SiC Ceramics Market Research 2035

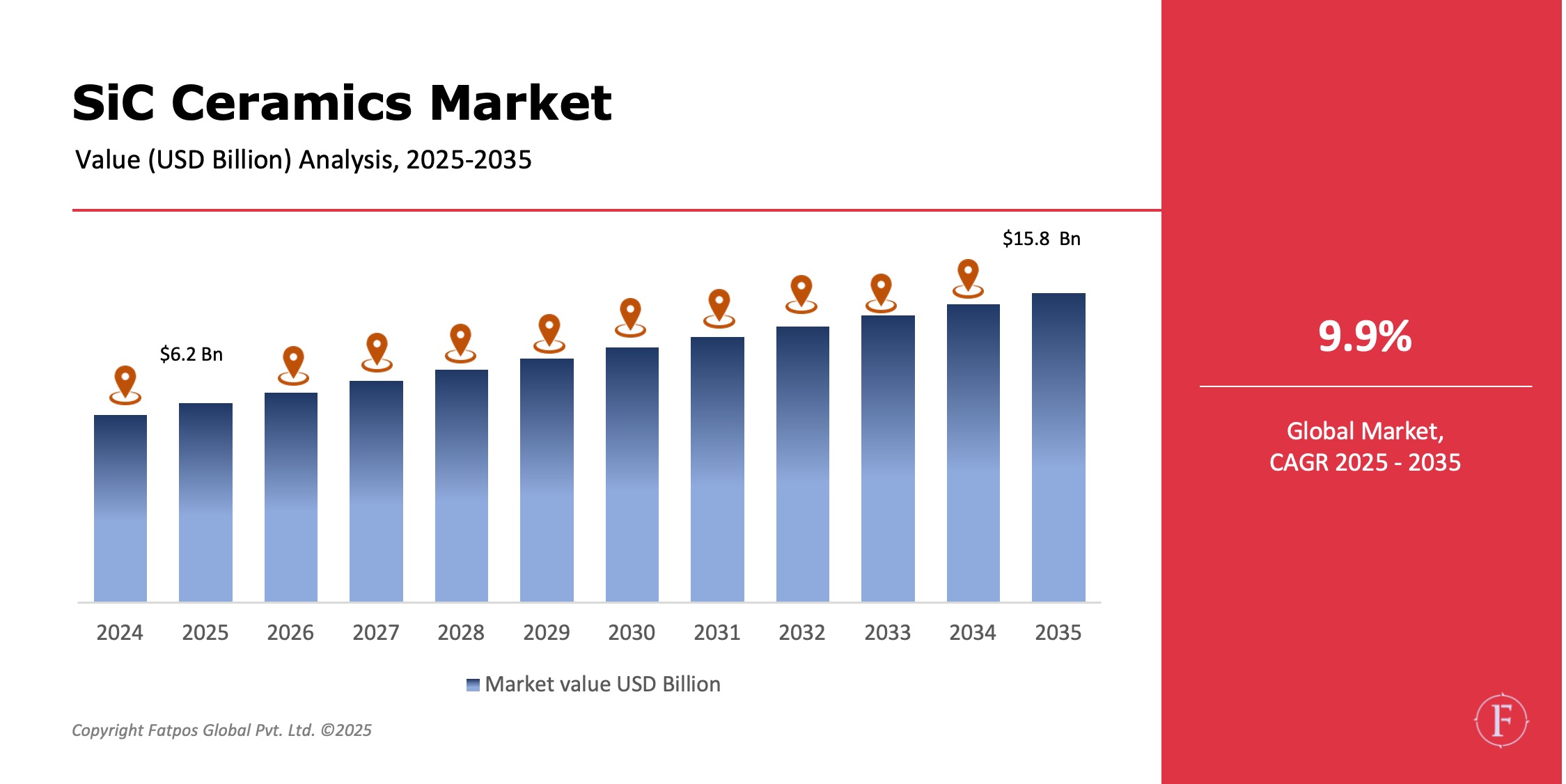

The SiC Ceramics Market Size was valued at USD 6.2 billion in 2025 and is projected to reach USD 15.8 billion by 2035, registering a CAGR of 9.9%. Market growth is driven by the rising demand for high-performance ceramic materials, expansion of semiconductor and power electronics manufacturing, increasing adoption in electric vehicles, and growing requirements for materials capable of withstanding extreme temperatures, mechanical stress, and corrosive environments.

