Orthopedic Splints and Casts Market Research, 2034

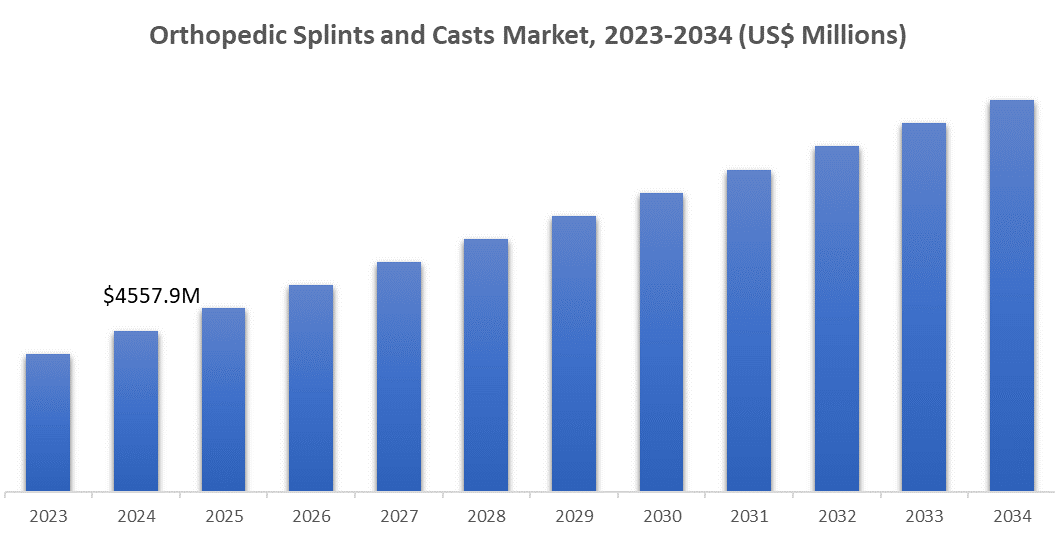

The global orthopedic splints and casts market is projected to grow at a CAGR of 7.5% in the forecast period (2024-2034), with the market size valued at US$ 4242.9 million in 2023 and anticipated to reach US$ 9425.6 million by 2034.

Orthopedic splints and casts are medical tools that are used to restrict movement and provide assistance to injured or fractured body parts. Casts, constructed from plaster or synthetic materials, are firm and offer durable, prolonged stability for fractures or post-operative care. In contrast, splints are flexible and can be altered to offer temporary or semi-permanent support for sprains, strains, and fractures.

They are typically made from materials like thermoplastics or cushioned fabric. Both casts and splints play a crucial role in orthopedic treatment, promoting proper bone healing, facilitating recovery, and minimizing pain and the risk of additional injury. Advances in materials and technology have enhanced comfort, durability, and functionality, improving patient results in different clinical environments.

Market Highlights

The Market growth is driven by the rising incidence of orthopedic injuries among the elderly and increased sports participation. The market is further strengthened by advancements in materials such as lightweight and breathable synthetics, enhancing patient comfort and usability. Expansion of healthcare facilities and improved access to orthopedic care also contribute to market growth.

Additionally, future growth is expected to be fueled by advancements in integrating smart technology for customized treatment options and improved patient outcomes. The increasing availability of healthcare in developing economies will also sustain the demand for these medical devices.

Source: Fatpos Global

Market Segmentation

Synthetic splints and casts' lightweight and durable characteristics have labeled them as the dominant market segment

The market is classified based on the Materials into Synthetic Splints & Casts, and Plaster of Paris Splints & Casts. In the current market landscape, Synthetic Splints and Casts have significantly outperformed Plaster of Paris as the primary material choice. This shift is due to several key advantages. Artificial materials are much lighter, improving patient comfort and mobility. They have greater longevity, and are less susceptible to damage, leading to an extended lifespan.

