Global Stainless Steel Market Research 2035

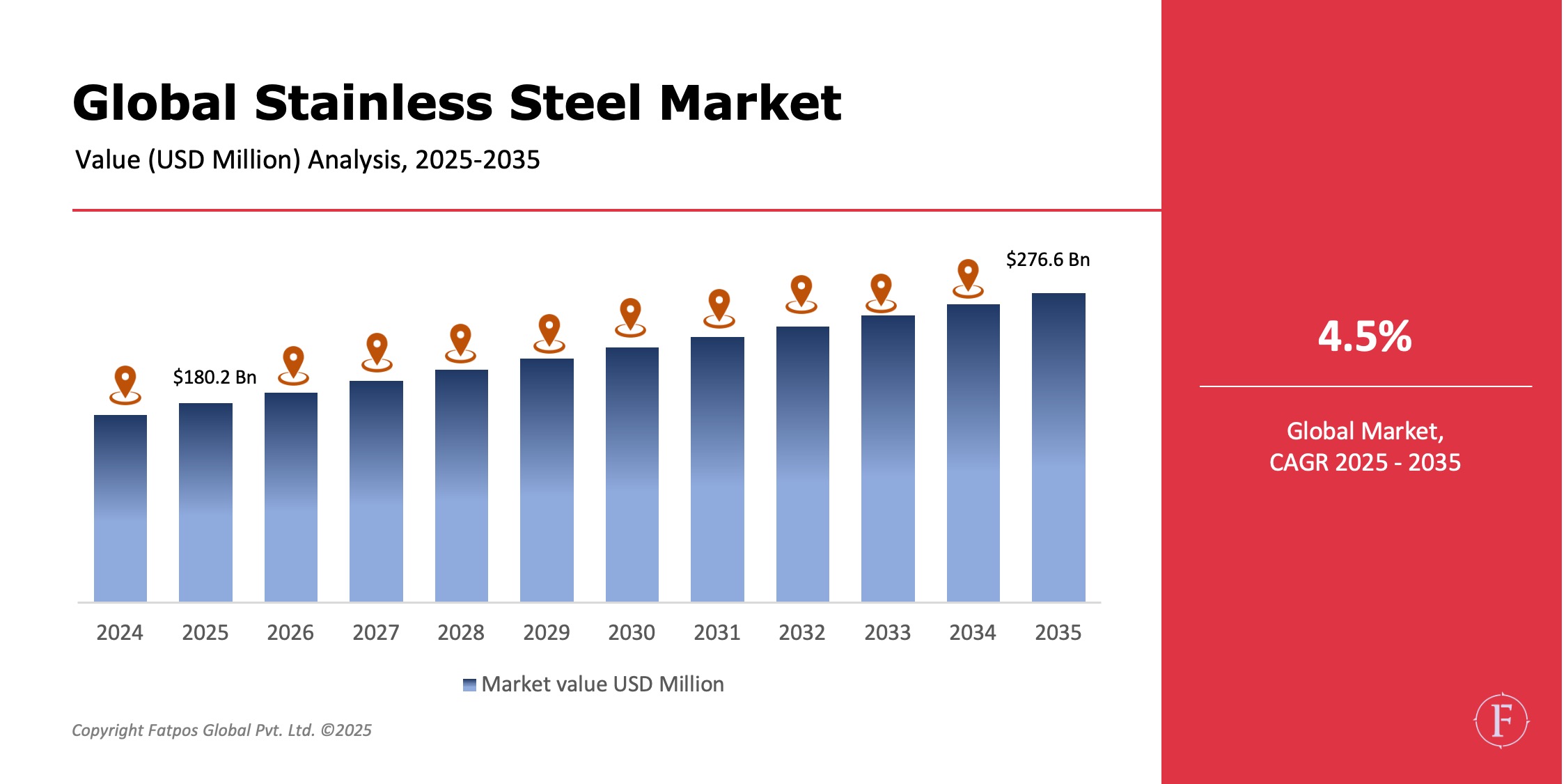

The Global Stainless Steel Market Size was USD 180.2 billion in 2025 and is projected to reach USD 276.6 billion by 2035, registering a CAGR of 4.5%, The market is a large, mature and strategically important sector serving infrastructure, mobility, energy, industrial and consumer applications. Demand should remain resilient over 2025–2035, supported by infrastructure investment, automotive lightweighting, industrial upgrades and growth in energy and chemical projects. Key drivers include rising use of duplex and higher-alloy grades in corrosive or high-stress conditions, expanding pipe and tube demand in energy and petrochemicals, and greater need for hygienic stainless surfaces in food, beverage and healthcare.

