Third-Party Logistics (3PL) Research 2035

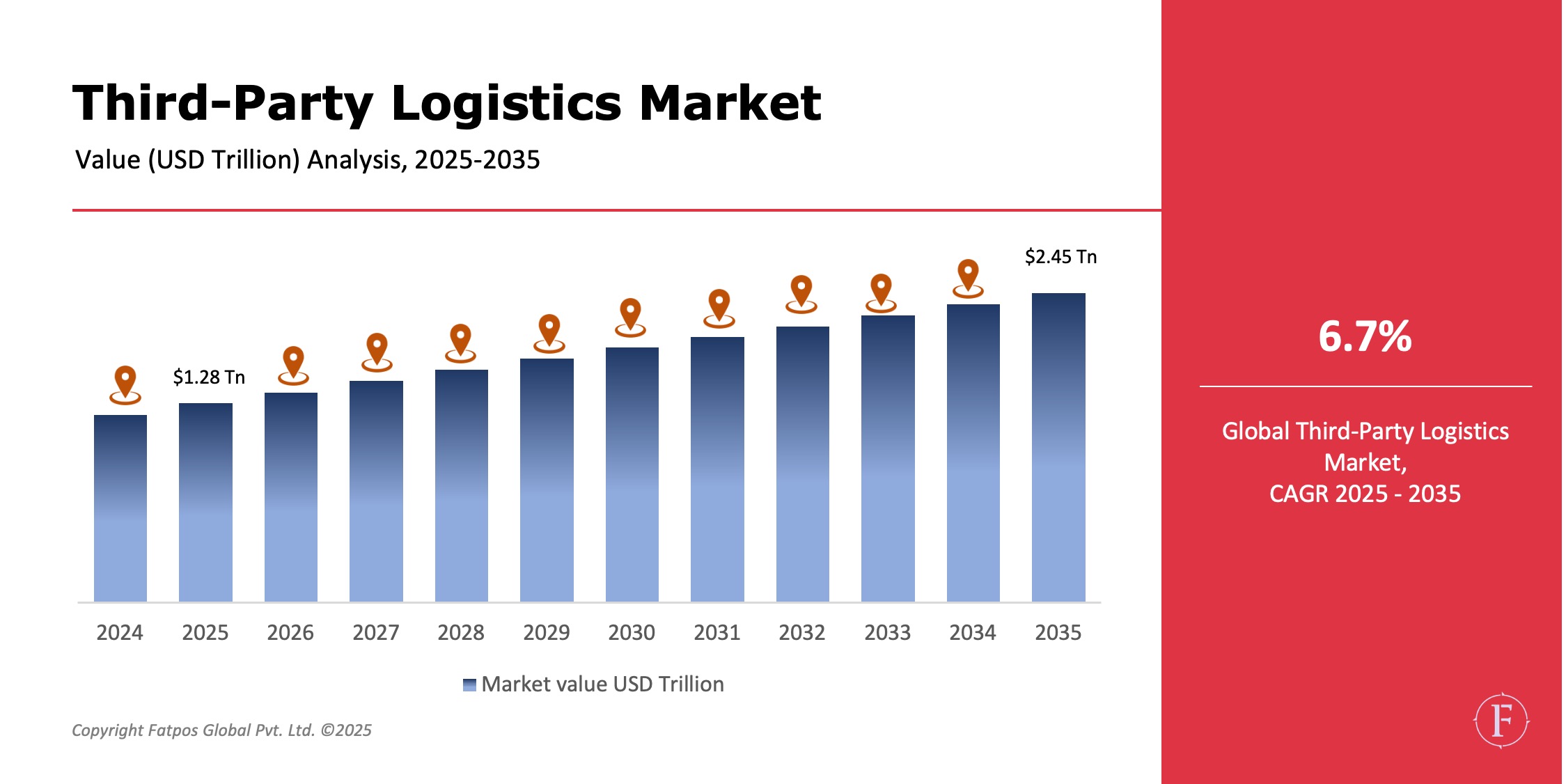

The Third-Party Logistics Market Size was USD 1.28 trillion in 2025 and is projected to reach USD 2.45 trillion by 2035, registering a CAGR of 10.4%, Market growth is driven by globalization of trade, rapid expansion of e-commerce, increasing outsourcing of logistics operations, growing complexity of supply chains, and rising demand for cost-efficient and scalable logistics solutions.

