Driverless Car Market Research 2035

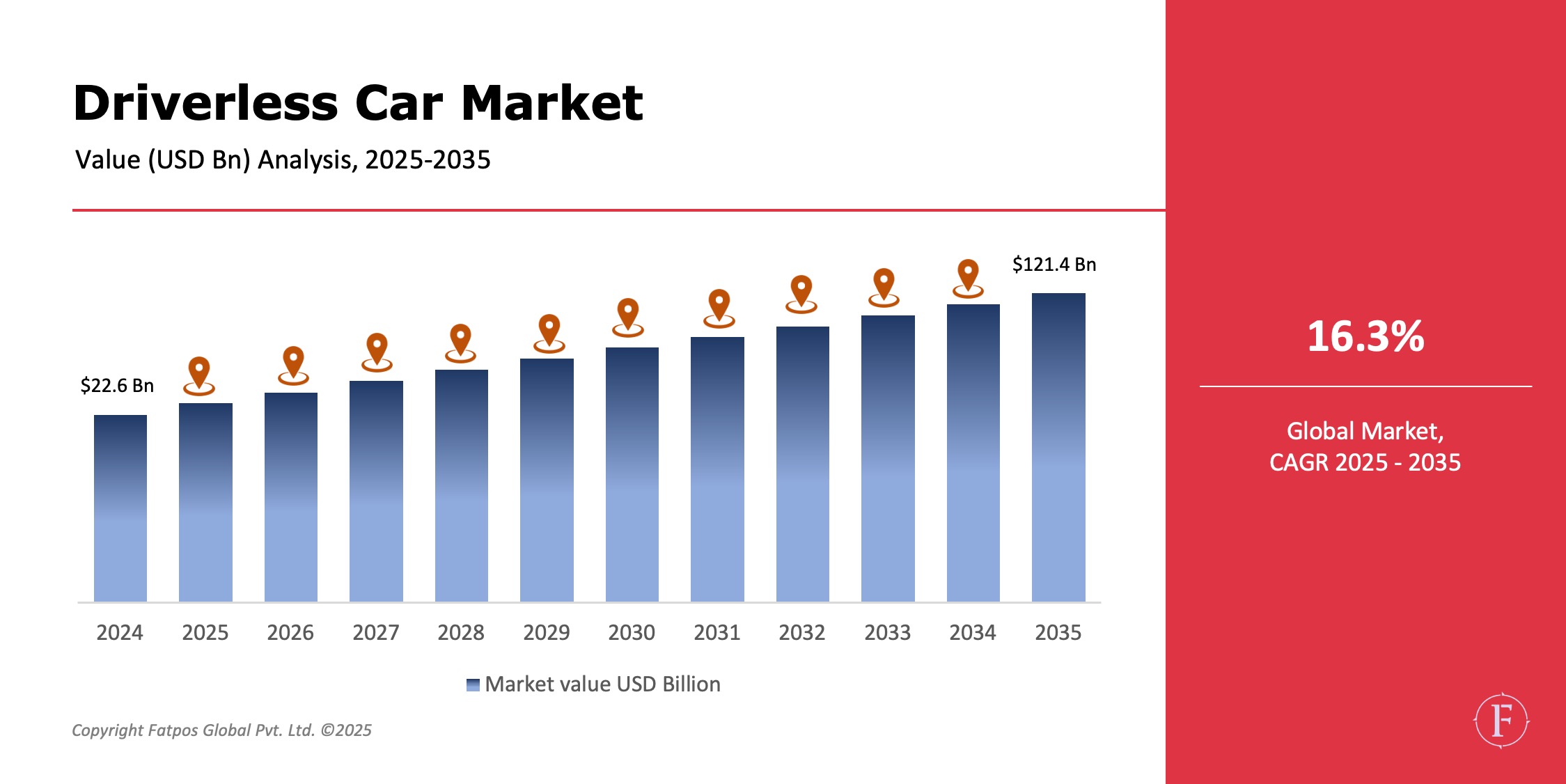

Driverless Car Market is undergoing a transformative shift as advancements in artificial intelligence, sensor fusion, onboard computing, and connectivity reshape how the world approaches mobility. The global market reached USD 22.6 billion in 2024 and is projected to expand significantly, reaching USD 121.4 billion by 2035, at a CAGR of 16.3% during the forecast period. What was once a futuristic concept is now becoming reality as fully autonomous systems begin to appear in controlled commercial environments across North America, China, Japan, the UAE, and parts of Europe.