Product Overview

Stainless steel is a family of iron-based alloys with at least 10.5% chromium, which forms a passive film providing corrosion resistance. Major alloy families include austenitic (304, 316, 321) for general-purpose use, ferritic (430, 409) for cost-effective appliance and exhaust applications, martensitic (410, 420) for high-strength cutlery and valves, duplex/super duplex for aggressive chemical and offshore environments, and precipitation-hardening grades for aerospace and marine. Products span coils, sheets, plates, pipes, tubes, bars, wire, forgings and castings, produced via integrated or increasingly scrap-based EAF routes, with varied surface finishes tailored to structural, hygienic and aesthetic applications.

Key Takeaways:

- Stainless steel remains a strategic industrial metal with stable long-term demand across infrastructure, transportation, energy and consumer sectors.

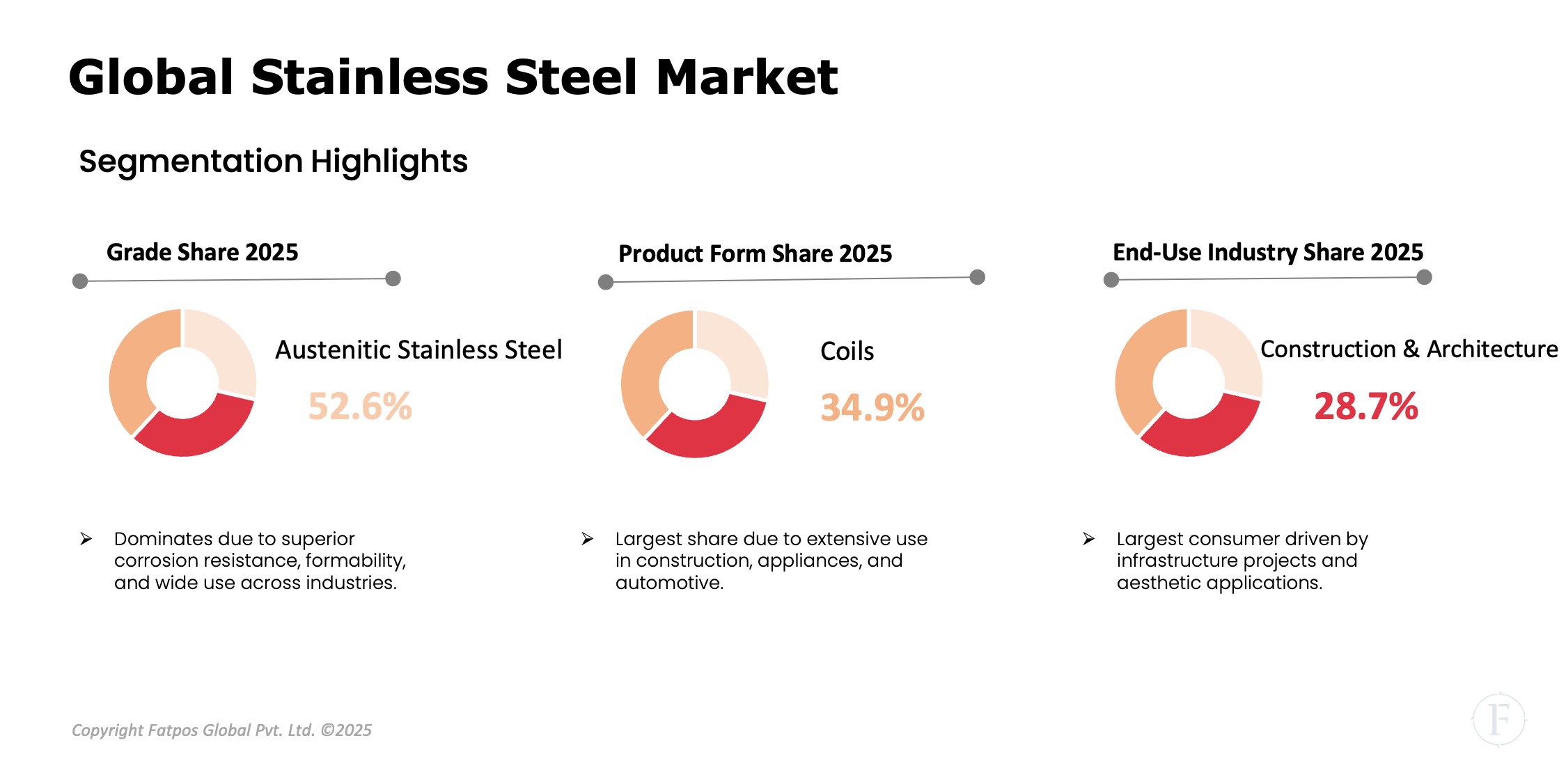

- Austenitic grades (304/316) continue to dominate volume, while duplex & higher-nickel alloys grow fastest in value terms.

- Pipes & tubes, sheets/coils are the largest product form segments by value due to heavy use in construction, energy and manufacturing.

- EAF (scrap - based) production is rising, improving carbon profile and aligning with decarbonization trends.

