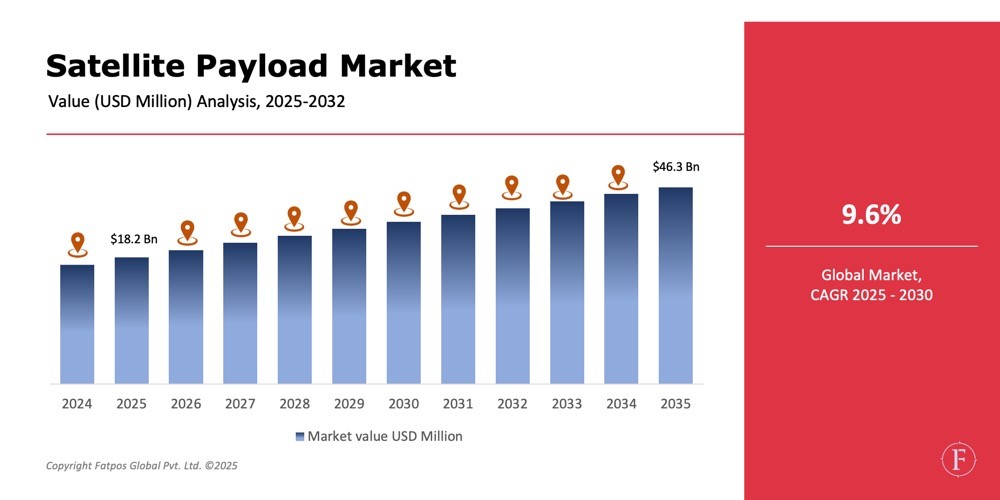

The global Satellite Payload Market was valued at USD 18.2 billion in 2025 and is projected to reach USD 46.3 billion by 2035, exhibiting a CAGR of 9.6% from 2025–2035. Market expansion is driven by the surge in broadband connectivity demand, Earth observation missions, defense modernization, satellite-based IoT, and lower-cost space access enabled by reusable launch systems. Satellite operators increasingly adopt flexible, software-defined payloads, bringing new capabilities in capacity allocation, beam-forming, network routing, and frequency management.

Large commercial constellation programs in telecom, navigation, weather forecasting, climate analytics, military ISR, and remote sensing further accelerate adoption. As NewSpace startups, national agencies, and private telecom operators push persistent global coverage and low-latency communications, the satellite payload industry is entering its strongest investment phase in two decades.

Product Overview

A satellite payload is the functional equipment carried onboard a spacecraft that performs mission objectives such as communication, Earth imaging, navigation, sensing, or science experimentation. Payloads include transponders, cameras, onboard processors, sensors, power modules, phased-array antennas, frequency converters, and data handling subsystems.

Payload innovation is rapidly transitioning from traditional fixed GEO communication systems to software-defined, reconfigurable, multi-band LEO payload architectures. New technologies enable in-orbit switching, quantum encryption, intelligent data routing, onboard AI processing, and laser inter-satellite links for ultra-fast transmission. Payloads today serve major applications, including broadband connectivity, television, defense surveillance, maritime monitoring, environmental intelligence, precision agriculture, climate tracking, aviation, and national security.

As commercial constellation economics improve, satellite payloads are increasingly integrated into small and medium satellite classes, reducing cost per bit, mission lifecycle, and deployment time compared to traditional GEO platforms.

Key Takeaways(in bullets)

- LEO dominates global deployments, driven by mega-constellations for broadband and Earth imaging.