Third-party logistics providers manage transportation, warehousing, inventory management, order fulfillment, and value-added services on behalf of shippers. As companies increasingly focus on core competencies, outsourcing logistics functions to specialized 3PL providers has become a strategic necessity across industries.

Product Overview

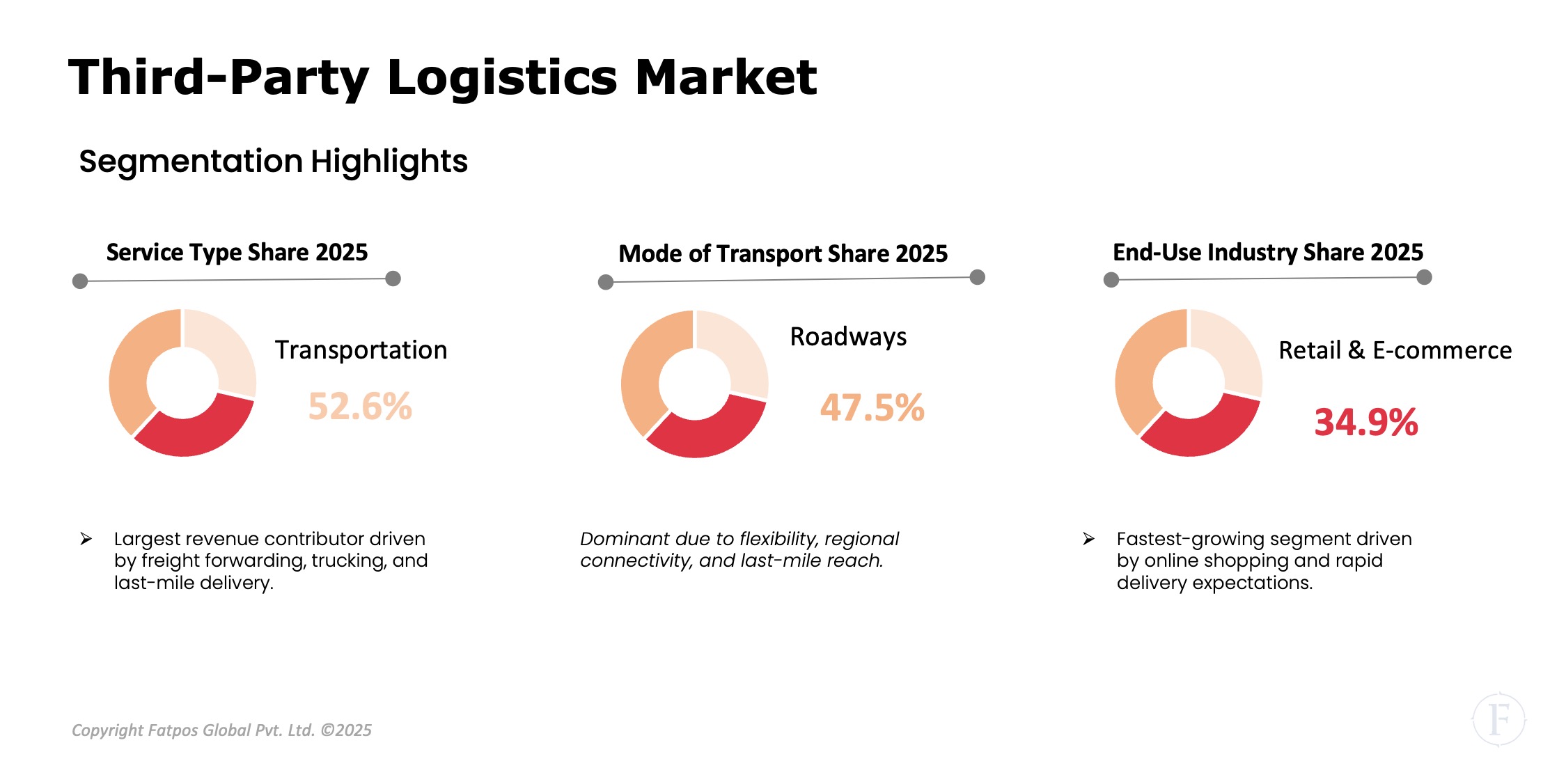

3PL services streamline end-to-end logistics, delivering efficiency, flexibility, and scalability for businesses outsourcing complex operations. By service type, transportation encompasses freight forwarding, brokerage, and last-mile delivery to optimize routes and costs; warehousing & distribution handles storage, inventory tracking, order picking, and fulfillment for seamless supply chains; Value-added services include packaging, labeling, reverse logistics, customs brokerage, and kitting to enhance customer satisfaction. By transport mode, roadways lead with versatile last-mile access; railways excel in economical long-haul bulk movement; waterways support global bulk trade; and airways prioritize urgent, high-value cargo.

Key Takeaways :

- The Third-Party Logistics Market is expected to grow at ~6.7% CAGR through 2035.

- Transportation services account for the largest revenue share.

- Retail & e-commerce is the fastest-growing end-use segment.

- Increasing adoption of digital logistics platforms and automation.

- Asia-Pacific is the fastest-growing regional market.

- Sustainability and green logistics are becoming key competitive differentiators.

Market Dynamics

Drivers

The emergence in global and cross-border e-commerce propels 3PL demand as retailers scale fulfillment for same-day deliveries and international shipments. Businesses increasingly seek cost reductions and efficiency gains amid rising fuel prices and labor shortages, outsourcing to 3PL providers for optimized routing and inventory control. Supply chain complexity from omnichannel retail—spanning online, stores, and pop-ups—requires specialized handling that 3PLs master through integrated networks. Booming international trade and manufacturing output, especially in Asia, amplify freight volumes, while AI, IoT sensors, and data analytics adoption enables predictive demand forecasting, real-time tracking, and automated warehousing for resilient operations.

