Aircraft Seating Market Research 2035

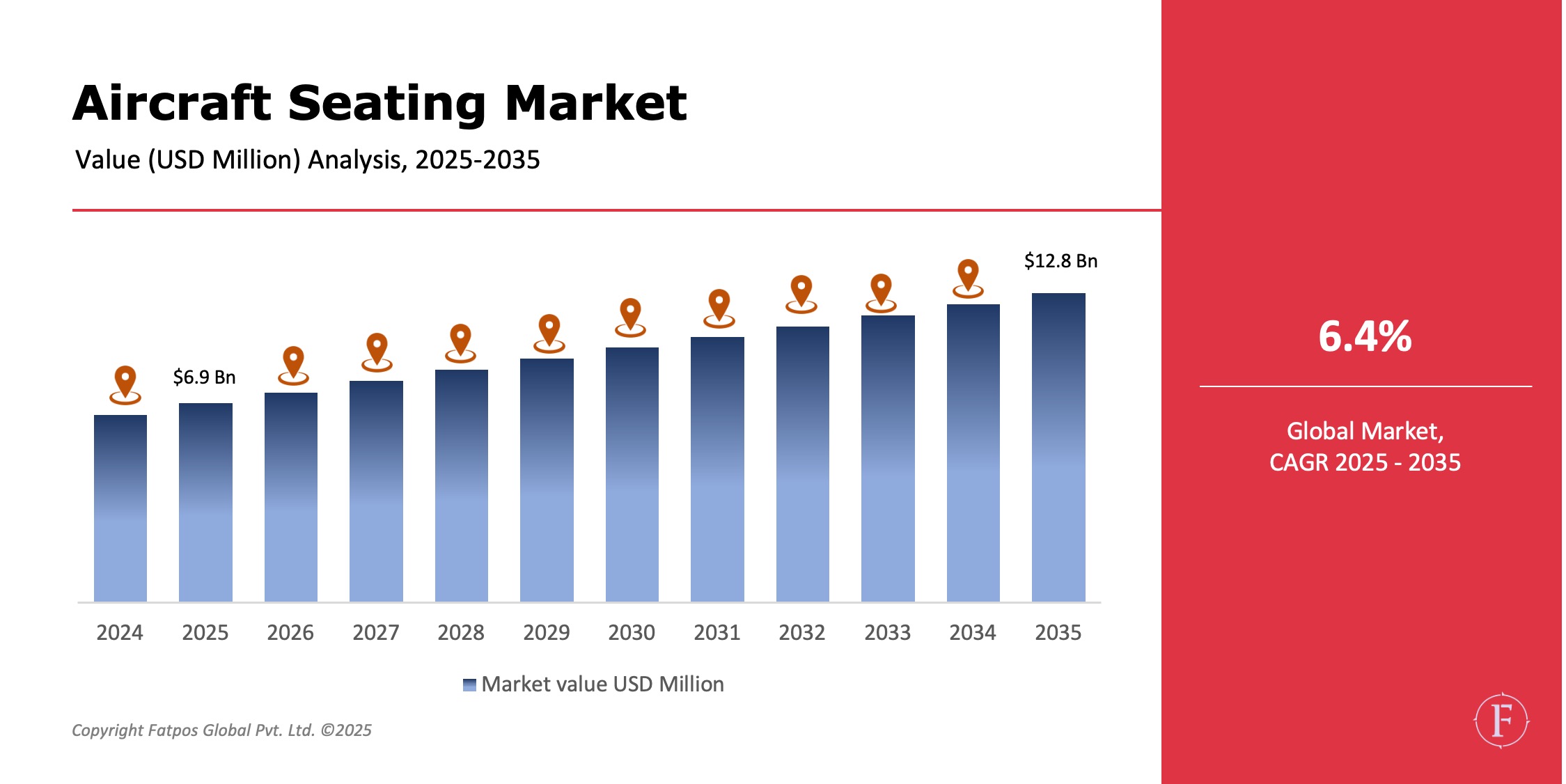

The Aircraft Seating Market Size was USD 6.9billion in 2025 and is projected to reach USD 12.8 billion by 2035, registering a CAGR of 6.4%. Market growth is propelled by emerging air passenger traffic, airline fleet growth, increased aircraft deliveries, and demand for lightweight, fuel-efficient seats that reduce operating costs and emissions. Passenger comfort drives innovations in ergonomic designs, modular systems, lightweight materials, and premium cabin upgrades, enabling airlines to differentiate offerings and enhance in-flight experiences amid competitive aviation dynamics.