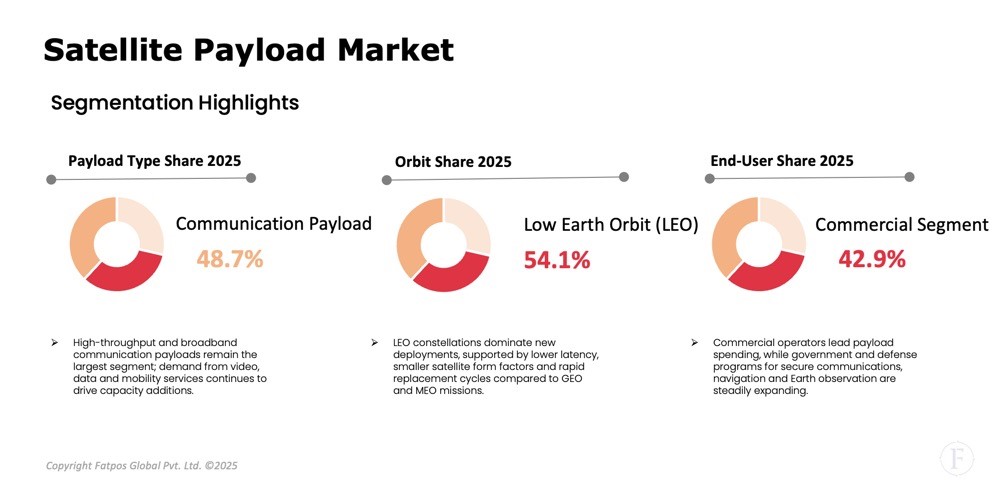

- Communication payloads hold the highest global satellite payload market share, followed by Earth observation and navigation missions.

- Small satellites and CubeSat payloads show the fastest growth, supported by shortened development cycles, lower launch costs, and rapid constellation refresh.

- Ka-Band and Ku-Band payloads are expanding due to high-throughput mobility, aviation connectivity, inflight broadband, and multi-spot beam architectures.

- Government and defense agencies remain major buyers, but commercial operators are scaling fastest due to connectivity demand.

Market Dynamics

Drivers

The Satellite Payload Market is propelled by environmental regulations, net-zero goals in Europe and North America, and the shift to renewables amid rising fossil fuel costs, positioning it as a key player in energy transition. With organic waste abundance from agriculture and municipalities, biomethane supports circular economies, backed by incentives in the EU, U.S., and China that enhance production scalability. The market, valued around USD 9-15 billion in 2025, expects 7-14% CAGR through 2035 driven by these factors.

Restraints

The satellite payload market is expanding as demand rises for broadband connectivity, defense surveillance, weather and climate monitoring, and global IoT coverage. Reusable launch vehicles and miniaturized electronics are lowering costs and enabling large constellations. Advanced payload technologies—high‑throughput architectures, multi‑band antennas, onboard processing, phased arrays, and laser links—boost capacity and flexibility, while government space programs and connectivity needs in maritime, aviation, and autonomous transport underpin strong growth prospects through 2035.

Opportunities

Satellite payload innovation is opening new revenue streams through software‑defined transponders, multi‑band RF systems, laser optical links, and onboard AI that cuts latency and ground‑processing needs. Faster constellation refresh enables frequent capability upgrades, while data‑as‑a‑service models in earth observation, IoT, mobility, and defense ISR grow alongside national security, quantum encryption, and space‑situational‑awareness payload demand.

Challenges

Cybersecurity, encryption standardization, in-orbit redundancy, debris collision risk, and radiation hardening remain persistent payload design challenges. Regulatory approval for frequency allocation, cross-border imaging rules, and dual-use technology controls limit adoption speed. Thermal management, payload miniaturization, and space-qualified semiconductor supply constraints impact mission reliability and cost competitiveness

Satellite Payload Market Trends

The Satellite Payload Market is poised for strong growth as NewSpace players deploy mega‑constellations with AI‑enhanced imaging and high‑throughput connectivity. Software‑defined payloads and laser links are reshaping bandwidth economics, while Earth observation supports climate intelligence, risk analytics, and smart agriculture. Small‑satellite payloads dominate demand through 2035, offering low costs, rapid refresh, and scalable capacity for telecom, EO, and industrial IoT.

Key Players Featured in the Report

The global satellite payload market analysis includes several leading manufacturers, such as:

- Lockheed Martin

- Airbus Defence & Space

- Thales Alenia Space

- Northrop Grumman

- Honeywell International

- SpaceX (Starlink Payload Division)

- Surrey Satellite Technology Limited (SSTL)