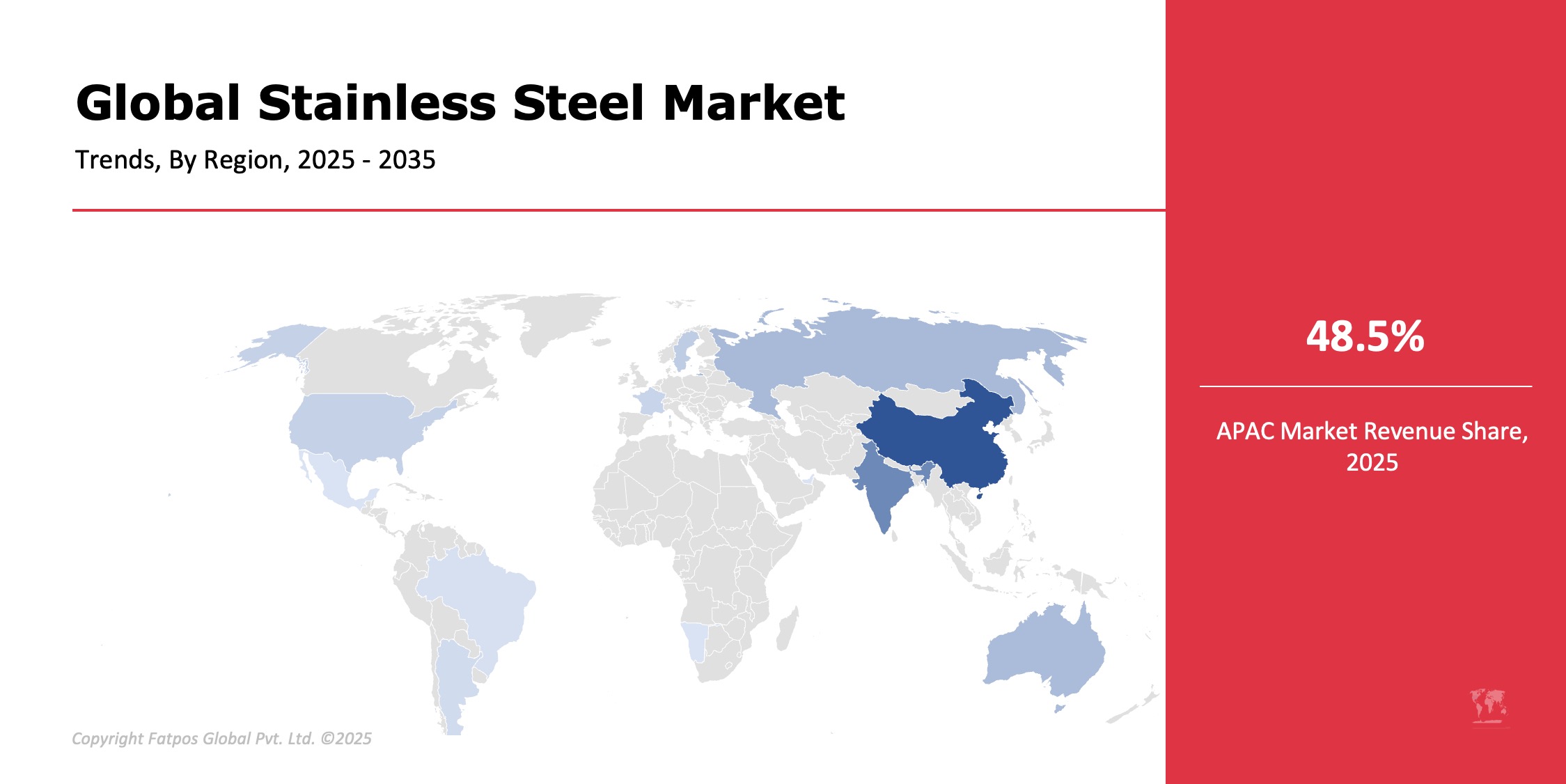

- Asia-Pacific continues to be the largest market by volume and production (China, India, South Korea, Japan), while Europe & North America lead in high-value applications and premium alloys.

- Market growth is moderate—sensitive to construction cycles, automotive production, and energy investment—but structurally supported by long-lived assets and retrofit/modernization projects.

Market Dynamics

Drivers

Stainless steel demand is underpinned by infrastructure, mobility, energy and hygiene applications. Urban construction, airports and ports consume structural and façade grades, while EVs and hybrids use stainless in exhausts, structures and battery enclosures. Duplex steels grow in pipelines, heat exchangers and offshore platforms, with 304/316 dominant in food, pharma and medical uses; rising scrap-based production supports lower-carbon, circular supply.

Restraints

Stainless steel demand is exposed to cyclicality in construction and automotive, where slowdowns quickly soften order books and pricing. Profitability is further pressured by volatile nickel, chromium and ferroalloy costs, which complicate contract pricing and inventory management. In several applications, aluminum, composites and coated carbon steels substitute on weight or cost, limiting stainless share. Trade remedies, tariffs, export controls and anti-dumping actions can disrupt traditional trade lanes, raise input costs, and drive regional market fragmentation.

Opportunities

