Mining Equipment Market Research 2035

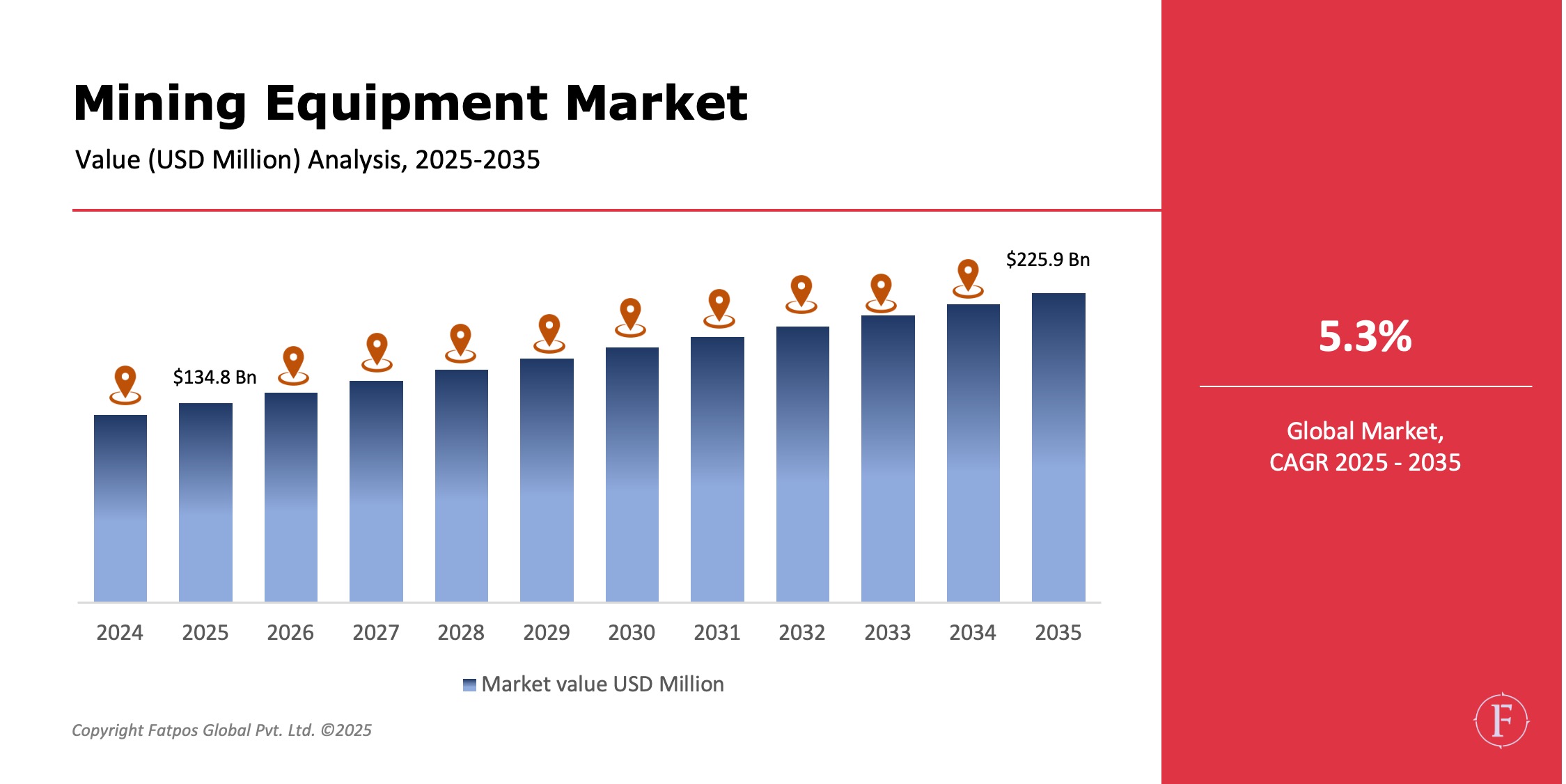

The Mining Equipment Market Size was USD 134.8 billion in 2025 and is projected to reach USD 225.9 billion by 2035, registering a CAGR of 5.3%, Key drivers include surging demand for minerals and metals amid infrastructure growth, renewable energy expansion, and EV supply chains, alongside mining modernization via automation and digital tech.

Essential for ore extraction, hauling, crushing, and processing, the sector is shifting toward electrification, automation, and sustainability. Companies prioritize energy-efficient, low-emission, digitally enabled equipment to boost productivity, safety, and environmental compliance.