Restrictions

3PL providers grapple with escalating operational costs, as volatile fuel prices and persistent labor shortages—exacerbated by driver deficits and wage pressures—erode margins despite efficiency gains. Infrastructure bottlenecks plague developing regions, where inadequate roads, congested ports, and limited rail networks delay shipments and inflate expenses in high-growth markets like India and Africa. Regulatory complexities compound challenges, with divergent customs rules, trade tariffs, compliance standards, and Brexit-style border shifts across 190+ countries demanding constant adaptation, documentation, and expertise to avert purposes and disruptions in global supply chains.

Opportunities

The 3PL sector advances through specialized expansions and technological upgrades. Cold chain and healthcare logistics surge with temperature-controlled transport for vaccines, perishables, and biologics, ensuring compliance amid global health demands. Last-mile delivery and urban logistics boom from e-commerce, deploying micro-fulfillment centers and electric fleets to conquer "last meter" challenges in dense cities. Warehouse automation, robotics for picking/packing, and AI-driven route optimization slash errors by 30% and boost throughput, enabling same-day service scalability. Rising reverse logistics and returns management—now 30% of e-commerce orders—leverage data analytics for efficient processing, refurbishment, and resale loops.

Challenges

3PL providers face mounting challenges in a volatile landscape. Supply chain disruptions—from geopolitical tensions, natural disasters, and pandemics—strain capacity constraints, forcing reliance on diversified sourcing, nearshoring, and flexible contracts to maintain flow. Ensuring end-to-end visibility demands blockchain, IoT trackers, and unified dashboards, bridging silos across global networks for real-time decisions and customer trust. Intense competition erodes margins as hyperscalers and asset-light players undercut prices, compelling 3PLs to differentiate via tech investments, sustainability, and value-added services amid commoditized freight rates.