High-value stainless and specialty alloys are increasingly specified for hydrogen, offshore wind, and desalination projects where corrosion resistance and reliability are critical. Producers can capture margin through value-added services such as pre-coating, precision forming, integrated assemblies and just-in-time delivery to OEMs. Digitalization and Industry 4.0 enhance mill productivity, quality control and traceability via digital material passports, while regionalized, scrap/EAF-based supply chains support domestic energy and infrastructure builds with lower-carbon products.

Challenges

Stainless steel producers face intensifying decarbonization pressure, as blast-furnace based integrated routes require large transition capex and are subject to rising stakeholder and regulatory scrutiny. The sector also contends with skill shortages in specialty metallurgy and precision processing, constraining high-end product development. Ambitious green steel projects and portfolio diversification into higher-alloy and value-added products are highly capital-intensive, challenging balance sheets and investment timelines.

Global Stainless Steel Market Trends

Producers are increasingly shifting to EAF and scrap-based stainless steel production to cut carbon intensity and align with green procurement requirements. Premiumization trends favor duplex, super duplex and nickel-rich alloys in highly corrosive environments, while advanced coatings and surface engineering enable anti-fingerprint, hygienic and colored finishes for architecture. Digital traceability, sustainability certifications, near-net-shape manufacturing and automated finishing improve transparency, reduce waste and shorten lead times, supporting regional reshoring of strategic stainless supply for energy and defense projects.