Product Overview

Mining equipment encompasses heavy machinery for surface and underground operations. Surface types include excavators, haul trucks, loaders, bulldozers, draglines, and motor graders for open-pit mines. Underground features load-haul-dump (LHD) machines, underground trucks, roof bolters, longwall systems, and shuttle cars.

Crushing, pulverizing, and screening equipment—crushers, mills, screens—handles ore size reduction and processing. Drills and breakers cover rotary/blast hole drills, hydraulic breakers, and rock drills. Diesel dominates power sources, but electric and hybrid models surge for cost savings and emission cuts.

Key Takeaways:

- The Mining Equipment Market is expected to grow at ~5.3% CAGR through 2035.

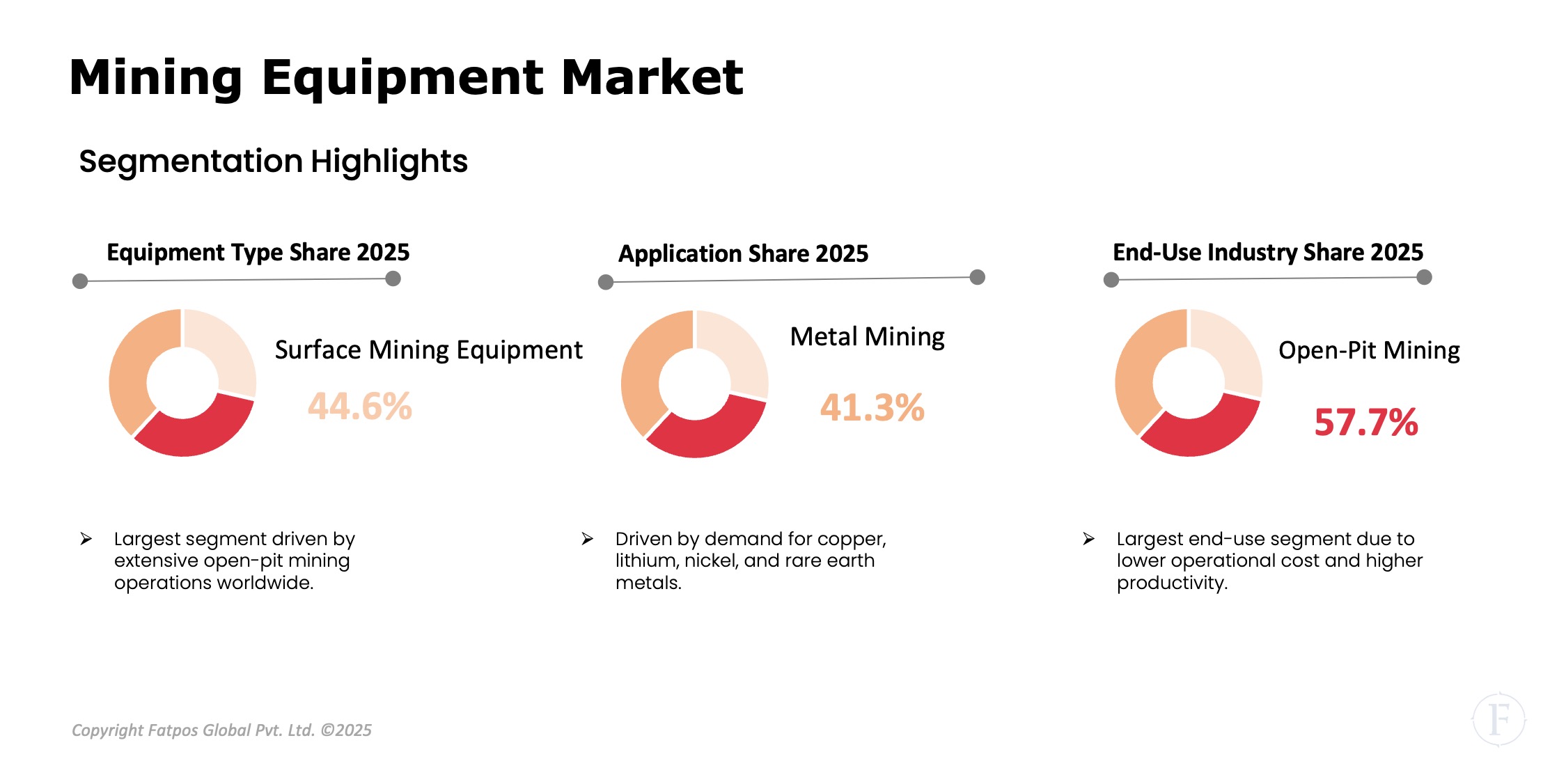

- Surface mining equipment holds the largest market share due to large-scale open-pit mining operations.