Product Overview

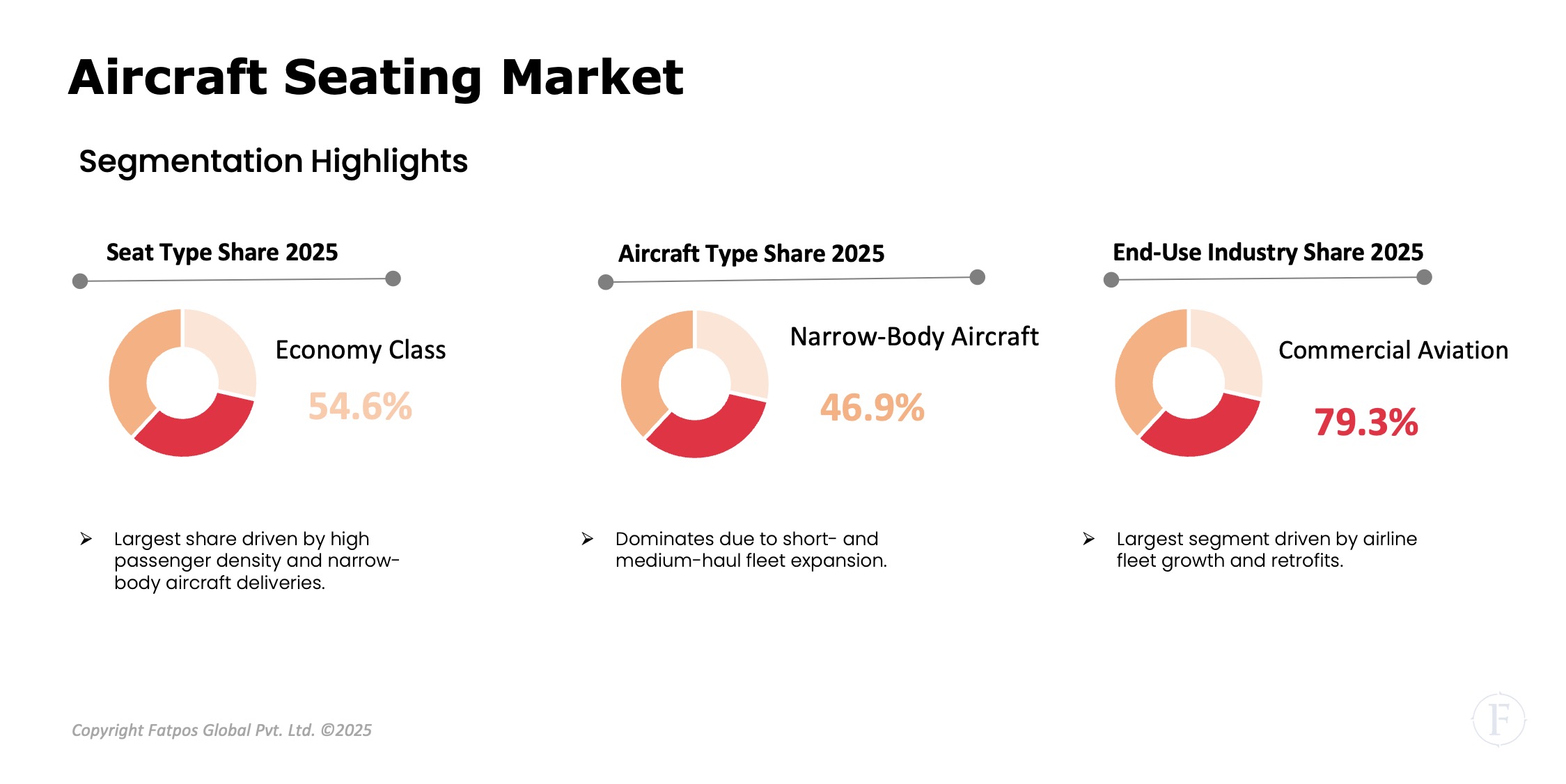

Aircraft Seating solutions balance stringent safety regulations with advancements in comfort, aesthetics, and operational efficiency to optimize airline performance. By seat type, economy class dominates volume due to high passenger density on mass-market flights; premium economy gains traction for affordable enhancements like extra legroom; business class prioritizes lie-flat beds, privacy suites, and connectivity; while first class, though low-volume, commands premium value through bespoke luxury and customization. By aircraft type, narrow-body jets lead owing to prolific short- and medium-haul operations; wide-body aircraft drive demand for multi-class premium layouts; regional jets serve feeder routes with compact designs; and business jets feature tailored, high-end seating for corporate travel.

Key Takeaways :

- The Aircraft Seating Market is expected to grow at ~6.3% CAGR through 2035.

- Economy class seating accounts for the largest market share by volume.

- Premium economy and business class segments are growing faster in value terms.

- Airlines increasingly focus on lightweight, modular, and slimline seats.

- Asia-Pacific is the fastest-growing regional market.

- Cabin retrofitting and seat replacement cycles drive recurring demand.

Market Dynamics

Drivers

Rising global air travel and passenger traffic growth fuels demand for expanded aircraft seating capacity amid booming international routes and leisure travel. Increasing aircraft production and fleet modernization programs by major OEMs drive retrofits and new deliveries with advanced seating systems. Demand for improved passenger comfort and cabin aesthetics spurs innovations like adjustable headrests, IFE integration, and stylish designs to boost satisfaction scores. Focus on reducing aircraft weight through lightweight composites and slimline seats enhances fuel efficiency and lowers emissions. Growth of low-cost carriers emphasizes durable economy solutions, while premium service differentiation elevates business and first-class offerings with luxury amenities.

