EV Chargers Market Research 2035

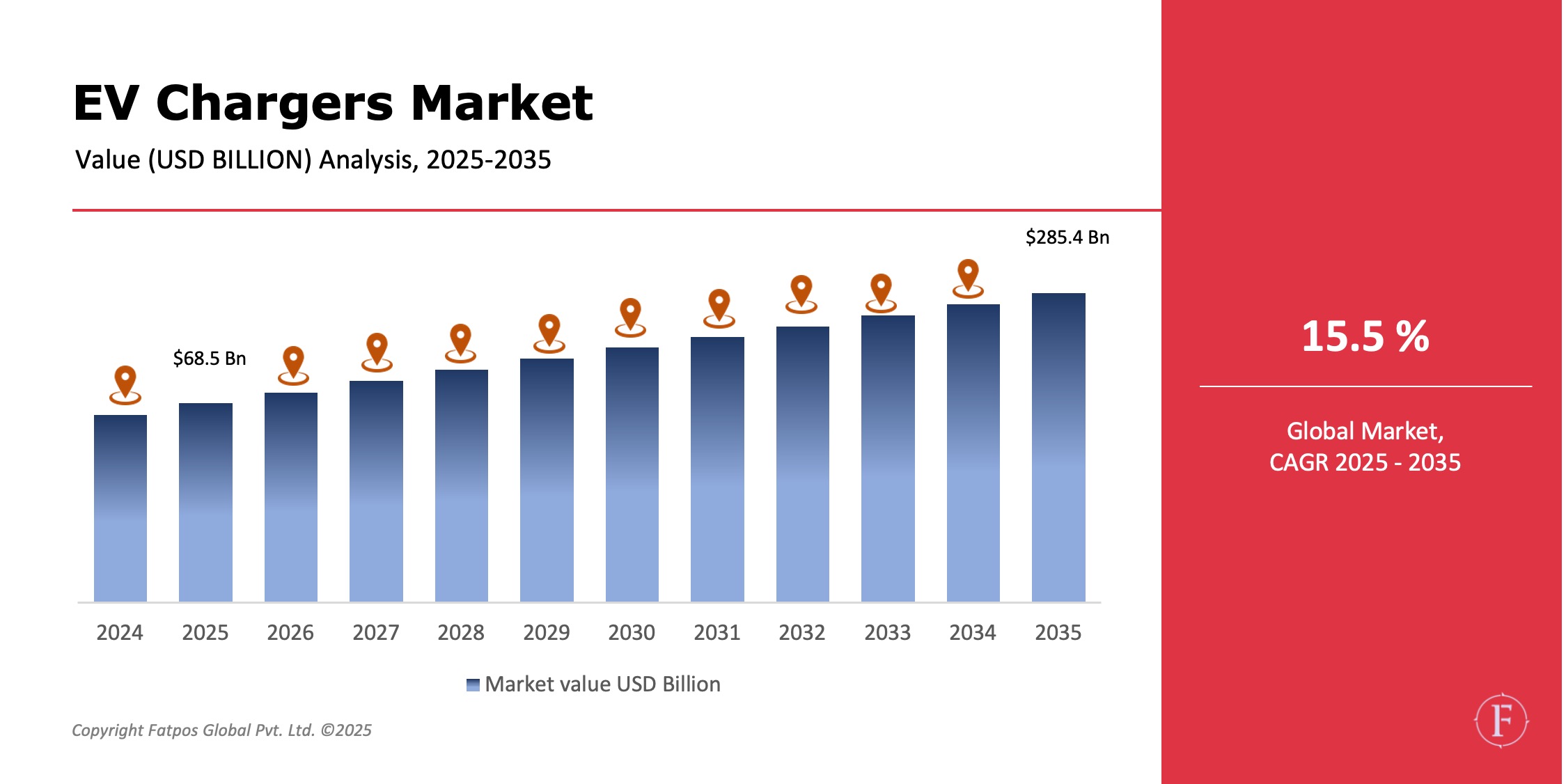

The EV Chargers Market Size was valued at USD 68.5 billion in 2025 and is projected to reach USD 285.4 billion by 2035, registering a CAGR of 15.5%. Market growth is driven by rapid electric vehicle adoption, aggressive government policies supporting electrification, expansion of charging infrastructure, declining battery costs, and rising investments in smart and fast-charging technologies.