- Metal mining is a key growth segment, supported by demand for copper, lithium, nickel, and rare earth elements.

- Electrification and automation are reshaping equipment design and procurement strategies.

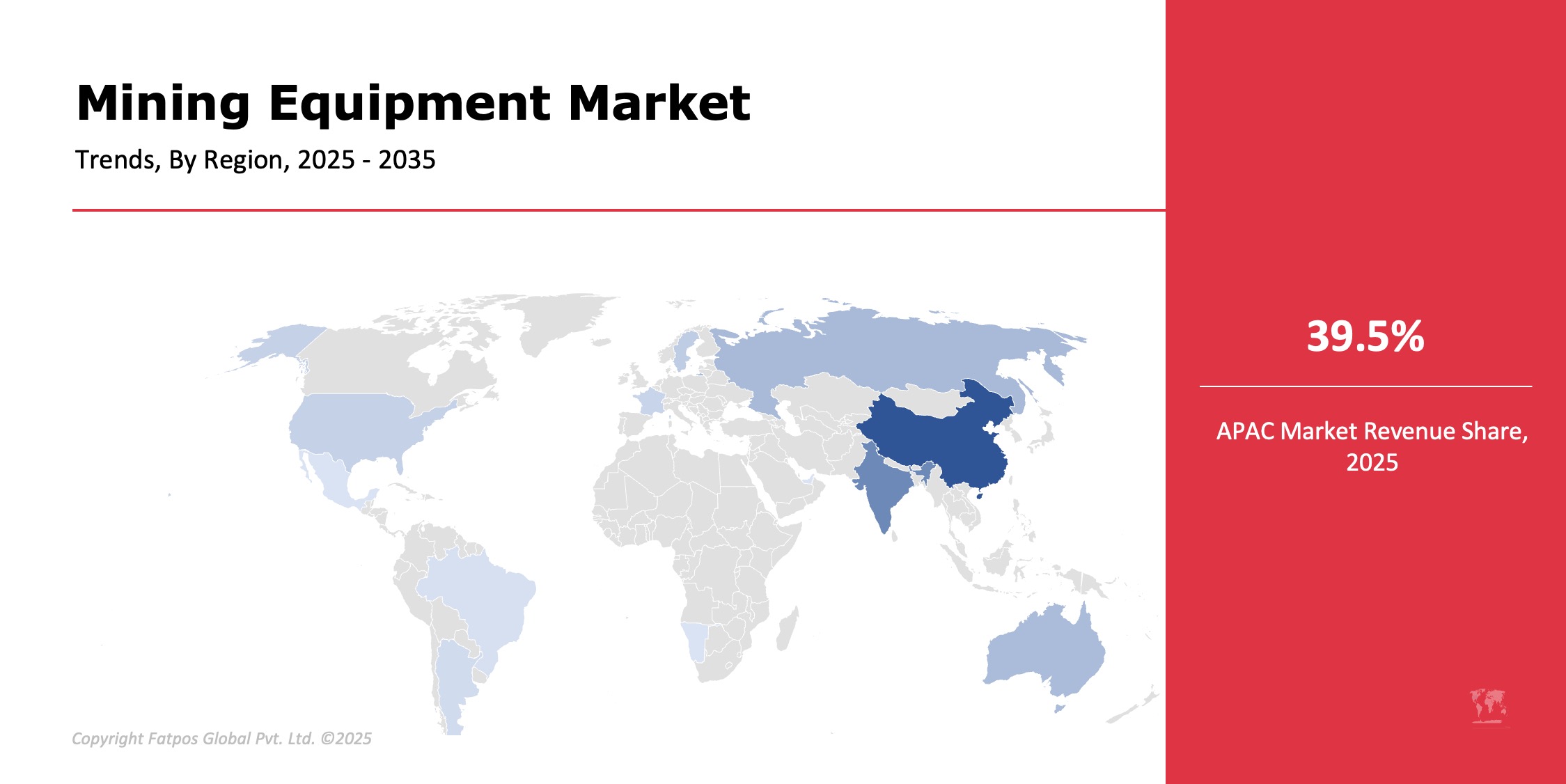

- Asia-Pacific dominates the market, while Latin America and Africa show strong growth potential.

Market Dynamics

Drivers

Rising global demand for metals and minerals drives the mining equipment market, supporting infrastructure development, renewable energy projects, and EV battery production. Expansion of open-pit and underground mining in emerging economies boosts equipment needs. Increasing adoption of automated and autonomous systems enhances productivity. A strong focus on worker safety and operational efficiency further propels investments in advanced machinery.

