Data Converters Market Research 2035

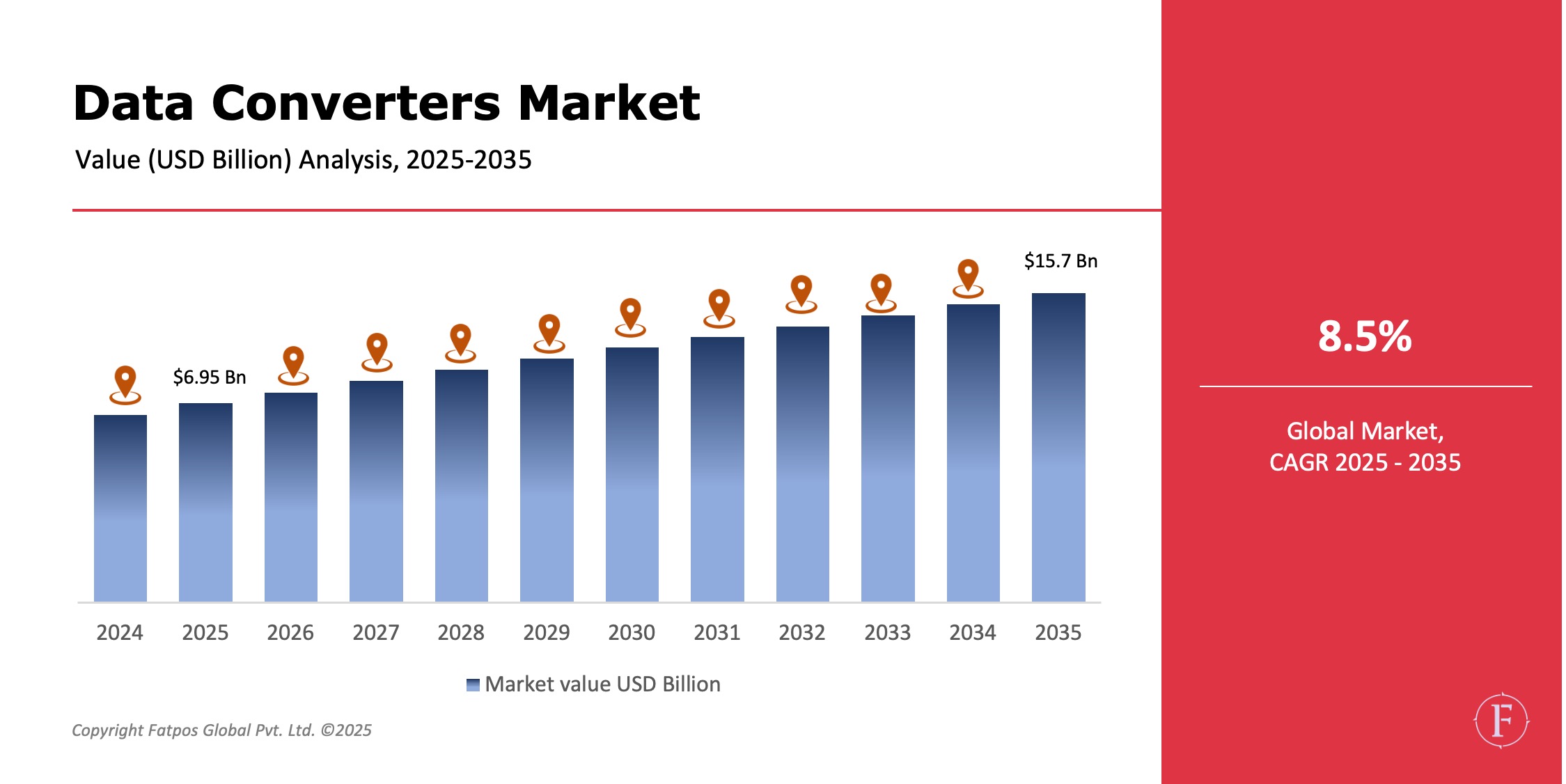

The Data Converters Market Size was USD 6.95 billion in 2025 and is projected to reach USD 15.7 billion by 2035, registering a CAGR of 8.5%. Market growth is driven by rapid digitization across industries, proliferation of IoT and connected devices, increasing demand for high-speed data acquisition, advancements in semiconductor technologies, and rising adoption of automation and smart systems.

