Simulation software market research, 2034

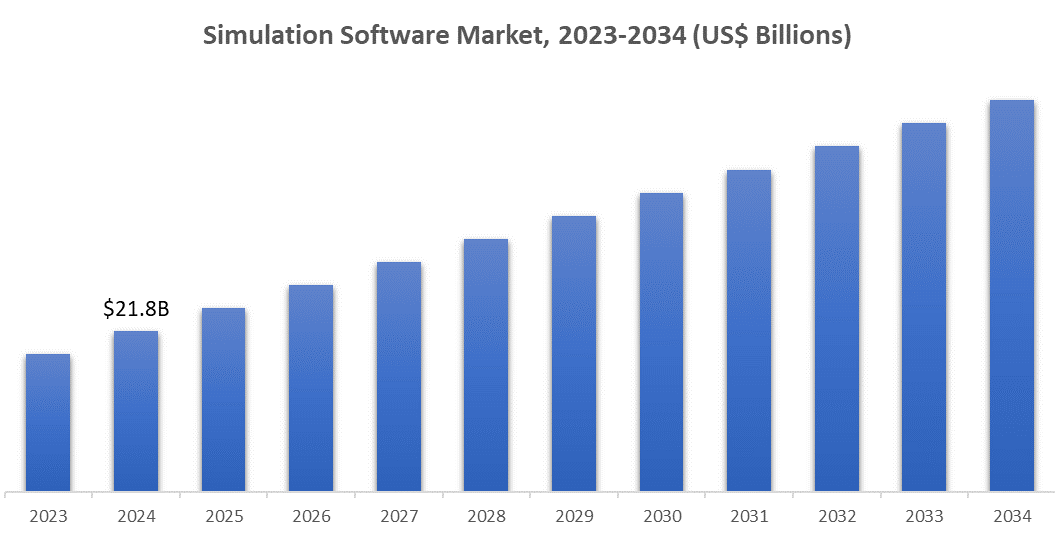

The global simulation software market is anticipated to grow at a CAGR of 12.8% in the forecast period (2024-2034), with the market size valued at US$ 19.4 billion in 2023 and projected to reach US$ 72.9 billion by 2034.

Simulation software is a digital program that emulates real-life systems and operations, allowing users to imitate and study behaviors in different scenarios. This software makes testing designs, workflows, and scenarios easier, without the requirement for any type of physical prototypes or risking resources.

Simulation software can replicate engineering systems, manufacturing processes, logistics, and human interactions in virtual environments through the use of advanced algorithms, 3D modeling, and real-time data. It is commonly utilized in various sectors like automotive, aerospace, healthcare, and IT to enhance performance, lower expenses, and innovate efficiently. The combination of AI and digital twins has broadened its range, becoming a crucial tool in Industry 4.0.

Market Highlights

The market is expected to grow due to the rising demand for affordable solutions for product development and testing. Businesses are using this software to lower costs associated with physical prototyping and accelerate the time it takes to bring products to market. The increasing prominence of Industry 4.0, AI-based analytics, and IoT has made simulation tools more widely used, as they allow for instant process improvement and predictive maintenance.

Additionally, the recent developments in cloud computing and high-performance computing (HPC) have increased the accessibility and capability of simulation software. Strong future growth is anticipated to stem from autonomous systems, healthcare, and digital twins relying more on simulation technologies. The growing use of virtual training in different industries is also spurred by the emergence of markets in Asia-Pacific.

Market Segmentation

Software-based products are expected to dominate the market, given their widespread application in modeling, analysis, and design across verticals

The market is segmented based on the Component into Software and Services. The software sector holds the largest market share as it is widely used in various industries for modeling, analysis, and design purposes. Simulation tools such as ANSYS, Simcenter, and MATLAB, whether used independently or together, enable companies to enhance processes, cut down on prototyping expenses, and enhance effectiveness.

Improvements in AI, machine learning, and real-time data analytics have significantly boosted the capabilities of simulation software, making it essential for intricate industrial uses. Additionally, the increased use of cloud-based solutions is leading to higher adoption rates by eliminating the necessity for complex infrastructure, enabling scalability and cost savings.

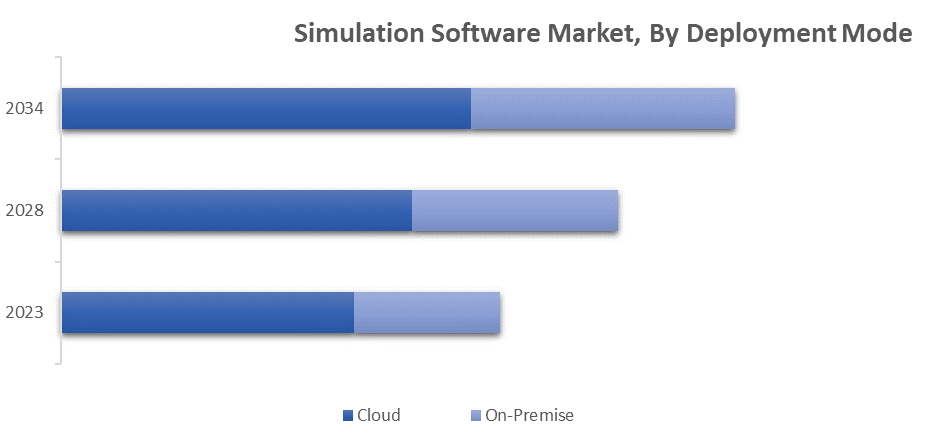

Cloud Segment to lead the market due attributed to its flexibility, scalability, and cost-effectiveness

