Virtual Reality (VR) Software Market Size

Virtual Reality Software Market Research, 2034

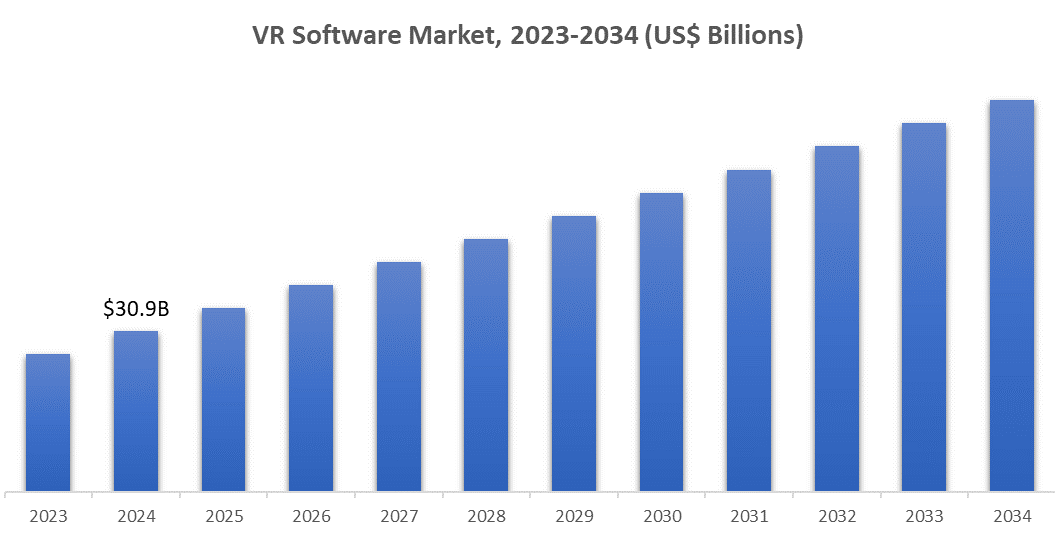

The global virtual reality (VR) software market is poised for significant expansion, with projections indicating a compound annual growth rate (CAGR) of 33% from 2024 to 2034. Starting from a valuation of US$ 23.3 billion in 2023, the market is expected to surge to an impressive US$ 538.1 billion by 2034.

Virtual reality (VR) software enables users to interact with digital environments in an immersive manner using specialized hardware like VR headsets. This software comes in different forms, including 3D modelling software for creating detailed virtual objects and environments, VR software for immersive panoramic experiences, and simulation software for real-time interactive scenarios.

VR is utilized across various industries: gaming and entertainment for immersive experiences, education, and training for interactive learning, healthcare for medical training and therapy, and retail and architecture for virtual tours and design visualization. Despite its potential, virtual reality software faces challenges such as high costs, technical limitations, and the need for robust infrastructure.

Market Highlights

The market is rising due to the growing desire for gaming and entertainment is pushing for technological progress, resulting in more immersive and available VR experiences. Additionally, sectors such as healthcare, education, and training are incorporating VR technology for simulations and interactive learning, improving effectiveness and participation.

Additionally, progress in technology and a significant reduction in prices have made virtual reality more accessible and popular. Moreover, increased funding from leading technology firms drives advancements and progress in the virtual reality industry. Anticipated future expansion as VR becomes essential for a wide range of uses, from virtual gatherings to distant teamwork, showcasing its increasing impact and adaptability in different industries.

Source: Fatpos Global

Market Segmentation

Real-time software's versatility in industrial applications and its ability to create immersive experiences position it as a leading market segment

The market is segmented based on Type into 3D Modelling Software, 360-degree Custom VR Software, and Real-time Simulation Software. Real-time Simulation Software is currently the leading type of VR software in the market. Its demand is influenced by its ability to be used in a variety of industries such as gaming, healthcare, training, education, and engineering. Real-time simulation software is essential for flight simulators, medical training, and military exercises as it offers immersive and interactive experiences.