Data converters play a critical role in modern electronic systems by enabling seamless translation between analog real-world signals and digital processing environments. As industries increasingly rely on data-driven decision-making, precise and high-performance data converters have become essential components across consumer, industrial, and mission-critical applications.

Product Overview

Data converters play a crucial role in signal processing by bridging analog and digital domains. Analog-to-Digital Converters (ADCs) digitize real-world signals like sound, temperature, pressure, and voltage for use in data acquisition, sensing, and communication systems. Conversely, Digital-to-Analog Converters (DACs) convert digital data back to analog for applications in audio, video, and control. Categorized by resolution, low-resolution types suit cost-sensitive consumer devices, mid-resolution ones power industrial and automotive systems, while high-resolution variants enable precision in instrumentation, medical imaging, and aerospace. Overall, they deliver signal integrity, low noise, high speed, and power efficiency across diverse uses.

Key Takeaways :

- The Data Converters Market is expected to grow at ~8.5% CAGR through 2035.

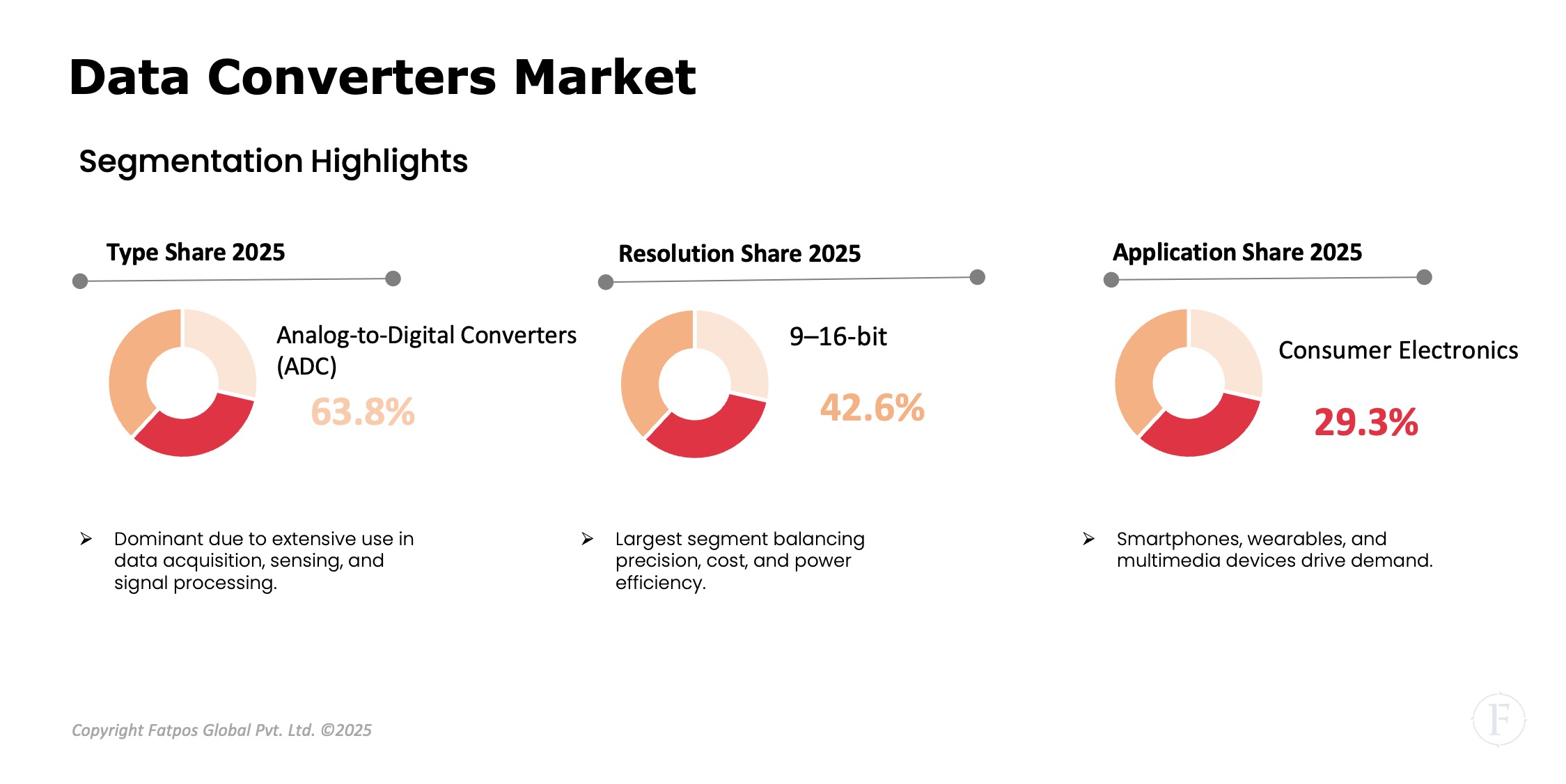

- Analog-to-Digital Converters hold the largest revenue share.

- Consumer electronics remain the largest application segment.

- Automotive and industrial automation are the fastest-growing applications.