EV chargers are critical components of the electric mobility ecosystem, enabling safe and efficient energy transfer between the power grid and electric vehicles. As global transportation systems transition toward low-emission alternatives, the availability, reliability, and scalability of charging infrastructure have become central to EV adoption across passenger, commercial, and public transport segments.

Product Overview

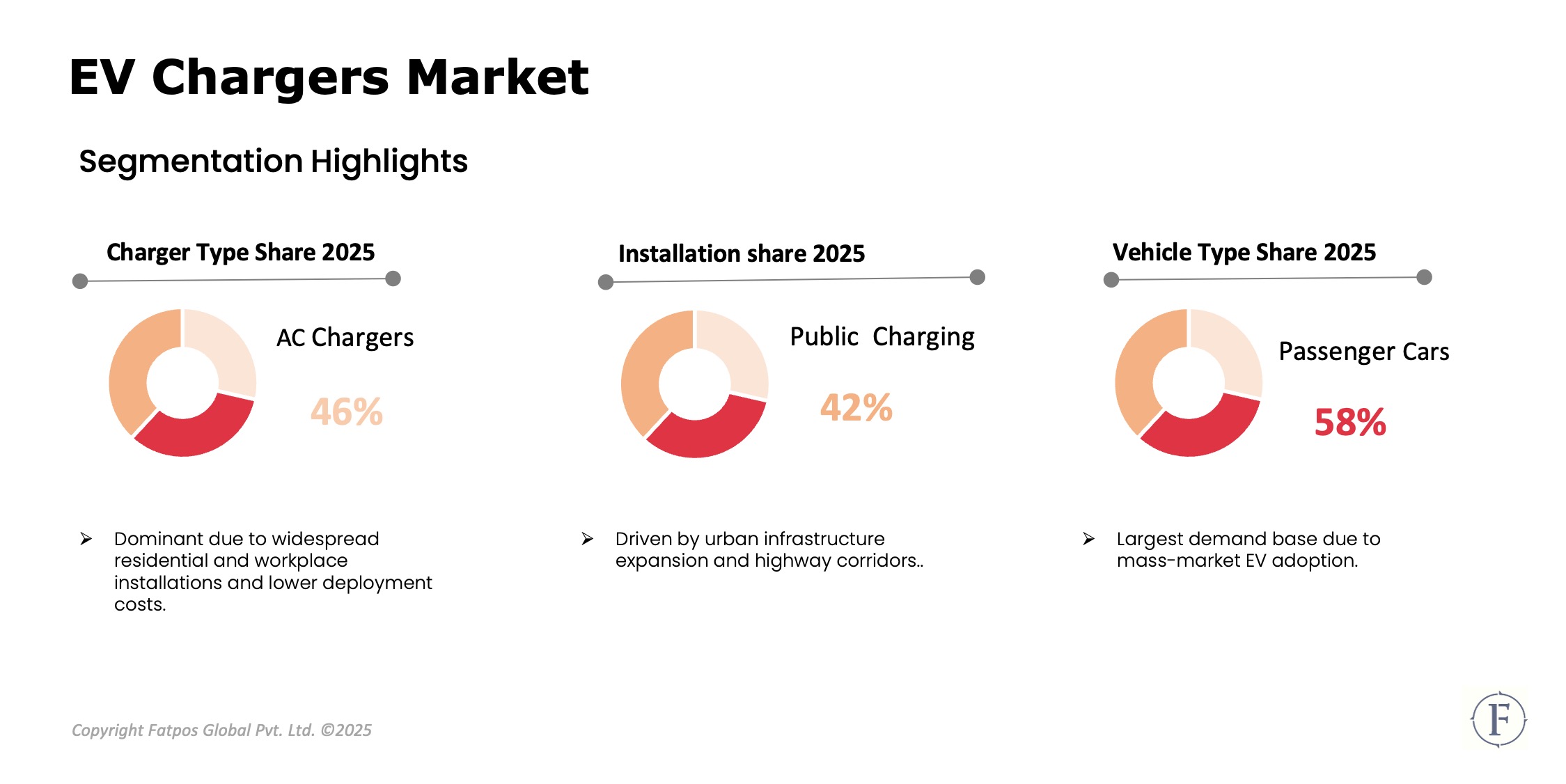

EV chargers are power supply devices designed to recharge electric vehicle batteries by converting electrical energy from the grid into a form suitable for vehicle storage systems. By charger type, AC chargers dominate residential and workplace installations due to lower costs and compatibility with standard electrical infrastructure. DC fast chargers enable rapid charging in public and highway locations, while ultra-fast chargers support high-power applications for fleet operations and long-distance travel.

By charging level, Level 1 chargers offer basic, low-speed charging primarily for residential use. Level 2 chargers represent the most widely adopted solution across homes, commercial buildings, and public locations due to balanced speed and affordability. Level 3 chargers, including DC fast chargers, are essential for commercial fleets, public transit, and fast turnaround charging. EV chargers are deployed across residential, commercial, and public settings, supporting a wide range of vehicle types including passenger cars, electric buses, light commercial vehicles, and two- and three-wheelers.

Key Takeaways:

- The EV Chargers Market is expected to grow at ~15.5% CAGR through 2035

- Level 2 chargers dominate overall installations

- DC fast charging is the fastest-growing segment

- Public and commercial installations are expanding rapidly

- Asia-Pacific leads global charger deployment

- Smart and networked charging solutions are key differentiators

Market Dynamics

Drivers

The primary driver of the EV chargers market is the rapid global adoption of electric vehicles driven by climate policies, fuel economy standards, and emission reduction targets. Governments across North America, Europe, and Asia-Pacific are implementing incentives, subsidies, and mandates to accelerate EV adoption and charging infrastructure deployment. Rising investments in public charging networks, particularly along highways and urban centers, support range confidence and mass-market adoption.