Third-Party Logistics Market Trends

The 3PL industry accelerates with e-commerce fulfillment and last-mile innovations, powering same-day deliveries through micro-hubs and drone pilots to meet soaring consumer expectations. Digital freight platforms and real-time tracking via IoT unify visibility, slashing delays by 25% and enabling dynamic rerouting. Sustainability gains traction with electric fleets, biofuels, and carbon-neutral warehousing, aligning with ESG mandates. Contract logistics expands into end-to-end supply chains, bundling procurement and after-sales. Strategic M&A among giants like DHL and Kuehne+Nagel consolidate scale, tech stacks, and global reach for competitive dominance.

Key Players in the Global Third-Party Logistics Industry

- DHL Supply Chain & Global Forwarding

- Kuehne + Nagel

- DB Schenker

- DSV A/S

- C.H. Robinson

- XPO Logistics

- UPS Supply Chain Solutions

- FedEx Logistics

- GEODIS

- Expeditors International

- Nippon Express

- CEVA Logistics

Regional & Country Analysis

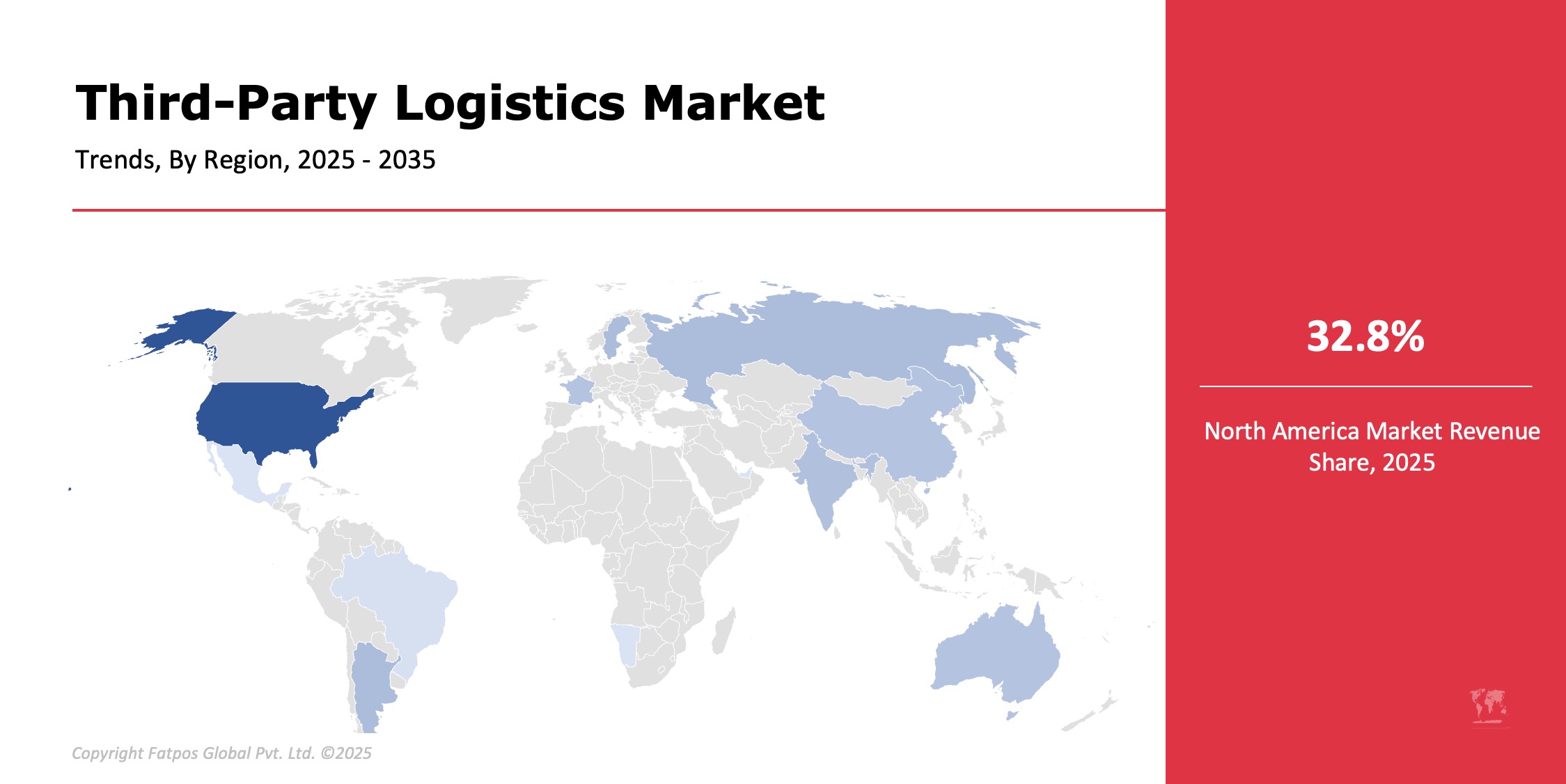

North America commands the largest 3PL market, fueled by cutting-edge logistics infrastructure, deep e-commerce penetration, and rapid technology adoption in automated warehouses and AI routing. Europe sustains a mature landscape through robust cross-border trade, stringent regulations, and emerging contract logistics for automotive and retail sectors. Asia-Pacific races ahead as the fastest-growing region, propelled by manufacturing booms, burgeoning consumer markets, and explosive e-commerce in China and India. Latin America posts moderate gains via upgraded trade corridors and retail expansion, while Middle East & Africa unlock emerging potential through strategic logistics hubs, port modernizations, and infrastructure megaprojects.

Segmentation Highlights