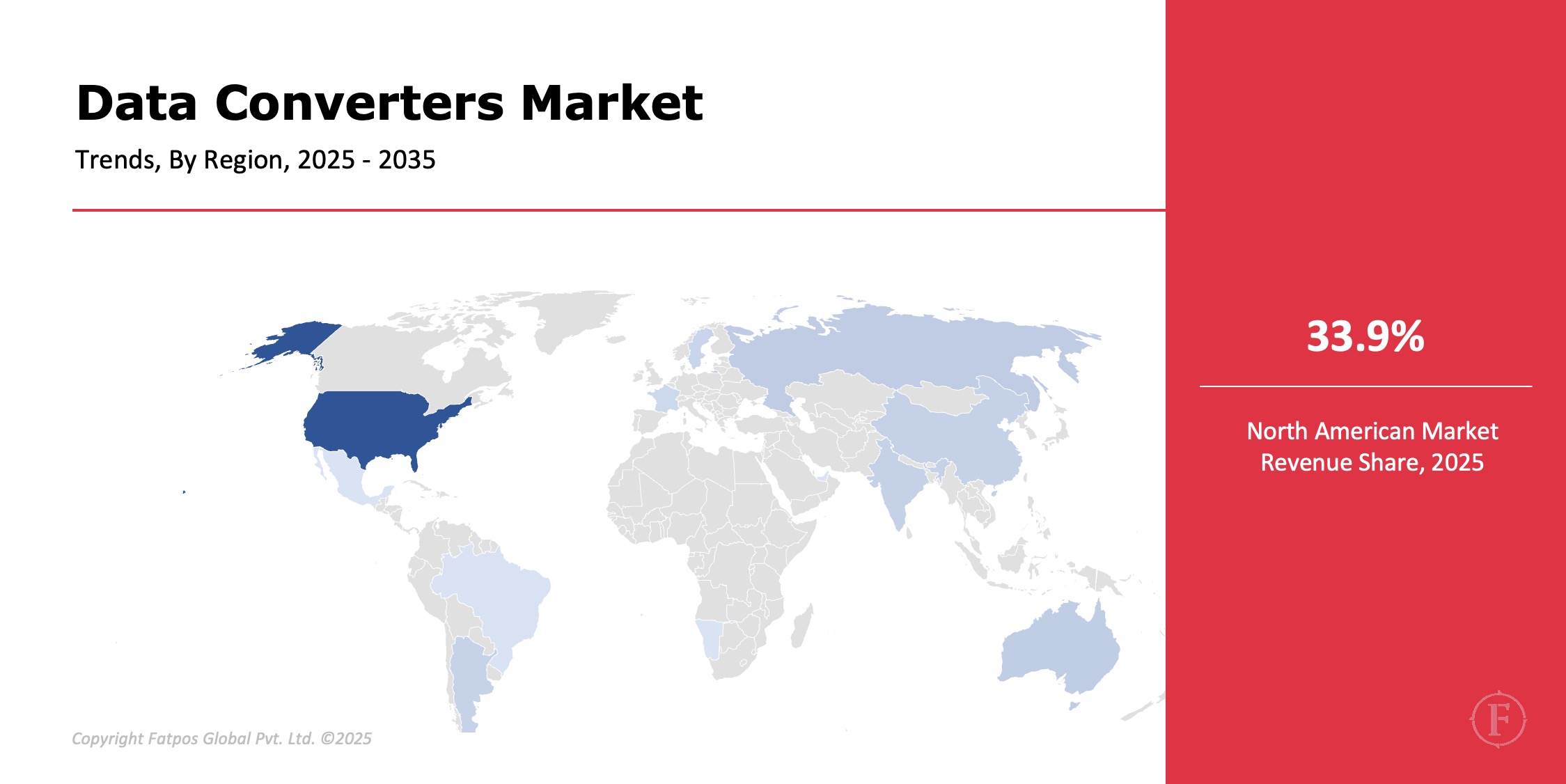

- Asia-Pacific dominates manufacturing and consumption.

- Miniaturization and low-power designs are key competitive factors.

Market Dynamics

Drivers

The accelerating adoption of smart devices, IoT sensors, and connected systems is a primary driver of the data converters market, as these applications require continuous and accurate signal conversion. Growth in automotive electronics—including ADAS, electric vehicles, and infotainment systems—demands high-speed and high-resolution converters for safety and control. Industrial automation and Industry 4.0 initiatives further boost demand for reliable data acquisition and real-time monitoring. Additionally, advancements in semiconductor manufacturing, such as CMOS scaling and mixed-signal integration, are enabling higher performance at lower power consumption, expanding the use of data converters across diverse environments.

Restrictions

Despite strong demand, the data converters market faces challenges related to design complexity and cost pressures. High-resolution and high-speed converters require sophisticated architectures, increasing development time and R&D investment. Power consumption and heat dissipation remain critical concerns, particularly in portable and battery-operated devices. Moreover, price competition among semiconductor vendors can compress margins, while supply chain disruptions and dependency on advanced fabrication nodes may impact production stability and lead times

Opportunities