Growth in commercial EV fleets, ride-sharing services, and electric public transportation further boosts demand for fast and ultra-fast charging solutions. Technological advancements in power electronics, connectivity, and energy management enhance charger efficiency, reliability, and user experience.

Restraints

Despite strong growth, the EV chargers market faces restraints related to high installation costs, grid integration challenges, and uneven infrastructure availability. Deployment of fast-charging stations requires significant capital expenditure, grid upgrades, and permitting processes. Interoperability issues between charging standards and connectors, along with fragmented regulatory frameworks, complicate large-scale rollouts. In developing regions, limited grid capacity and lack of standardized policies further restrict adoption Cybersecurity risks associated with connected chargers also present emerging concerns.

Opportunities

Significant opportunities exist in smart charging, vehicle-to-grid (V2G) integration, and renewable-powered charging stations. Smart chargers enable load balancing, dynamic pricing, and energy optimization, supporting grid stability and cost efficiency. Growth of electric buses, delivery fleets, and logistics electrification creates demand for high-capacity depot charging solutions. Expansion of charging infrastructure in emerging economies and smart city projects offers long-term growth potential. Integration of AI, cloud platforms, and payment solutions further enhances monetization opportunities.

Challenges

Key challenges include managing grid load impact, ensuring charger uptime, and achieving cost-effective scalability. High-power chargers place stress on local grids, requiring advanced energy management and storage integration. Standardization across connectors, communication protocols, and payment systems remains a challenge. Rapid technological evolution also shortens product lifecycles, requiring continuous R&D investment. Ensuring cybersecurity, data privacy, and compliance across connected charging networks adds further complexity.