Product Overview

Driverless cars also referred to as autonomous vehicles (AVs) use a combination of high-precision LiDAR, radar, cameras, ultrasonic sensors, AI decision engines, HD mapping, machine learning, and V2X (vehicle-to-everything) communication. These components work together to interpret traffic environments, avoid obstacles, and execute maneuvers with minimal human involvement. Automation levels range from L1 (driver assistance) to L5 (full automation). While Level 5 remains under research, Level 3 and Level 4 systems are now being tested on public roads and integrated into ride-hailing fleets.

Key Takeaways:

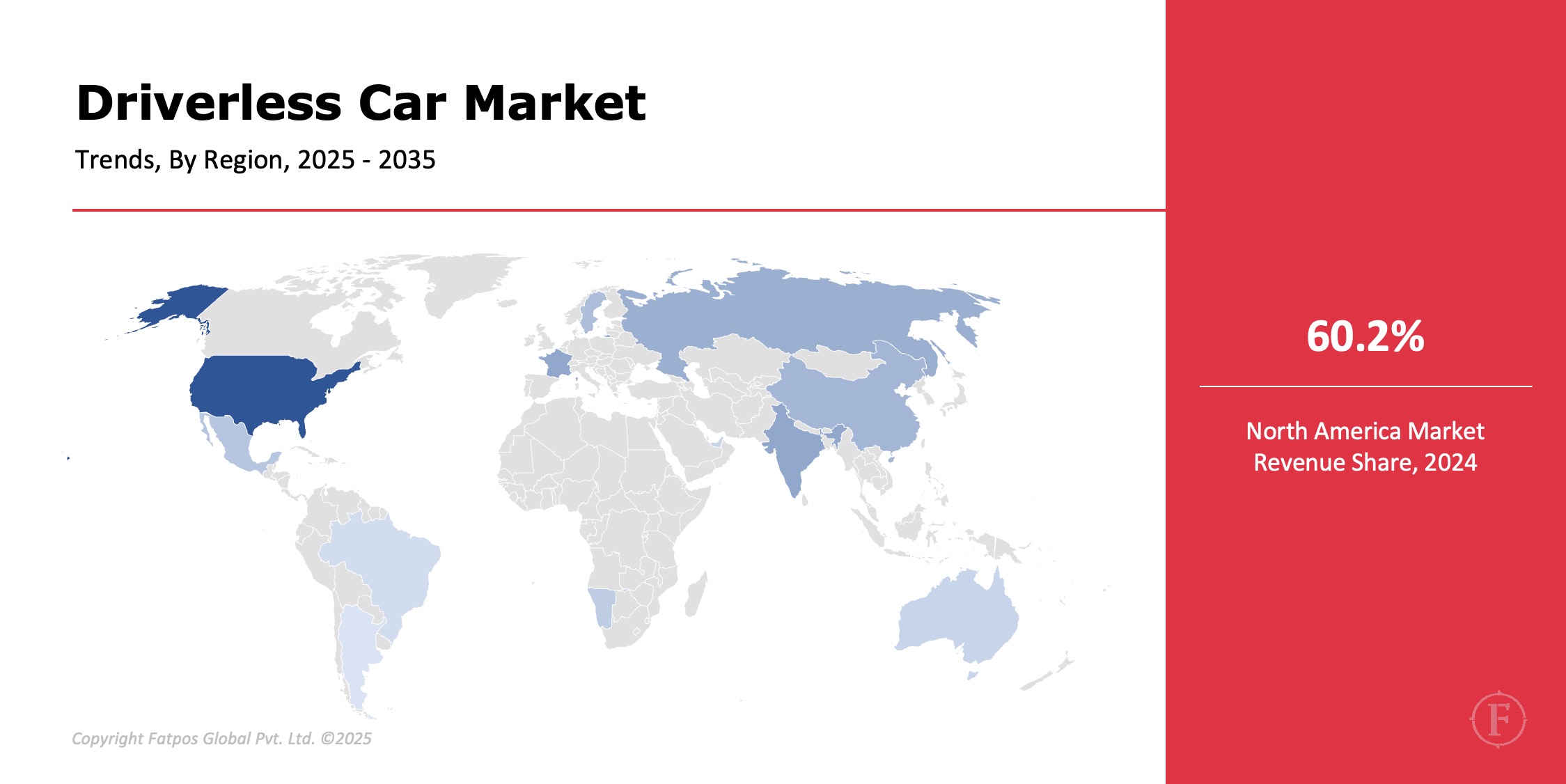

- The U.S. autonomous/driverless car vehicle market grows rapidly through incentives and supportive regulations, with North America capturing about 40–45% of early revenue share.

- Europe holds a major share of the autonomous car market in 2024, supported by strong safety regulations, ADAS mandates, and pilot robotaxi projects across Germany, France, and the UK.

- Asia-Pacific records the fastest CAGR of around 30–37% through 2035, led by large-scale deployments and investments in China, Japan, and South Korea.

- Level 2–3 systems and robotaxis lead adoption, with Asia-Pacific and North America together accounting for well over half of global autonomous vehicle volumes.

- Mobility-as-a-Service and logistics applications capture major growth, as fleets deploy driverless cars and robo‑delivery services to cut costs and emissions.

Market Dynamics

Drivers

Advances in AI, sensing, and computing are rapidly reshaping the driverless car market. Powerful chips running machine learning and computer vision let vehicles analyze data in milliseconds and react faster than humans, while high‑resolution LiDAR and 4D radar improve perception in difficult conditions. Combined with rising concern over global road deaths and emissions, these technologies are driving governments and consumers toward autonomous vehicles as a safer and more efficient transport option.