Key Players in the Global Stainless Steel Industry

- Outokumpu

- Acerinox

- Thyssenkrupp Stainless / Steel Europe

- Nippon Steel & Sumitomo / JFE Steel (stainless divisions)

- POSCO / POSCO International

- Tata Steel Long Products (stainless capabilities)

- Aperam

- AK Steel (now Cleveland-Cliffs in US stainless portfolio)

- Nisshin Steel / Kobe Steel (specialty stainless)

- Baosteel (stainless divisions)

- JSW / Jindal Stainless (India)

- Zhejiang Huayou

Regional & Country Analysis

Asia-Pacific has the largest stainless steel market share and manufacturing base, with China dominating output and India growing quickly on construction, rail and manufacturing demand. Europe has high per-capita use, strong uptake of premium alloys and architectural finishes, and leads in decarbonized production for chemicals and renewables such as offshore wind. North American demand is steady in energy, aerospace and machinery, supported by nearshoring and expanding EAF capacity, while EV-driven automotive changes reshape stainless applications. Latin America sees moderate demand concentrated in mining, energy and industrial projects, whereas the Middle East and Africa rely heavily on imports for high-value oil, gas, desalination and infrastructure projects, with local fabrication gradually increasing.

Segmentation Highlights

The stainless steel market is segmented along five key axes. By grade, it spans austenitic, ferritic, martensitic, duplex/super duplex, and precipitation‑hardening and other specialty alloys. By product form, it includes flat products (coils, sheets, plates), long products (bars, rods, wire), and pipes, tubes, forgings and castings. Production routes are split between integrated BF/BOF lines and increasingly important EAF or hybrid scrap-based routes. Surface finishes range from hot/cold rolled and pickled to polished, mirror and specially coated. End-use sectors cover construction, automotive, energy, chemicals, food, pharma, healthcare, appliances and industrial machinery, each modelled for value, share and annual growth for 2025–2035.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Global Stainless Steel Market Forecast Period |

2025–2035 |

|

Global Stainless Steel Market Size by 2035 |

USD 276.6billion |

|

Market CAGR |

4.5% |

|

By Grade |

Austenitic: 304, 316; Ferritic: 430; Martensitic; Duplex; Precipitation-Hardening |

|

By Product Form |

Coils, Sheets & Plates, Bars & Rods, Pipes & Tubes, Wire, Forgings |

|

By Production Route |

Integrated Mills, Electric Arc Furnace), By Surface Finish (Cold-Rolled, Hot-Rolled, Polished |

|

By End User |

Construction & Architecture, Automotive & Transportation, Industrial Machinery, Energy & Power, Food & Beverage, Medical & Healthcare, Chemical & Petrochemical, Consumer Appliances |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Key Market Players |

Outokumpu, Acerinox, Thyssenkrupp Stainless / Steel Europe, Nippon Steel & Sumitomo / JFE Steel (stainless divisions), POSCO / POSCO International, Tata Steel Long Products (with stainless capabilities), and Aperam |

Global Stainless Steel Industry Instances

- A major refinery project selected super duplex piping across subsea manifolds for corrosion resistance in sour environments.

- A stadium façade project specified mill-finished 316L panels for longevity in marine climate.

- An EV OEM adopted stainless battery enclosures for improved thermal and fire safety.

- An EAF-based mill launched a low-carbon stainless slab product with documented LCA to win green procurement tenders.

Analyst Review

As per our Global Stainless Steel Market Analysis report, Stainless steel’s long service life, recyclability, and performance across diverse environments underpin its strategic role in future industrialization. While volume growth may track global industrial cycles, the value uplift from higher-grade alloys, value-added processing and green production credentials presents significant upside. Manufacturers that invest in scrap-circularity, EAF modernization, product diversification (duplex, specialty alloys), and digital quality traceability are best positioned to capture premium margins and meet decarbonizing-buyer demands. Trade policy, raw material supply (nickel & chromium), and regional infrastructure programs will remain the primary short-term risk factors.

Frequently Asked Questions (FAQ):

Austenitic (304/316) grades remain the largest volume contributors globally.

Duplex and super-duplex steels are growing fastest in value due to demand from offshore, chemical and desalination projects.

EAF/scrap-based production and supplier LCA credentials are increasingly required by customers; integrated mills face transition investment needs

Asia-Pacific (China & India) dominates volume; Europe and North America are critical demand markets for premium alloys.

Mill owners, downstream processors, pipe & tube manufacturers, OEM procurement teams, commodity traders, investors, and policy makers.

Select License Type

Select License Type