Restraints

High capital expenditure poses a major barrier to mining equipment procurement, requiring hefty initial outlays. Volatility in commodity prices disrupts mining investments, fostering hesitation. Stringent environmental regulations increasingly restrict diesel-based equipment, compelling shifts to sustainable options.

Opportunities

Growth in electric and hybrid mining equipment accelerates, slashing emissions and costs. Adoption of autonomous haulage systems (AHS) and smart solutions boosts efficiency and safety. Rising investments in digitalization and predictive maintenance minimize downtime. Expansion of critical mineral mining—lithium, copper, nickel—fuels demand.

Challenges

Equipment maintenance and downtime costs escalate operational expenses in harsh mining environments. Skill gaps hinder effective operation of advanced automated machinery, requiring extensive training. Supply chain disruptions delay equipment availability, impacting project timelines.

Mining Equipment Market Trends

The mining equipment sector shifts toward battery-electric and hybrid models, slashing carbon emissions and fuel costs while meeting regulatory demands. Increased deployment of autonomous trucks, drills, and loaders enhances safety by reducing human exposure in hazardous areas and boosts productivity through 24/7 operations.

Integration of AI, IoT, and data analytics enables real-time equipment monitoring, predictive maintenance, and optimized performance. Demand surges for modular, scalable equipment, allowing flexible mine planning and rapid adaptations to ore body changes.

OEM-mining company partnerships foster long-term service contracts, ensuring reliability, customized upgrades, and shared innovation in electrification and autonomy.

Key Players in the Global Mining Equipment Industry

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- Epiroc AB

- Hitachi Construction Machinery

- Liebherr Group

- Volvo Construction Equipment

- Doosan Infracore

- XCMG Group

- SANY Group

- Metso Outotec

- Terex Corporation

Regional & Country Analysis

Asia-Pacific commands the largest Mining Equipment market share, fueled by massive commercial North America benefits from mining modernization, automation demand, and critical mineral investments in the U.S. and Canada. Europe grows via technological innovation, sustainable practices, and robust OEM presence. Asia-Pacific reigns as the largest, fastest-expanding region, powered by vast activities in China, India, Australia, and Indonesia. Latin America sees strong gains from copper, lithium, and gold mining in Chile, Peru, and Brazil. Middle East & Africa offer emerging prospects through mineral exploration and infrastructure, especially in Africa.

Segmentation Highlights

Surface mining equipment leads the market, driven by large-scale open-pit operations that outpace underground gear, crushers/screens, and drills in dominance. Diesel power sources hold sway with reliable performance, but electric and hybrid options grow fastest, supporting decarbonization and cost efficiencies. Metal mining surges ahead as the quickest-expanding application, fueled by demand for energy transition metals like copper, lithium, and nickel vital for EV batteries and renewables. Open-pit mining captures the largest end-use share, leveraging scalability and productivity for vast deposits. These trends signal a broader pivot to efficient, green technologies amid intensifying global mineral needs.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Mining Equipment Market Forecast Period |

2025–2035 |

|

Mining Equipment Market Size by 2035 |

USD 225.9billion |

|

Market CAGR |

5.3% |

| Equipment Tyape | Surface Mining Equipment, Underground Mining Equipment, Crushing, Pulverizing & Screening Equipment, Drills & Breakers |

|

By Power Source |

Diesel, Electric, Hybrid |

|

By Application |

Coal Mining, Metal Mining, Mineral Mining |

|

By End User |

Open-Pit Mining, Underground Mining |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Key Market Players |

Caterpillar Inc., Komatsu Ltd., Sandvik AB ,Epiroc AB, Hitachi Construction Machinery, Liebherr Group |

Global Mining Equipment Industry Instances

- Mining companies deployed autonomous haul trucks to reduce labor costs and improve safety.

- Large copper mines adopted battery-electric underground loaders to cut emissions.

- OEMs launched AI-enabled predictive maintenance platforms for mining fleets.

- Lithium mining projects increased demand for advanced drilling and crushing equipment.

Analyst Review

As per our Mining Equipment Market analysis report, market is transitioning from conventional heavy machinery toward smart, electric, and autonomous systems. While capital intensity and commodity price volatility remain challenges, long-term demand for critical minerals, infrastructure expansion, and sustainability initiatives underpin steady market growth. OEMs investing in electrification, automation, and digital services are best positioned to capitalize on opportunities through 2035.

Frequently Asked Questions (FAQ):

Demand for minerals, infrastructure development, and mining automation.

Surface mining equipment due to extensive open-pit mining operations.

Electric and hybrid mining equipment.

Asia-Pacific.

Steady growth driven by automation, electrification, and demand for critical minerals.

Select License Type

Select License Type