Restrictions

High development and certification costs burden aircraft seating manufacturers, as designing compliant seats involves multimillion-dollar R&D, testing, and FAA/EASA approvals that span years. Stringent aviation safety and regulatory requirements enforce rigorous standards for fire resistance, crashworthiness, and durability, delaying launches and inflating expenses amid evolving rules. Long aircraft production and retrofit cycles exacerbate challenges, with OEM timelines stretching 5-10 years for new models and cabin upgrades, limiting agility and exposing firms to market shifts and supply chain disruptions.

Opportunities

Airlines are rapidly expanding premium economy seating to capture mid-tier demand, offering enhanced legroom, recline, and amenities between economy and business for profitable yield management. Adoption of advanced composite and lightweight materials like carbon fiber reduces seat weight by 15-20%, boosting fuel efficiency and range while meeting safety standards. Growth in cabin retrofits and aftermarket services emerges with aging fleets, enabling quick upgrades via modular designs for cost-effective refreshment. Increasing demand for customized business jet interiors emphasizes bespoke luxury, connectivity, and multifunctional spaces tailored to high-net-worth clients and corporate operators.

Challenges

Managing supply chain complexity approval and certification timelines challenges aircraft seating manufacturers, requiring robust vendor coordination for global sourcing of specialized materials while navigating prolonged FAA/EASA processes that delay market entry. Balancing comfort, durability, and weight reduction demands innovative engineering, such as integrating ergonomic padding with carbon composites to enhance passenger experience without compromising crash safety or adding mass. Cost pressures faced by airlines impact seat procurement, forcing suppliers to offer modular, value-engineered solutions amid fleet budget constraints and competition from low-cost carriers.