Emerging applications present indicates significant growth opportunities for data converter manufacturers. The expansion of 5G and future 6G communication networks drives demand for ultra-fast and low-latency converters. Healthcare applications, including medical imaging, wearable diagnostics, and remote patient monitoring, require high-precision and low-noise signal conversion. The rise of edge computing and AI-enabled devices also increases the need for efficient data converters capable of handling large data volumes locally. Furthermore, electric vehicles and renewable energy systems create opportunities for robust converters in power management and control systems.

Challenges

The data converters industry faces challenges in balancing performance, power efficiency, and cost within increasingly compact designs. As signal frequencies rise, maintaining accuracy and minimizing noise becomes more difficult, particularly in harsh industrial or automotive environments. Rapid technological evolution requires continuous innovation, placing pressure on vendors to shorten product development cycles. Additionally, compliance with stringent quality and reliability standards in aerospace, defense, and medical applications adds complexity to manufacturing and certification processes.

Data Converters Market Trends

Key trends shaping the market include the integration of data converters into system-on-chip (SoC) designs, reducing footprint and improving performance. There is growing demand for low-power converters optimized for wearable and IoT devices. Automotive trends such as autonomous driving consideration and vehicle electrification are driving adoption of high-speed, multi-channel converters. Sustainability is also gaining importance, with manufacturers focusing on energy-efficient designs and optimized manufacturing processes. Strategic collaborations and acquisitions among semiconductor companies are strengthening portfolios and accelerating innovation.