Restraints

The driverless car market is restrained by fragmented regulations, unclear liability, and high costs. Countries apply different rules to automation, testing, and accidents, slowing global rollout. Automakers must invest in expensive sensors, AI computing, and redundant safety systems, while deployment also depends on 5G connectivity, smart traffic management, and reliable road infrastructure that many regions still lack.

Opportunities

Autonomous mobility and driverless car market services such as robotaxis and delivery fleets are emerging as major revenue engines, with players like Waymo, Cruise, Baidu, Nuro, and Amazon piloting commercial deployments. At the same time, smart city programs, 5G‑enabled V2X networks, and government-funded autonomous shuttles and road infrastructure in markets like the UAE, Singapore, China, and the U.S. are accelerating adoption.

Threats

Autonomous cars introduce significant challenges in cybersecurity, data privacy, and public trust. Their cloud‑connected systems can be vulnerable to hacking, GPS spoofing, and sensor tampering, while always‑on cameras and LiDAR generate sensitive data that must be carefully protected. At the same time, high‑profile accidents can erode confidence, prompt stricter regulation, and slow deployment unless companies clearly demonstrate safety through transparent reporting, rigorous security, and strong safeguards for both vehicle systems and user data.

Driverless Car Market Trends

The driverless car market is scaling quickly, with global value expected to rise sharply over the next decade as governments push road‑safety, decarbonization, and smart‑city agendas. Autonomous ride‑hailing, logistics fleets, and advanced driver‑assistance features are the fastest‑growing applications, while AI, sensors, and connectivity form the core technology stack. North America and Asia‑Pacific lead large‑scale pilots and investments, positioning autonomous vehicles as a central pillar of future intelligent, low‑emission mobility systems.