Ongoing progress in graphics processing, AI integration, and haptic feedback improves authenticity and interactivity, drawing in a larger user base. It is commonly used in training and education to provide a safe environment for practicing skills. Businesses and educational institutions are attracted to the cost-effectiveness in comparison to traditional training methods. In the world of gaming, it provides exciting experiences that drive the rise in VR game popularity. Moreover, it facilitates remote teamwork by allowing virtual communication among team members.

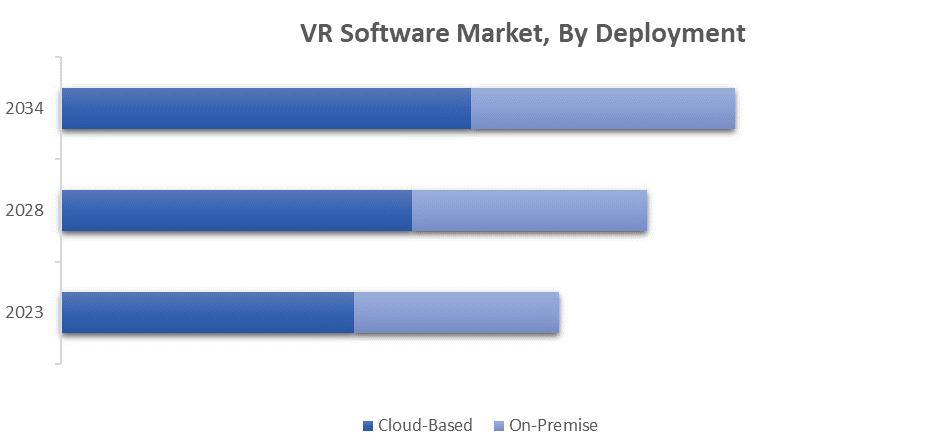

Cloud-based software’s scalability and easier accessibility position them as the dominant segment

The market is segmented based on Deployment into Cloud-Based and On-Premise. Cloud-based VR software is prevalent due to its ability to scale, adapt, and provide cost savings. Businesses can easily modify resources according to demand, cutting upfront hardware expenses by using a pay-as-you-go model. Cloud-based options allow distant teams to work together in real time through remote access. Cloud providers take care of regular updates and maintenance to guarantee users to access the most up-to-date features.

Connecting with different cloud services boosts capabilities, as extensive data storage and strong processing power facilitate intricate simulations. Global cloud infrastructure offers essential low-latency access for global business operations. Effective disaster recovery and backup solutions guarantee the continuation of business operations. With the increasing popularity of remote work and digital transformation, cloud-based VR solutions are becoming increasingly important, accredited to advancements such as edge computing and improved security measures.

Source: Fatpos Global

Market Dynamics

Growth Drivers

Increasing Adoption of VR in Gaming and Entertainment to Provide Significant Growth Opportunities

The ever-rising use of VR in gaming and entertainment plays a pivotal role in propelling the market forward. Initially, there is a growing need for VR software content as more users are looking for immersive gaming and entertainment experiences. The increase in demand results in a dynamic market for developers who are producing VR games, movies, simulations, and interactive experiences, which guarantees a continuous supply of appealing content for VR headset users.

Additionally, the effectiveness of VR devices is heavily reliant on the accessibility and caliber of software. A strong market not only satisfies but surpasses user expectations, encouraging ongoing investment in VR headsets and accessories. Furthermore, the appeal of VR in the gaming and entertainment industries draws significant investment from both established corporations and new ventures.

Rising Investment in VR by Major Technology Companies to Boost Overall Market Growth

Recently, there has been a rising interest from major technology companies in virtual reality boosting overall expansion in the VR software industry through various important channels. To begin with, these major technology companies are leading progress in VR hardware by investing significantly in improved resolution screens, upgraded processing power, and advanced user tracking technology. These developments pave the way for even more enriched and intricate VR software experiences, expanding the possibilities in virtual reality.