Several synthetic options are water-resistant, enabling individuals to participate in everyday tasks without limitations. Furthermore, artificial casts and splints have a faster drying time compared to plaster, which reduces any form of inconvenience for patients. They are usually transparent on X-rays, so they don't need to be taken out for imaging. Customized synthetic casts can frequently be tailored to better fit the patient's anatomy and come in a range of colors and designs, enhancing patient satisfaction.

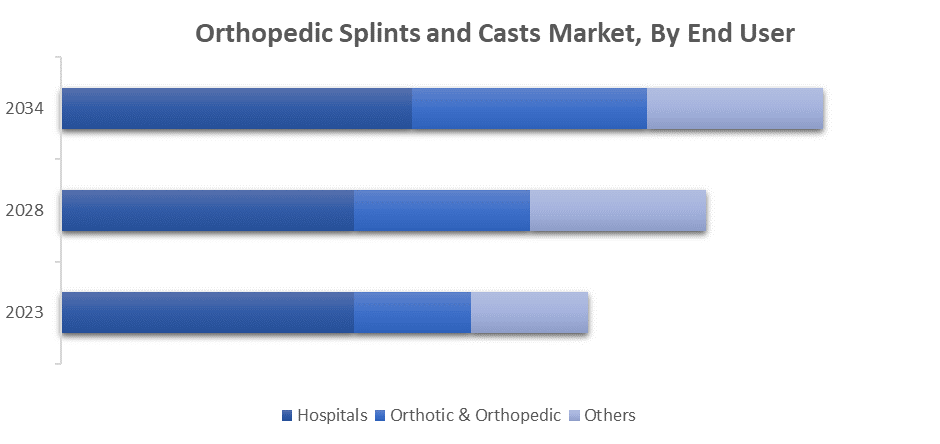

Hospitals hold a significant market share due to specialized units, essential equipment, and infrastructure

The market is classified based on End Users into Orthotic & Orthopedic Clinics, Hospitals, and Others. Hospitals are the dominant users of orthopedic splints and casts due to several compelling factors. They are equipped to deal with emergencies such as accidents and traumas, which frequently lead to fractures and soft tissue injuries that require splints and casts. Many orthopedic surgeries necessitate post-operative immobilization, making hospitals the primary users.

Furthermore, hospitals often have dedicated wards for orthopedic care and teams of trained staff who are proficient in using and overseeing these tools. They have all the infrastructure needed, such as casting rooms and equipment, to effectively manage a large number of patients. Moreover, hospitals offer a wide range of medical services, such as diagnostic imaging, physiotherapy, and follow-up care, crucial for successful splint and cast treatment.

Source: Fatpos Global

Market Dynamics

Growth Drivers

Growing Prevalence of Musculoskeletal Disorders to Create Significant Demand for Orthopaedic Splints and Casts

The increasing prevalence of musculoskeletal disorders such as arthritis, osteoporosis, and sports injuries is significantly fueling the need for orthopedic splints and casts. Arthritis and osteoporosis are common long-term health issues that cause joint pain, stiffness, and higher chances of fractures, requiring the use of splints and casts for immobilization and assistance.

Moreover, the surge in sports participation and related injuries such as sprains, strains, and fractures, also contributes to the growing need for medical treatment. Proper management of these conditions frequently necessitates the utilization of orthopedic devices to assist in healing and alleviating pain. With the growing recognition of these conditions and advancements in diagnosis, the demand for splints and casts is on the rise to meet the needs of an increasing number of patients.

Rising Geriatric Population Being Susceptible to Fractures and Orthopaedic Conditions Drive Market Growth

The increasing geriatric population is a vital factor in driving the expansion of the market. Elderly individuals are at a higher risk for fractures, osteoporosis, and other orthopedic issues due to their lower bone density and age-related deterioration. This shift in population demographics results in more bone injuries and degenerative disorders, requiring the use of splints and casts for proper treatment and recovery.