Key Players in the Driverless Car Market Industry

- Tesla

- Waymo (Alphabet)

- General Motors

- Volkswagen

- Toyota

- BMW

- Ford

- Uber

- Zoox

- Aurora

Regional & Country Analysis

North America

North America is the leading autonomous driving hub, with the U.S. generating most regional revenue and hosting large-scale trials by major AV and AI companies. Its strong AI ecosystem, EV infrastructure, and flexible regulation support Level 4 robotaxi pilots across several states. Canada prioritizes autonomous freight corridors, while Mexico is gradually adopting advanced driver‑assistance systems as a step toward full autonomy.

Europe

Europe is shaping the future of autonomous mobility through clear regulation and coordinated EU policy. Germany has legalized Level 4 driving for commercial use, allowing OEMs like Mercedes‑Benz, BMW, and Volkswagen to run autonomous fleets. France and the UK advance shuttles and logistics robotics, while the EU’s AI Act and roadmap guide cybersecurity, certification, and ethical AI, with Sweden and the Netherlands emerging as driverless car market key testing hubs.

Asia-Pacific

Asia-Pacific is the fastest‑growing autonomous driving region, led by China’s large‑scale robotaxi deployments in cities like Beijing, Shanghai, and Shenzhen through platforms such as Baidu Apollo and Pony.ai. Japan emphasizes autonomous public transport to support its aging society, while South Korea leverages strengths in sensors, semiconductors, and automotive AI. India remains in an early phase but is investing in smart roads, ADAS capabilities, and digitally integrated mobility to prepare for higher automation levels.

Middle East & Africa

The UAE leads regional adoption with Dubai aiming for 25% of transportation to be autonomous by 2035. Regulatory readiness, modern infrastructure, and strong partnerships with global AV providers make the UAE a prime market. Saudi Arabia is also building autonomous-ready cities such as NEOM, designed around driverless mobility.

Africa is at the earliest stage of adoption but is experimenting with autonomous shuttles in Rwanda and South Africa.

Latin America

Latin America is gradually entering autonomous mobility through ADAS-based vehicles and AI-supported logistics systems. Brazil and Mexico are improving their EV and AI ecosystems, creating future opportunities for automated fleets. Challenges include infrastructure limitations and slower regulatory readiness.