Moreover, larger organizations frequently create specialized software development kits (SDKs) and tools for VR software development, streamlining the process and empowering developers to create better content. Additionally, larger organizations are creating platforms for VR content production and sharing, either on their own or by adding VR features to current platforms. This broader reach provides VR software developers with access to a larger audience and robust distribution channels, nurturing a thriving ecosystem of VR content.

Restraints

Technical Challenges About Motion Sickness and Latency Issues Act as Significant Restraint on the Market

Technical challenges such as motion sickness and latency problems are major limitations for the VR software industry in various important aspects. Feeling sick and disoriented while using VR can discourage people from trying VR experiences, which in turn limits the market growth and reduces the overall attractiveness of VR software. Likewise, latency problems result in slow response times, interrupt the sense of being fully absorbed, and annoy users, preventing extended usage of VR applications.

These challenges impose constraints on content creation, mandating developers to create experiences that lessen discomfort, which can inhibit innovation and variety in VR software choices. Therefore, the expansion of the market could be hindered by users' reluctance to purchase hardware due to several usability issues. Attempts to address these limitations involve developments in hardware technology to enhance display refresh rates and tracking precision, along with software design methods like optimized rendering and user-adaptation strategies.

Recent Developments

- In Q3 of 2023, Meta (formerly Facebook) launched the next generation of their standalone VR headset, the Meta Quest 3, featuring improved processing power, higher resolution display, and enhanced comfort features. The company also acquired Within, a leading provider of VR fitness experiences, signaling its focus on expanding the VR fitness software market.

- In 2023, Google open-sourced several VR development tools like the OpenXR API and the Filament rendering engine. This promotes broader VR software development and could benefit the overall market.

- In 2023, Unity Technologies launched Unity MARS, a suite of tools specifically designed for creating and managing interactive experiences in the metaverse. This caters to the growing demand for VR software for metaverse applications. The company also acquired Weta Digital, a renowned visual effects company, to strengthen its capabilities in creating realistic 3D assets and immersive experiences for VR software.

- In February 2023, Sony Interactive Entertainment LLC launched the PlayStation VR2, a next-generation VR headset for the PlayStation 5 console, offering improved visuals, enhanced controller tracking, and a wider field of view.

- In 2023, Epic Games, Inc. introduced MetaSound, a suite of tools within Unreal Engine for creating realistic and immersive spatial audio experiences for VR software applications.

Key Players

- Meta (Oculus)

- Unity Technologies

- Sony Interactive Entertainment LLC

- Epic Games, Inc. (Unreal Engine)

- Dassault Systèmes SE

- Sandbox VR

- Autodesk, Inc.

- Microsoft Corporation

- Google LLC

- EON Reality, Inc.

- HTC Corporation

- Nvidia Corporation

- Virtuix

- Infinadeck

- Sixense Enterprises Inc.

- Other Prominent Players (Company Overview, Business Strategy, Key Product Offerings, Financial Performance, Key Performance Indicators, Risk Analysis, Recent Development, Regional Presence, SWOT Analysis)