Additionally, older individuals frequently need immobilization after orthopedic surgeries, leading to increased demand. As the world's population gets older, there will likely be a higher demand for dependable and effective orthopedic treatments like splints and casts, leading to market expansion and progress.

Restraints

High Cost of Advanced Materials May Limit the Accessibility of Splints and Casts

The significant challenge to market growth is the high cost of advanced materials in orthopedic splints and casts. Cutting-edge materials like advanced composites and specialized synthetics provide better durability, less weight, and increased comfort for the patient. Nevertheless, these benefits are accompanied by a high cost, making it difficult for many patients to access, especially those lacking sufficient insurance or in areas with limited healthcare resources.

The high expenses also create obstacles for healthcare providers dealing with budget constraints, limiting their capacity to implement and provide these innovative solutions on a large scale. As a result, although these resources promote technological advancement, their costly nature may impede broad market acceptance and availability.

Recent Developments

- In 2023, ALCARE introduced a new line of lightweight, synthetic casts designed for improved comfort and durability. The company also expanded its distribution network in emerging markets, aiming to increase accessibility to its orthopedic products.

- In 2023, Bauerfield launched a new range of orthopedic splints featuring advanced materials for better flexibility and support. In 2024, the company entered into a joint venture with a technology firm to integrate smart sensors into its cast and splint products for enhanced monitoring of healing progress.

- In 2023, Thuasne Group launched a new series of customizable orthotic splints tailored for specific medical conditions. The company acquired a small orthotics company to expand its product portfolio and strengthen its market presence.

- In 2023, Tynor introduced a new range of eco-friendly splints and casts made from recyclable materials. The company expanded its manufacturing capabilities with a new facility in Asia-Pacific to meet growing regional demand.

- In 2023, Orthosys launched an innovative cast removal system designed to enhance safety and ease of use. In 2024, the company is strongly focusing on digital transformation by incorporating AI technology into its product development process for improved precision.

Key Players

- ALCARE

- Bauerfeind

- Thuasne Group

- Breg

- Tynor

- Orthosys

- Carolina Narrow Fabric

- DeRoyal Industries

- Allard USA

- Enovis

- Essity Medical Solutions

- Frank Stubbs Company

- Lohmann & Rauscher

- medi

- Performance Health

- Other Prominent Players (Company Overview, Business Strategy, Key Product Offerings, Financial Performance, Key Performance Indicators, Risk Analysis, Recent Development, Regional Presence, SWOT Analysis)

Regional Analysis

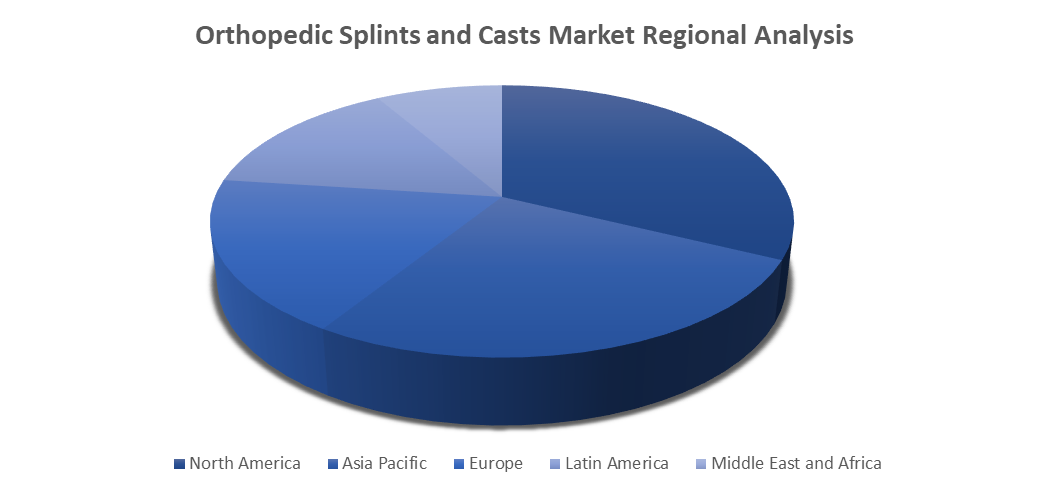

Global Orthopedic Splints and Casts Market is segmented based on regional analysis into five major regions: North America, Latin America, Europe, Asia Pacific and the Middle East and Africa.