Product Overview

SiC ceramics are advanced non-oxide ceramic materials produced using silicon carbide powder processed through sintering, bonding, or recrystallization techniques. These materials exhibit exceptional thermal stability at temperatures exceeding 1,600°C, high mechanical strength, superior abrasion resistance, and outstanding chemical and corrosion resistance. Additionally, SiC ceramics offer high thermal conductivity and favorable electrical properties, enabling use in both structural and functional applications.

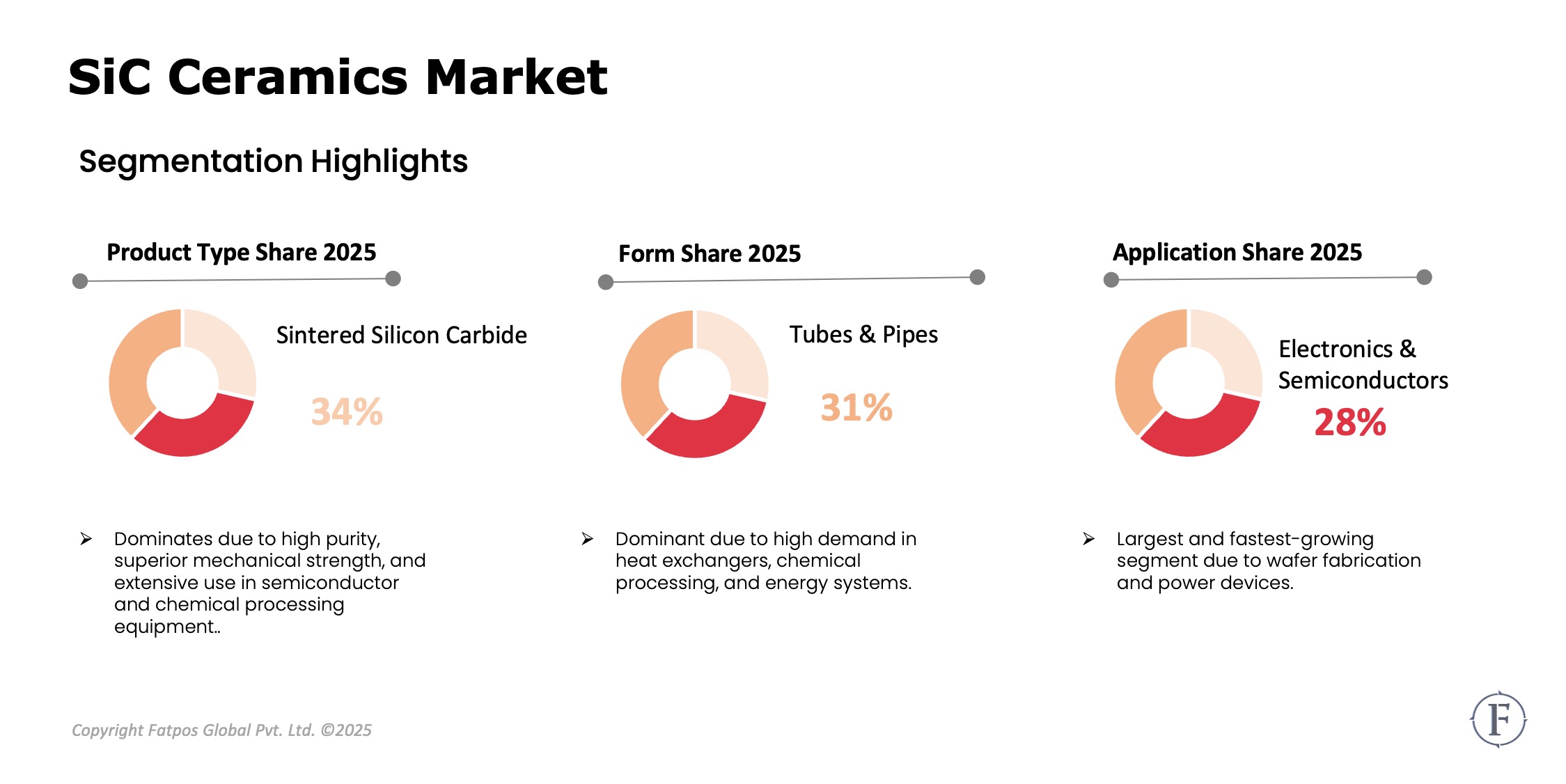

By product type, reaction-bonded silicon carbide (RBSC) is widely used due to its near-net-shape capability and cost efficiency. Sintered silicon carbide (SSiC) provides the highest purity and mechanical performance, making it suitable for semiconductor and chemical processing applications. Nitride-bonded silicon carbide (NBSC) is valued for thermal shock resistance, while recrystallized silicon carbide (RSiC) is used in high-temperature kiln furniture and energy applications. By form, SiC ceramics are manufactured as tubes, pipes, plates, discs, beams, rods, and complex-shaped components, supporting both standardized and customized industrial requirements.