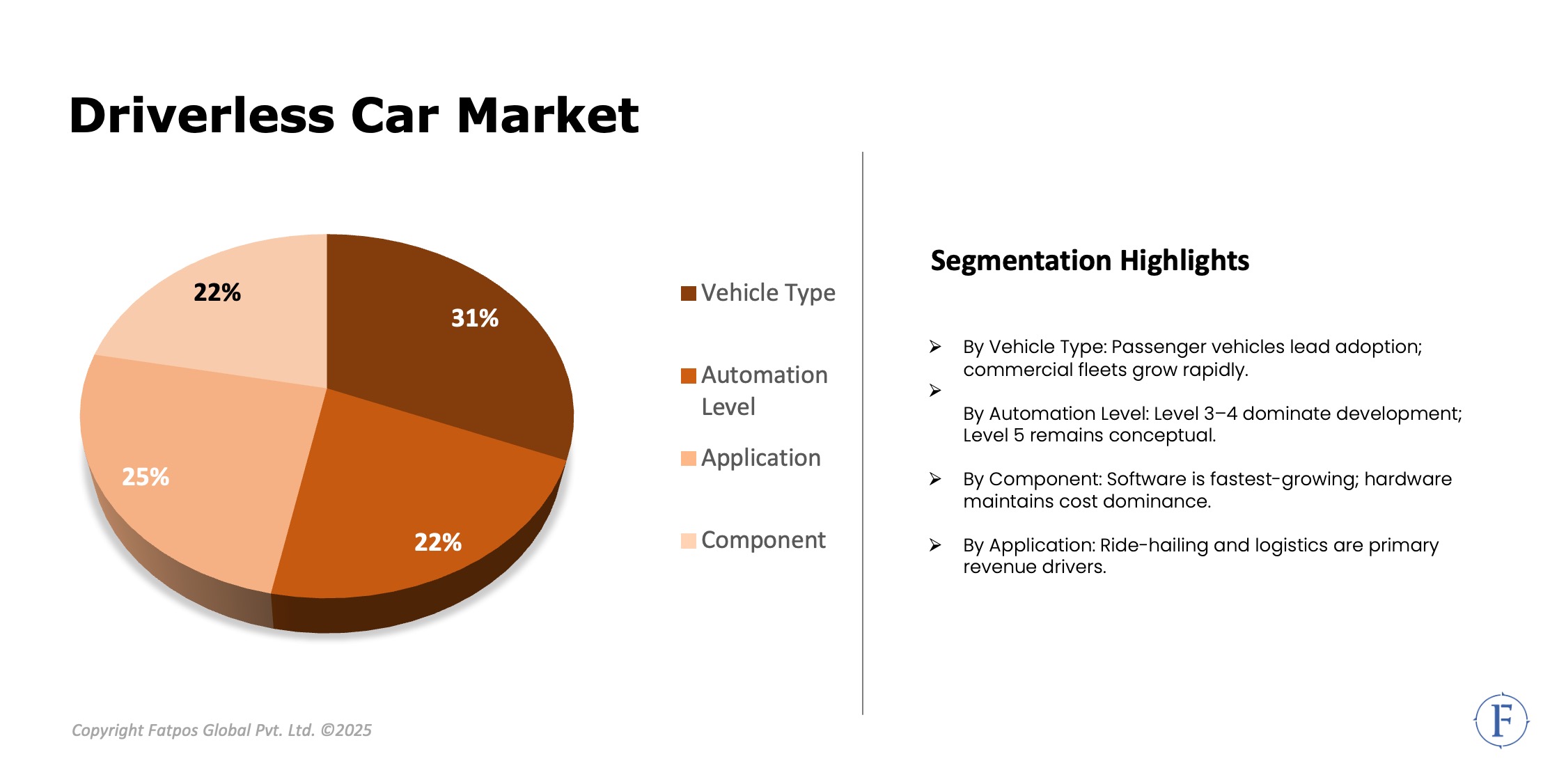

Segmentation Highlights

Passenger vehicles dominate the driverless car market, as consumers and robotaxi fleets prioritize autonomous cars for comfort, safety, and flexibility. Semi‑autonomous (Level 1–2) systems currently hold the largest share because they build on existing ADAS features and are easier to commercialize at scale. Higher‑automation Levels 3–4 are the fastest‑growing segment, led by robotaxis, autonomous shuttles, and logistics fleets in urban corridors and controlled environments.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Driverless Car Market Size by 2035 |

USD 121.4 billion |

|

Market CAGR |

16.3% |

|

By Vehicle Type |

Passenger, Commercial |

|

By Automation Level |

L1–L5 |

|

By Component |

Hardware, Software, Services |

|

By Application |

Ride-hailing, Logistics, Personal Mobility, Robo-taxis |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Key Market Players |

Tesla, Waymo (Alphabet), General Motors, Volkswagen, Toyota, BMW, Ford |

Key Developments

- Waymo expanded operations in multiple U.S. cities, strengthening robotaxi validation.

- NVIDIA launched DRIVE Thor, a next-gen platform offering multi-domain compute.

- Baidu Apollo surpassed 2 million autonomous road miles, boosting its global credibility.

- Mercedes-Benz gained approvals for Level 3 driving in Europe, establishing a new benchmark.

Analyst Review

The market is transitioning from technological exploration to structured deployment. Over the next decade, driverless mobility will reshape transportation economics, logistics efficiency, and urban planning. The Driverless Car Market Analysis suggests that early adopters—supported by robust regulations, AI infrastructure, and public acceptance—will lead global commercialization. The industry’s next phase will be defined by collaborations among automakers, AI chipmakers, cloud providers, and governments.

Frequently Asked Questions (FAQ):

USD 22.6 billion in 2024.

The United States, followed by China and Japan.

Advancement in AI compute and sensor fusion technologies.

High cost, regulatory complexity, and cybersecurity risks.

Strong growth driven by autonomous fleets and logistics automation.

Select License Type

Select License Type