The 3PL market segments reveal distinct leadership and growth patterns. By service type, transportation commands the largest share through freight management, while warehousing & value-added services like fulfillment and reverse logistics accelerate with e-commerce demands. Roadways dominate transport modes for their last-mile versatility, bolstered by rail for bulk efficiency and waterways for cost-effective global trade. Retail & e-commerce drives end-use volume and fastest expansion, outpacing manufacturing. B2B verticals hold sway via complex supply chains, but B2C emerges rapidly from direct-to-consumer models and same-day delivery expectations.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Market Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 2.45Tn |

|

Market CAGR |

6.7% |

| By Service Type | Transportation, Warehousing & Distribution, Value-Added Services |

|

By Mode of Transport |

Roadways, Railways, Waterways, Airways |

|

By Industry Vertical |

B2B, B2C |

|

By End User |

Retail & E-commerce, Manufacturing, Automotive, Healthcare, Food & Beverage, Chemicals, Others |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Third-Party Logistics: Key Players |

DHL Supply Chain & Global Forwarding, Kuehne + Nagel, DB Schenker, DSV A/S, CH Robinson. |

Global Third-Party Logistics Industry Instances

- E-commerce companies outsourced end-to-end fulfillment operations to 3PL providers.

- Logistics firms deployed AI-driven route optimization and warehouse automation.

- Healthcare companies expanded cold chain logistics partnerships.

- Global 3PLs invested in sustainable fleets and green warehouses.

Analyst Review

As per our Third-Party Logistics Market analysis report, market is evolving rapidly as supply chains become more complex, digital, and customer-centric. While cost pressures and operational challenges persist, advancements in automation, analytics, and integrated logistics solutions are enabling 3PL providers to deliver greater value. Companies that invest in technology, sustainability, and sector-specific expertise are expected to lead market growth through 2035.

Frequently Asked Questions (FAQ):

Outsourced logistics services including transportation, warehousing, and fulfillment.

E-commerce expansion, globalization, and supply chain complexity.

Transportation services.

Asia-Pacific.

Steady growth driven by digitalization and outsourcing trends.

Select License Type

Select License Type