Key Takeaways :

- The SiC ceramics market is expected to grow at ~9.9% CAGR through 2035

- Sintered and reaction-bonded SiC dominate product adoption

- Semiconductors and power electronics are the fastest-growing applications

- Automotive electrification significantly boosts demand

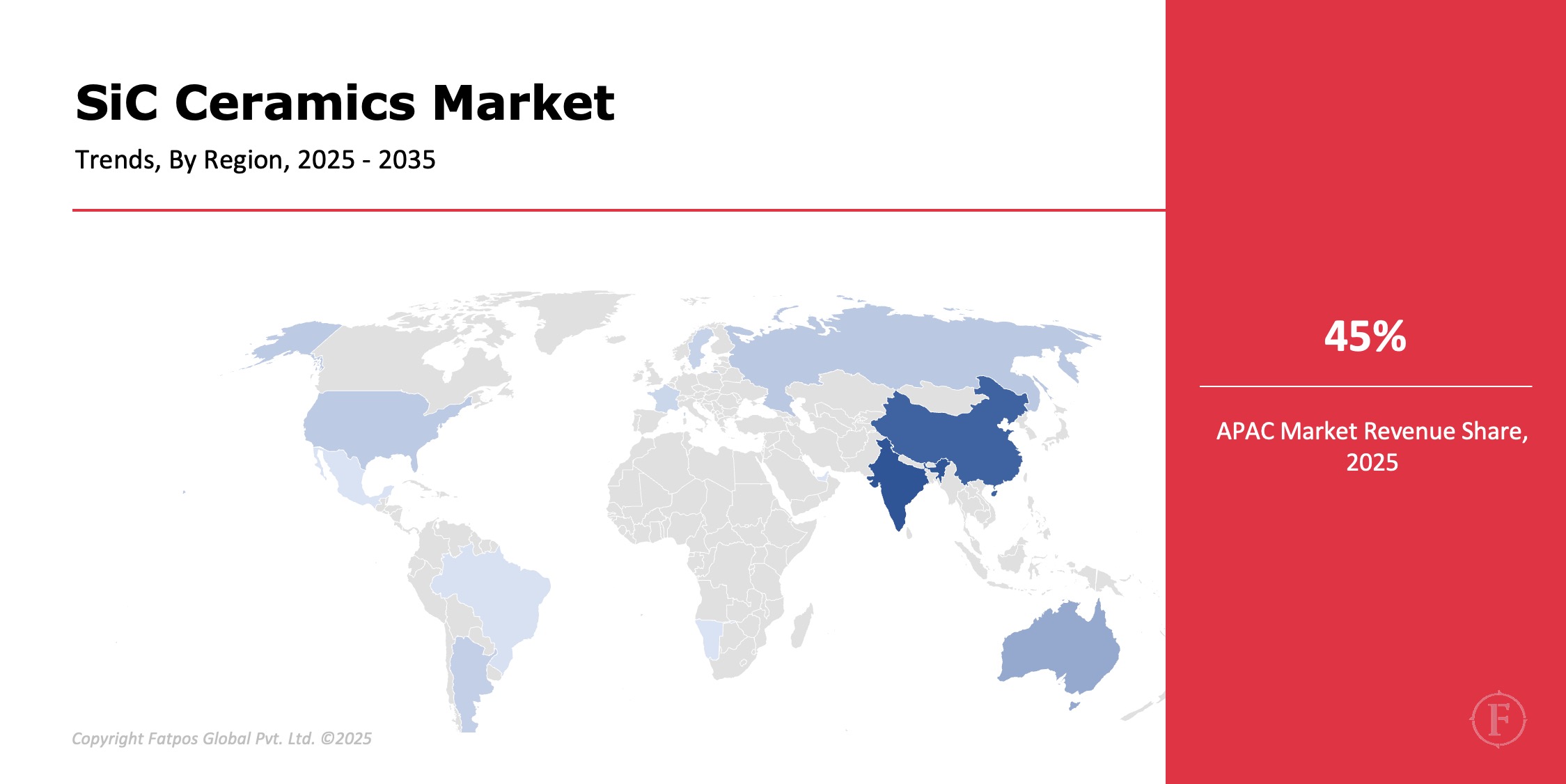

- Asia-Pacific leads global production and consumption

- Material performance and process innovation drive competitiveness

Market Dynamics

Drivers

The primary driver of the SiC ceramics market is the rapid expansion of semiconductor manufacturing and power electronics, particularly for electric vehicles, renewable energy systems, and high-voltage applications. SiC ceramics are essential in wafer processing equipment, plasma chambers, and thermal management systems due to their purity, thermal conductivity, and chemical resistance.