Aircraft Seating Market Trends

Rising adoption of slimline and lightweight seat designs reduces aircraft weight, improving fuel efficiency and enabling denser configurations without sacrificing basic comfort. Increased integration of in-flight entertainment and connectivity systems embeds personal screens, USB ports, and Wi-Fi into seats, catering to tech-savvy passengers demanding seamless digital experiences. Growth in lie-flat and suite-style business class seating elevates premium travel with privacy doors, direct aisle access, and adjustable beds for enhanced luxury. Focus on sustainable and recyclable materials incorporates bio-composites and recycled fabrics to lower environmental impact amid ESG pressures. Increased retrofitting of aircraft cabins post-pandemic prioritizes modular upgrades for hygiene, air filtration, and flexible layouts to restore traveler confidence.

Key Players in the Global Aircraft Seating Industry

- Safran Seats

- Recaro Aircraft Seating

- Collins Aerospace

- ZIM Aircraft Seating

- Thompson Aero Seating

- Stelia Aerospace (Airbus Atlantic)

- Geven SpA

- Aviointeriors

- HAECO Cabin Solutions

- Explicit

- Mirus Aircraft Seating

- Jamco Corporation

Regional & Country Analysis

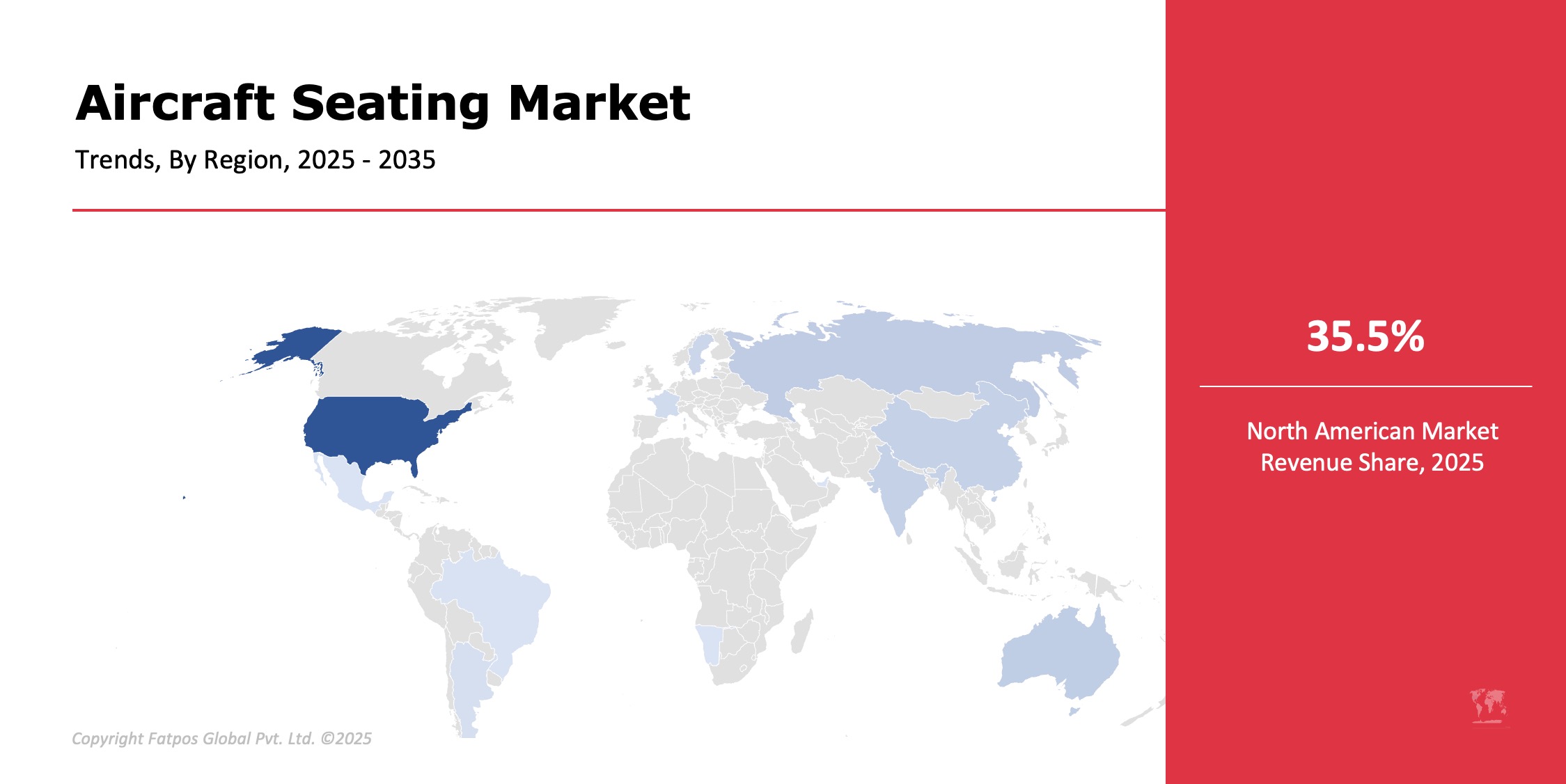

North America leads the global aircraft seating market, fueled by major manufacturers like Boeing and Airbus, extensive airline fleets, and robust retrofit programs for fleet modernization. Europe maintains a strong position through innovative seat makers such as Safran and Zodiac, alongside premium carriers like Lufthansa emphasizing high-end cabin products. Asia-Pacific emerges as the fastest-growing region, propelled by explosive passenger traffic in China and India, aggressive airline expansions, and emerging new aircraft deliveries. Latin America experiences moderate growth via low-cost carrier proliferation and regional connectivity improvements. The Middle East & Africa see demand from flagship premium airlines like Emirates and Qatar Airways, catering to long-haul luxury routes.

Segmentation Highlights