The market is classified based on the Deployment Mode into On-Premise and Cloud. The cloud-based deployments lead the market holding the dominant position, attributed to their flexibility, scalability, and cost-effectiveness. Cloud-based simulation software removes the necessity for costly on-site infrastructure, allowing convenient access from any location at reduced operational expenses.

This deployment mode is perfect for situations involving collaboration and remote work, which have become essential after COVID-19. Cloud solutions make it easier to have real-time updates, integrate with IoT smoothly, and access advanced features such as AI-driven simulations. The growing use of SaaS models is boosting its appeal, particularly for SMEs and businesses looking into agile processes.

Market Dynamics

Growth Drivers

Growing Focus on Industry 4.0 and IoT to Propel Market Growth

Simulation software plays a crucial role in the execution of Industry 4.0 tactics by aiding in predictive maintenance, optimizing processes, and allocating resources. Integration of IoT allows immediate exchange of data between physical systems and digital models, facilitating accurate simulations of industrial settings.

This has increased the demand in manufacturing, logistics, and energy industries, where efficiency and saving money are crucial. With the increasing use of IoT, simulation software is playing a larger role in the growth of smart factories and connected systems, leading to significant market expansion.

Increasing Use of Digital Twins to Drive Expansion of Simulation-Based Software Market

Digital twins, which are also referred to as virtual duplicates of physical assets, depend significantly on simulation software for offering immediate insights, forecasting failures, and improving overall performance. This technology is commonly used in the aerospace, automotive, and healthcare industries, helping companies increase efficiency and cut down on downtime.

The increasing digital transformation in various sectors has heightened the reliance on digital twins, making simulation software essential for industries focusing on operational excellence and innovation.

Restraints

High Initial Deployment Costs May Hinder Market Growth

One of the most prevalent obstacles to market growth is the expensive deployment of video sensor systems. Significant funds are required to set up the essential infrastructure, which includes high-quality cameras, advanced sensors, and processing units. Furthermore, incorporating AI and IoT technologies in video sensors increases expenses even more. SMEs and developing regions encounter difficulties in implementing these solutions owing to several budgetary restrictions.

Regular maintenance and updates of both hardware and software contribute to the overall operational expenses. This restriction hinders access to the market, especially in less economically developed areas, but improvements in technology and economies of scale could eventually reduce these expenses.

Recent Developments

- In 2024, Ansys achieved a significant milestone with its Ansys Fluent fluid simulation software, leveraging 320 NVIDIA GH200 Grace Hopper Superchips scaled with NVIDIA Quantum-2 InfiniBand at the Texas Advanced Computing Center (TACC). This synergy between Ansys and NVIDIA enabled the solution of a 2.4-billion-cell problem, resulting in faster and higher-fidelity simulations that enhance R&D processes for innovative products. Furthermore, Ansys has formed a collaborative partnership with IonQ to integrate advanced quantum computing into engineering simulations.

- In 2024, Autodesk acquired Wonder Dynamics, incorporating cloud-based AI technology to facilitate the creation of 3D content across media and entertainment industries.

- Recently, Dassault Systèmes expanded its 3DEXPERIENCE platform with new simulation tools for digital twin creation. The company has also collaborated with Airbus to enhance aerospace design simulations.

- PTC Inc. released updates to Creo Simulation Live, integrating AI-driven simulation features. Additionally, the company formed a collaborative partnership with Microsoft to develop IoT-integrated simulation tools via Azure.

- In 2024, MathWorks entered into a collaboration with NXP Semiconductors to develop a Model-Based Design Toolbox for Battery Management Systems. Toyota Motors also expanded its use of MATLAB and Simulink to enhance its workflow and develop smarter cars.

Key Players:

- ANSYS Inc.

- Autodesk, Inc.

- Dassault Systèmes

- PTC Inc.

- MathWorks, Inc.

- Altair Engineering Inc.

- AspenTech (Aspen Technology, Inc.)

- SAP SE

- ESI Group

- Hexagon AB

- Bentley Systems Incorporated

- Siemens Digital Industries Software

- Simulia (A Dassault Systèmes Brand)

- Rockwell Automation, Inc.