EV Chargers Market Trends

Smart, networked chargers dominate, equipped with IoT for remote monitoring via apps, AI predictive maintenance to preempt failures, and dynamic energy management optimizing peak loads—reducing costs 20-30%. Ultra-fast chargers (350-500kW) expand on highways, urban corridors, and depots, enabling 80% charge in 15-25 minutes, vital for fleet and intercity travel.

Stations integrate solar panels, wind, and onsite batteries (e.g., NMC or flow types) for off-grid operation, minimizing carbon footprints and utility bills. Subscription services like Electrify America passes, cross-provider roaming (Hubject), and unified NFC/RFID payments enhance seamless access. Strategic alliances—Volkswagen with Electrify, BP with Tesla—pool investments for millions of ports, standardizing plugs (CCS/NACS) and software. These shifts support global EV targets amid infrastructure lags.

Key Players in the EV Chargers Industry

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- ChargePoint, Inc.

- Tesla, Inc.

- EVBox Group

- Blink Charging Co.

- Delta Electronics, Inc.

- Webasto Group

- Tritium DCFC Limited

Regional & Country Analysis

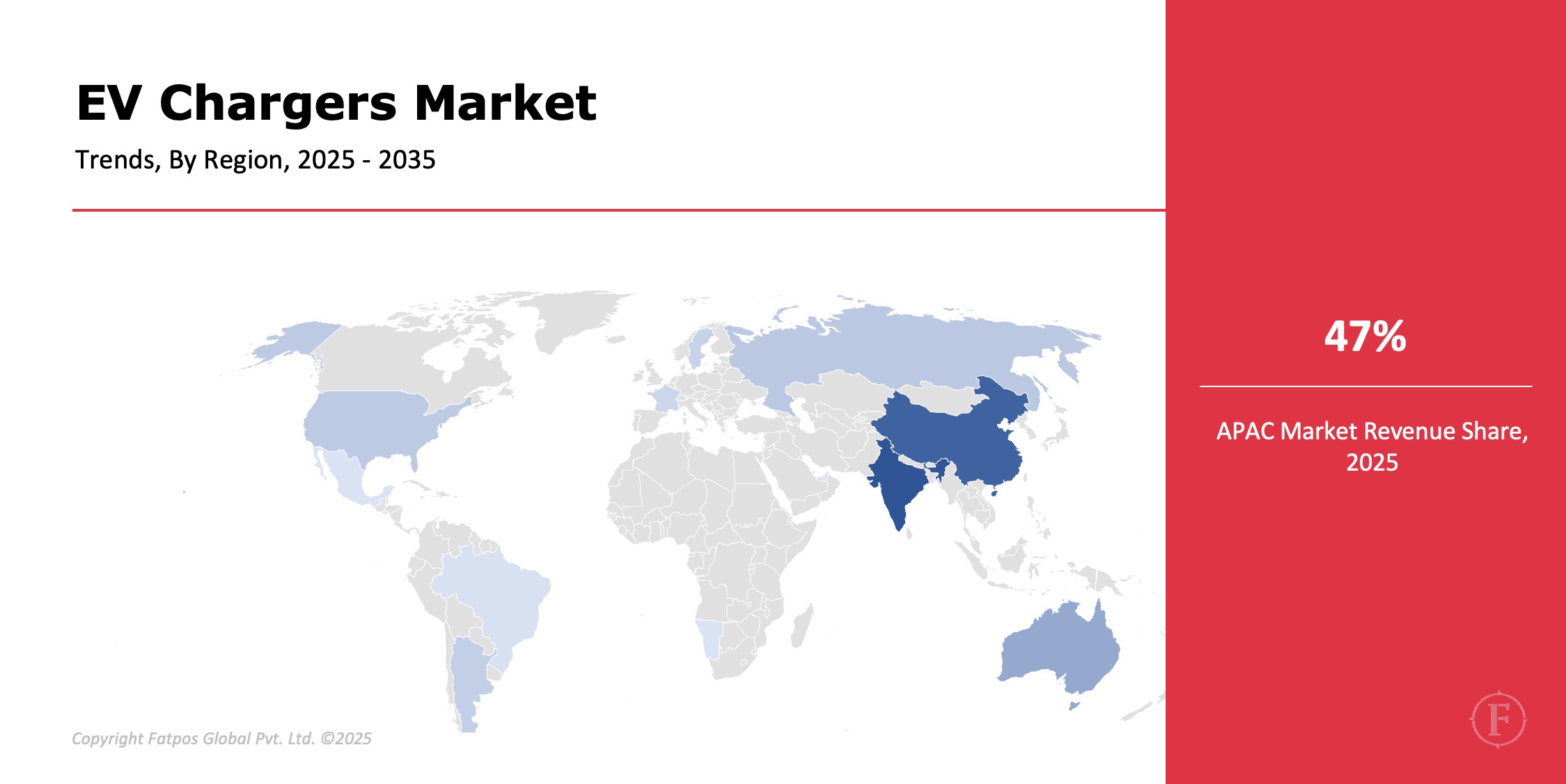

Asia-Pacific dominates the EV chargers market due to large-scale EV adoption, strong government support, and rapid infrastructure expansion in China, Japan, South Korea, and India. Europe shows strong growth driven by stringent emission regulations and pan-European charging initiatives. North America continues to expand through public-private partnerships and federal funding programs. Latin America and Middle East & Africa represent emerging markets supported by urban electrification and smart mobility projects.

Segmentation Highlights

By charger type, AC and Level 2 chargers hold the largest share due to widespread residential and commercial deployment. DC fast chargers show the fastest growth, particularly in public and fleet applications. Passenger cars dominate vehicle-type demand, while commercial vehicles and buses demonstrate higher growth rates.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 285.4 Billion |

|

Market CAGR |

15.5% |