In the aircraft seating market, economy class dominates by volume due to high-density configurations on commercial flights, while premium classes like business and first drive revenue growth through high-value features. Narrow-body aircraft account for the largest demand, serving prolific short- and medium-haul routes with efficient seating layouts. Seat frames and upholstery constitute the biggest component share, balancing structural integrity, comfort, and weight savings. Commercial aviation leads overall end-user demand, far outpacing business jets and regional operators in scale and procurement volume.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 12.8 billion |

|

Market CAGR |

6.4% |

| By Seat Type | Economy Class, Premium Economy Class, Business Class, First Class |

|

By Aircraft Type |

Narrow-Body Aircraft, Wide-Body Aircraft, Regional Jets, Business Jets |

|

By Component |

Seat Frame, Cushions & Upholstery, Actuators & Controls, In-Flight Entertainment Integration, Others |

|

By End User |

Commercial Aviation, Business & General Aviation, Military Aviation |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Aircraft Seating Market: Key Players |

Safran Seats, Recaro Aircraft Seating, Collins Aerospace, ZIM Aircraft Seating, Thompson Aero Seating, Stelia Aerospace (Airbus Atlantic) |

Global Aircraft Seating Industry Instances

- Airlines introduced new premium economy cabins on long-haul routes.

- Aircraft manufacturers adopted ultra-lightweight seating solutions.

- Business jet operators invested in custom luxury seating interiors.

- Seat manufacturers expanded aftermarket and retrofit services.

Analyst Review

As per our Aircraft Seating Market analysis report, market continues to evolve as airlines prioritize passenger experience, operational efficiency, and sustainability. While economy seating dominates volumes, premium seating innovations drive profitability. Manufacturers focusing on lightweight materials, modular designs, and faster certification processes are expected to gain competitive advantage through 2035.

Frequently Asked Questions (FAQ):

Rising air travel, aircraft deliveries, and cabin modernization.

Economy class seats by volume.

Premium economy and business class seating.

North America.

Steady growth supported by fleet expansion and cabin upgrades.

Select License Type

Select License Type