Key Players in the Global Data Converters Industry

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Infineon Technologies AG

- STMicroelectronics

- Microchip Technology Inc.

- Renesas Electronics Corporation

- NXP Semiconductors

- Maxim Integrated

- ON Semiconductor

- ROHM Semiconductor

Regional & Country Analysis

North America represents a major market for data converters, supported by strong presence of semiconductor companies, advanced R&D ecosystems, and high adoption of industrial automation and defense technologies. Europe maintains steady growth driven by automotive electronics, industrial control systems, and stringent quality standards. Asia-Pacific dominates the global market as the largest manufacturing hub for consumer electronics, semiconductors, and automotive components, with China, Japan, South Korea, and Taiwan leading production and consumption. Latin America and the Middle East & Africa exhibit emerging growth potential as industrialization, telecommunications expansion, and infrastructure development accelerate.

Segmentation Highlights

The data converters market demonstrates clear segmentation trends. By type, ADCs lead due to widespread use in sensing, imaging, and communication applications, while DACs remain essential in audio, video, and control systems. By resolution, 8–16-bit converters capture the largest share, balancing cost and performance, while above 16-bit converters grow rapidly in precision-critical applications. Consumer electronics dominate application demand, while automotive and industrial segments show the highest growth rates. OEMs represent the primary end users, supported by long-term supply agreements and integrated design requirements.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 15.7 billion |

|

Market CAGR |

8.5% |

| By Type | Analog-to-Digital Converters, Digital-to-Analog Converters |

|

By Resolution |

Up to 8-bit, 8–16-bit, Above 16-bit |

|

By Application |

Consumer Electronics, Automotive, Industrial, Telecommunications, Healthcare, Aerospace & Defense, Others |

|

By End User |

OEMs, Aftermarket |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Data Converters Market: Key Players |

Analog Devices, Inc. Texas Instruments Incorporated Infineon Technologies AG STMicroelectronics Microchip Technology Inc. |

Global Data Converters Industry Instances

- Consumer electronics manufacturers integrated advanced ADCs for high-resolution imaging and audio processing.

- Automotive OEMs adopted high-speed converters for ADAS and electric vehicle control systems.

- Industrial firms deployed data converters in smart factories and predictive maintenance solutions.

- Healthcare companies utilized precision converters in medical imaging and wearable monitoring devices.

Analyst Review

As per our Data Converters Market analysis report, market is poised for sustained growth as digital transformation accelerates across industries. While design complexity and pricing pressures pose challenges, continuous innovation in mixed-signal integration, power efficiency, and high-speed performance is expanding application scope. Companies that focus on advanced R&D, application-specific solutions, and long-term partnerships with OEMs are expected to maintain a competitive edge through 2035.

Frequently Asked Questions (FAQ):

The data converters market encompasses Analog-to-Digital Converters (ADCs) and Digital-to-Analog Converters (DACs) that transform analog signals (e.g., sound, temperature) into digital data and vice versa. According to Fatpos Global, it's vital for signal processing in consumer electronics, automotive, and industrial sectors.

Fatpos Global projects the global data converters market to reach USD 15.7 billion by 2035, growing at a CAGR of 8.5% from 2023-2035, fueled by IoT expansion and 5G adoption.

Leading companies include Analog Devices, Inc., Texas Instruments Incorporated, Infineon Technologies AG, STMicroelectronics, Microchip Technology Inc., Renesas Electronics Corporation, NXP Semiconductors, Maxim Integrated, ON Semiconductor, and ROHM Semiconductor, per Fatpos Global analysis.

Data converters enable data acquisition, sensing, communications, audio/video systems, and precision control. High-resolution types support medical imaging and aerospace, while mid-resolution ones dominate automotive and industrial uses.

Key drivers include rising demand for high-speed, low-power converters in EVs, AI, and edge computing. Fatpos Global highlights advancements in resolution and efficiency amid Industry 4.0 trends.

Select License Type

Select License Type