- Raytheon Technologies

- L3Harris Technologies

- Boeing Satellite Systems

Regional Analysis

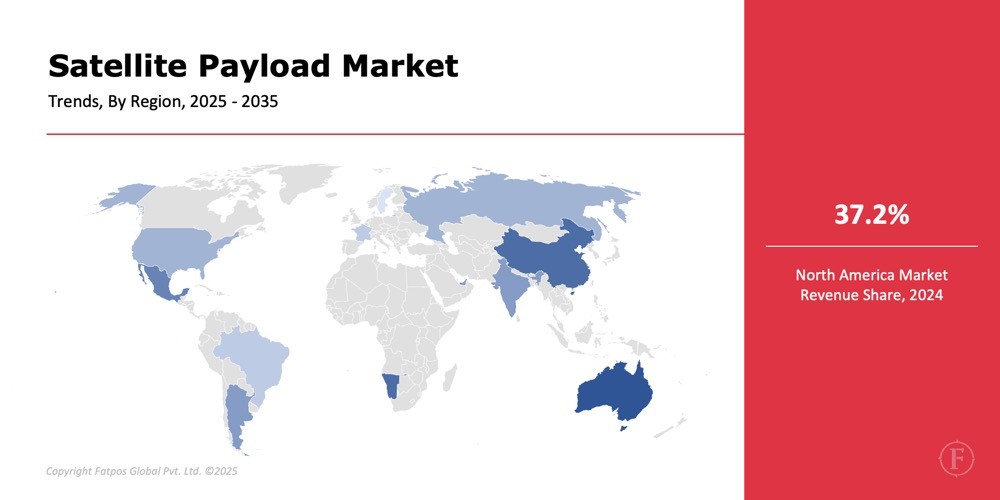

North America leads the satellite payload market, driven by defense spending, commercial LEO broadband networks, and advanced payload R&D funding. Europe follows with strong GEO and navigation programs, ESA funding, and Earth imaging missions.

Asia-Pacific records the fastest CAGR, led by China, India, Japan, and emerging ASEAN defense modernization and national space programs. Latin America, Middle East, and Africa are expanding steadily via telecom connectivity, maritime tracking, energy exploration, and environmental monitoring payload deployments.

Segmentation Analysis

- Communication payloads dominate, supported by broadband connectivity, high-throughput satellites, aviation mobility, and maritime data services.

- LEO orbit segment is fastest growing, enabling real-time global coverage and reduced latency.

- Small satellite payloads expand rapidly, enabled by shorter mission cycles and strong commercial investment.

- Ka-Band and Ku-Band payloads remain the preferred frequency bands for mobility and data-intensive applications, while C-Band and X-Band continue to serve secure defense, aerospace, and remote sensing requirements.

Report Key Elements

|

Report Key Elements |

Details |

|

Study Period |

2025–2035 |

|

Satellite Payload Market Size 2035 |

USD 46.3 billion |

|

Market CAGR |

9.6% |

|

By Payload Type |

Communication, Navigation, Earth Observation, Scientific |

|

By Orbit |

LEO, MEO, GEO, HEO |

|

By Vehicle Type |

Small, Medium, Large Satellites |

|

By Frequency Band |

C-Band, X-Band, Ku-Band, Ka-Band |

|

By Region |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Satellite Payload Industry Instances ( in Bullets)

- SpaceX expands LEO payload capacity using laser cross-link architecture for inter-satellite networking.

- Airbus launches fully software-defined payloads supporting in-orbit bandwidth allocation and multi-beam flexibility.

- SSTL introduces miniaturized payloads for CubeSat imaging and climate analytics.

- L3Harris provides tactical ISR payloads for military communications and situational awareness.

Analyst Review

As per our Satellite Payload Market Analysis Study, the market is accelerating with strong investment momentum in commercial telecom, climate intelligence, navigation, and remote sensing. Payload miniaturization, reconfigurability, and onboard AI are redefining cost, performance, and mission scalability. As LEO networks scale globally, satellite payload economics will shift toward recurring service models including satellite-as-a-platform (SaaP), data subscriptions, analytics, and defense modernization contracts..

Frequently Asked Questions (FAQ):

The market is projected to grow from USD 18.2 billion in 2025 to USD 46.3 billion by 2035, at a CAGR of 9.6%, driven by broadband demand, defense programs, commercial LEO constellations, and miniaturized payload engineering.

North America leads due to strong defense spending, secure communications programs, and LEO broadband deployments from commercial operators.

Communication payloads remain the largest segment, while Earth observation and navigation payloads show strong multi-industry demand.

LEO deployments will expand fastest due to mega-constellations, real-time coverage, and low-latency telecom and sensing missions.

Satellite manufacturers, constellation operators, telecom companies, aerospace primes, launch providers, defense agencies, Earth analytics providers, utilities, agriculture analytics firms, insurers, and national space strategists evaluating investment, technology roadmaps, regulatory implications, and mission planning..

Select License Type

Select License Type