- COMSOL Multiphysics

- Other Prominent Players (Company Overview, Business Strategy, Key Product Offerings, Financial Performance, Key Performance Indicators, Risk Analysis, Recent Development, Regional Presence, SWOT Analysis)

Regional Analysis

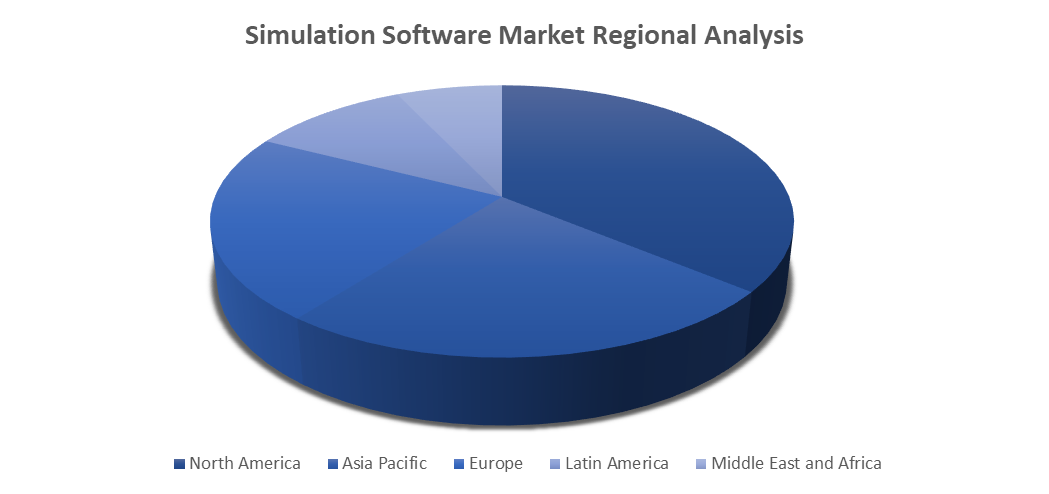

The global simulation software market is segmented based on regional analysis into five major regions: North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa.

North America tends to dominate the market accredited to its robust technological infrastructure and landscape, the early adoption of new solutions, and the significant presence of major companies such as ANSYS, Autodesk, and PTC. The area experiences a strong need for simulation in aerospace, automotive, and healthcare, along with substantial funding in AI and IoT technologies. Government efforts in supporting digital transformation and research and development are also driving market expansion.

The Asia-Pacific region is experiencing fast-paced growth, driven by the growing numbers of manufacturing centers in China, Japan, and India, supported by the rising investments in digital technologies.

Europe is closely monitoring sustainable manufacturing and automotive advancements.

Latin America and the Middle East & Africa (MEA) are experiencing slow growth, propelled by industrialization, urbanization, and emerging digital strategies in energy and mining industries.

Market is further segmented by region into:

- North America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United States and Canada

- Latin America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – Mexico, Argentina, Brazil, and Rest of Latin America

- Europe Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United Kingdom, France, Germany, Italy, Spain, Belgium, Hungary, Luxembourg, Netherlands, Poland, NORDIC, Russia, Turkey, and Rest of Europe

- Asia Pacific Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – India, China, South Korea, Japan, Malaysia, Indonesia, New Zealand, Australia, and Rest of APAC

- Middle East and Africa Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – North Africa, Israel, GCC, South Africa, and Rest of MENA

Market Scope and Segments:

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2018-2034 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2034 |

|

Historical Period |

2019-2022 |

|

Growth Rate |

CAGR of 12.8% from 2024-2034 |

|

Unit |

Value (US$ Billion) |

|

Segmentation |

Main Segments List |

|

By Component |

|

|

By Deployment |

|

|

By Application |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions (FAQ):

The global simulation software market size was valued at US$ 19.4 billion in 2023 and is projected to reach the value of US$ 72.9 billion in 2034, exhibiting a CAGR of 12.8% during the forecast period.

The market is the worldwide market for software that allows simulation, modeling, and analysis of different systems, processes, and phenomena. These solutions are implemented in various sectors like aerospace, automotive, healthcare, and manufacturing to enhance designs, cut costs, and enhance decision-making.

The Software and Cloud segment accounted for the largest market share.

Key players in the global simulation software market include ANSYS Inc., Autodesk, Inc., Dassault Systèmes, PTC Inc., MathWorks, Inc., Altair Engineering Inc., AspenTech (Aspen Technology, Inc.), SAP SE, ESI Group, Hexagon AB, Bentley Systems Incorporated, Siemens Digital Industries Software, Simulia (A Dassault Systèmes Brand), Rockwell Automation, Inc., COMSOL Multiphysics and Other Prominent Players.

Factors such as the growing use of digital twins, higher demand for IoT and AI technologies, increased need for simulation-based design and testing, and wider adoption of cloud-based simulation solutions are driving the market.

Select License Type

Select License Type