|

By Charger Type |

AC chargers, DC Fast chargers, Ultra-Fast chargers |

|

By Charging Level |

Level 1, Level 2, Level 3

|

|

By Installation |

Residential, Commercial, Public |

|

By Vehicle Type |

Passenger Cars, Commercial Vehicles, Buses, Two & Three Wheelers |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

EV Chargers Market: Key Players |

ABB, Siemens, Schneider Electric, ChargePoint, Tesla

|

Global EV Chargers Industry Instances

- Governments rolled out nationwide public fast-charging networks to strengthen market share.

- Logistics companies deployed depot-based DC charging for fleets

- Automakers partnered with utilities to expand home charging solutions

- Smart cities integrated EV chargers with renewable energy systems

Analyst Review

As per our EV chargers market analysis report, the market is transitioning from early infrastructure build-out to large-scale, technology-driven deployment. While grid integration, standardization, and cost challenges persist, advancements in smart charging, energy storage, and policy support are unlocking strong long-term growth. The market forecast indicates companies focusing on interoperability, scalability, and digital platforms are expected to lead the market through 2035.

Frequently Asked Questions (FAQ):

EV chargers supply energy via cables/wireless: Level 1 (slow home), Level 2 (7-22kW), DC fast (50-350kW) with OCPP protocols, safety, metering.

EV sales surge to 40M by 2030, subsidies, $100B+ funds, net-zero goals drive chargers; cheaper batteries, range fixes boost installs.

Level 2 chargers hold 60%+ share, balancing affordability ($500-2K/unit), speed (25-60 miles/hour), and versatility for homes, offices, malls. They suit daily use, outpacing slow Level 1 and pricier ultrafast DC amid grid limits.

Asia-Pacific commands 47% share, led by China's 2M+ public ports (State Grid), Japan's dense urban networks, and India's FAME incentives.

Steep install costs ($2K-10K/site) deter rollouts; grid overloads from clustered demand strain aging networks; standardization gaps (CCS vs. CHAdeMO) confuse users/supply chains.

Select License Type

Select License Type