The market is experiencing rapid growth in Asia Pacific, fueled by the region's expanding healthcare infrastructure, growing awareness of orthopedic treatments, and rising incidence of musculoskeletal disorders. The high number of elderly residents in the area and increasing cases of sports-related injuries contribute to the demand as well. Improvement in economic development in nations such as China and India leads to increased availability of advanced medical treatments and technologies, thus contributing to the growth of the market.

North America is dominating the market due to its advanced healthcare systems, high incidence of orthopedic conditions, and substantial investment in medical technology.

Europe closely follows, taking advantage of a well-developed healthcare system and a growing elderly population.

Latin America, the Middle East, and Africa are developing markets experiencing growth due to enhanced healthcare access and rising investments in medical facilities and technologies.

Source: Fatpos Global

Impact of Covid-19 on the Market

The market was significantly impacted by the Covid-19 pandemic. Elective surgeries and non-emergency medical interventions were rescheduled or halted to give priority to COVID-19 patients, causing a temporary decline in the overall demand for splints and casts. Furthermore, disruptions in the supply chain led to shortages of both raw materials and finished goods, ultimately impacting market expansion.

Nevertheless, the increased focus on telemedicine and remote patient monitoring spurred creativity in digital health offerings, such as smart splints and casts. As healthcare systems adjust and heal, the market is forecasted to bounce back, propelled by the return of elective surgeries, increasing awareness of musculoskeletal health, and the incorporation of innovative technologies in orthopedic treatment.

Market is further segmented by region into:

- North America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United States and Canada

- Latin America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – Mexico, Argentina, Brazil, and Rest of Latin America

- Europe Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United Kingdom, France, Germany, Italy, Spain, Belgium, Hungary, Luxembourg, Netherlands, Poland, NORDIC, Russia, Turkey, and Rest of Europe

- Asia Pacific Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – India, China, South Korea, Japan, Malaysia, Indonesia, New Zealand, Australia, and Rest of APAC

- Middle East and Africa Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – North Africa, Israel, GCC, South Africa, and Rest of MENA

Market Scope and Segments:

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2018-2034 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2034 |

|

Historical Period |

2019-2022 |

|

Growth Rate |

CAGR of 7.5% from 2024-2034 |

|

Unit |

Value (US$ Million) |

|

Segmentation |

Main Segments List |

|

By Product |

|

|

By Material |

|

|

By Body Part |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions (FAQ):

The global orthopedic splints and casts market size was values at US$ 4242.9 million in 2023 and is projected to reach the value of US$ 9425.6 million in 2034, exhibiting a CAGR of 7.5% during the forecast period.

The market includes devices used to immobilize and support injured body parts. This market includes various products like rigid casts, flexible splints, and advanced materials designed for fracture management, sprains, and post-surgical support. It is driven by rising orthopedic injuries and technological advancements.

The Synthetic Splints & Casts and Hospitals segment accounted for the largest market share.

Key players in the orthopedic splints and casts market include ALCARE, Bauerfeind, Thuasne Group, Breg, Tynor, Orthosys, Carolina Narrow Fabric, DeRoyal Industries, Allard USA, Enovis, Essity Medical Solutions, Frank Stubbs Company, Lohmann & Rauscher, medi, Performance Health and Other Prominent Players.

Rising geriatric population, increasing incidence of musculoskeletal disorders, and advancements in material technology drive the market.

Select License Type

Select License Type