Regional Analysis

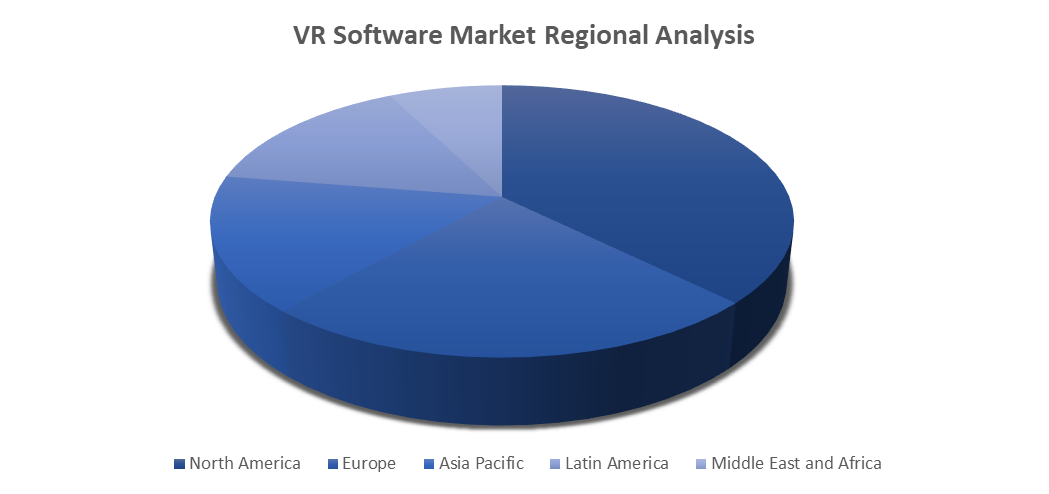

The global VR software market is segmented based on regional analysis into five major regions: North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa.

North America is currently the leading region in VR software with several compelling factors. The region is at the forefront of technological advancements and acceptance, with significant funding from major tech companies for VR development. Strong demand can be seen in various sectors such as gaming, entertainment, healthcare, and education, contributing to market expansion.

North America has strong market leadership due to the presence of numerous top VR software developers and technology companies globally. The availability of developed infrastructure and widespread high-speed internet access makes it easier to implement and use VR technologies. Moreover, substantial funding from venture capital firms and government programs also drives market growth.

Despite the growth of VR in Europe and Asia-Pacific, North America remains a leader in the industry owing to its advanced technology ecosystem and established market for VR software development and deployment.

Source: Fatpos Global

Impact of Covid-19 on the Market

The market experienced a multifaceted effect from the COVID-19 pandemic, with outcomes both beneficial and adverse. Supply chain disruptions caused by lockdowns and travel restrictions hindered the availability of VR hardware, thus impeding the growth of VR software reliant on these devices. Furthermore, in the early days of the pandemic, there was a trend towards purchasing essential items, leading to a decrease in spending on non-essential goods such as VR products.

Event cancellations and limitations on gatherings also negatively impacted location-based VR entertainment businesses that depended on VR software experiences. On the flip side, there were also some positive effects: COVID-19 led to a rise in the need for remote solutions, which in turn increased the popularity of VR software for training, education, and remote collaboration. VR fitness options became popular as individuals looked for different ways to work out in their own homes.

Market is further segmented by region into:

- North America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United States and Canada

- Latin America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – Mexico, Argentina, Brazil, and Rest of Latin America

- Europe Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United Kingdom, France, Germany, Italy, Spain, Belgium, Hungary, Luxembourg, Netherlands, Poland, NORDIC, Russia, Turkey, and Rest of Europe

- Asia Pacific Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – India, China, South Korea, Japan, Malaysia, Indonesia, New Zealand, Australia, and Rest of APAC

- Middle East and Africa Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – North Africa, Israel, GCC, South Africa, and Rest of MENA

Market Scope and Segments

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2018-2034 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2034 |

|

Historical Period |

2019-2022 |

|

Growth Rate |

CAGR of 33% from 2024-2034 |

|

Unit |

Value (US$ Billion) |

|

Segmentation |

Main Segments List |

|

By Type |

|

|

By Deployment |

|

|

By Application |

|

|

By Region |

|

Frequently Asked Questions (FAQ):

The global VR software market size was valued at US$ 23.3 billion in 2023 and is set to reach the value of US$ 538.1 billion in 2034, exhibiting a CAGR of 33%

The market provides interactive experiences for VR headsets. It's booming with growth, driven by gaming, training, and new applications like the metaverse. From 360° videos to real-time simulations, VR software fuels the immersive world of virtual reality.

The Real-time Simulation Software segment and Cloud-based segment accounted for the largest market share.

Key players in the global VR software market include Meta (Oculus), Unity Technologies, Sony Interactive Entertainment LLC, Epic Games, Inc. (Unreal Engine), Dassault Systèmes SE, Sandbox VR, Autodesk, Inc., Microsoft Corporation, Google LLC, EON Reality, Inc., HTC Corporation, Nvidia Corporation, Virtuix, Infinadeck, Sixense Enterprises Inc. and Other Prominent Players.

Rise demand for immersive experiences in gaming, entertainment, and training fuels the market's growth.

Select License Type

Select License Type