Growing adoption of electric vehicles and fast-charging infrastructure further accelerates demand for SiC-based components capable of handling high power densities and thermal loads. Industrial applications such as chemical processing, metal production, and energy generation require materials that maintain performance under extreme operating conditions, favoring SiC ceramics over traditional materials.

Restrictions

Despite robust demand, the SiC (silicon carbide) ceramics market grapples with key hurdles. High manufacturing costs stem from capital-intensive sintering—requiring high-temperature furnaces—and precision machining for tight tolerances, inflating prices 2-5x over alternatives. Complex processing demands specialized expertise, scarce globally, leading to production bottlenecks and quality variability. Long qualification cycles in semiconductors (for wafers/power devices) and aerospace (engine components) delay market entry by 2-3 years due to rigorous testing. Raw material volatility—silicon and carbon supply disruptions—and energy-heavy processes (up to 10x cement's intensity) exacerbate cost pressures amid fluctuating energy prices. These factors compress margins, limiting scalability despite SiC's superior thermal/electrical properties.

Opportunities

The SiC Ceramics market holds strong opportunities in sustainable, smart technologies. Smart and energy-efficient devices align with global sustainability goals, featuring low-power designs, recyclable materials, and IoT optimization amid stricter regulations and eco-conscious consumers. Wearable health devices—like fitness trackers and biometric smart watches—thrive on post-pandemic health focus, alongside smart home appliances for automation and security, supported by subscriptions.

AI integration in gadgets enhances personalization and voice features, driving differentiation. Emerging markets in Asia-Pacific, Africa, and Latin America explode with digital penetration, improved infrastructure, rising incomes, and tech awareness, unlocking massive potential. Success requires R&D, partnerships, and localization.

Challenges

Scaling high-purity SiC for semiconductors demands flawless consistency, but defects in crystal growth or polishing slash yields to under 80%. Machining proves tricky—SiC's extreme hardness requires diamond tools, while brittleness risks cracks during shaping. Yield optimization struggles with process variability in CVD/PVD deposition. IP walls from leaders like Wolfspeed block newcomers, compounded by lengthy customer qualifications (1-2 years) and high switching costs for validated suppliers. Striking a balance—pushing performance (eg, lower resistance) without cost spikes—remains elusive amid R&D expenses.

SiC Ceramics Market Trends

Demand spikes for high-purity SiC in semiconductor manufacturing equipment—wafer boats, susceptors, and plasma etch parts—critical for sub-2nm processes due to unmatched purity and heat resistance. Custom-engineered components proliferate in EVs (inverters handling 800V+), renewables (wind turbine generators), and aerospace (turbine shrouds), designed via CAD for precise tolerances. Digital manufacturing transforms production: process automation with robotics ensures repeatability; AI-driven machine learning predicts defects, boosting yields to 95%; digital twins simulate sintering for optimization. Sustainability pushes include electric furnaces slashing emissions, water recycling, and circular supply chains reusing grind waste. Strategic alliances—eg, STMicroelectronics with substrate makers or Toyota with ceramists—lock in supply, co-develop specs, and fund next-gen like sintered SiC for 1,200V devices This convergence accelerates commercialization and cost parity with silicon as per market forecast.

Key Players in the SiC Ceramics Industry

- CoorsTek, Inc.

- Saint-Gobain

- Morgan Advanced Materials

- CeramTec GmbH

- Kyocera Corporation

- NGK Insulators, Ltd.

- SGL Carbon SE

- Entegris, Inc.

- 3M Company

- Ibiden Co., Ltd.

Regional & Country Analysis

Asia-Pacific dominates the SiC ceramics market due to strong semiconductor manufacturing ecosystems, automotive electrification, and industrial expansion in China, Japan, South Korea, and Taiwan. North America shows robust growth driven by semiconductor fabs, defense applications, and clean energy investments. Europe maintains steady demand from automotive, aerospace, and industrial machinery sectors. Latin America and Middle East & Africa present emerging opportunities through energy and industrial infrastructure development.

Segmentation Highlights

By product type, sintered and reaction-bonded SiC hold the largest shares. By application, semiconductors and power electronics represent the fastest-growing segments. Automotive and energy applications show strong momentum, while industrial machinery and chemical processing provide stable baseline demand.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 15.8 Billion |

|

Market CAGR |

9.9% |

|

By Product Type |

Reaction-Bonded SiC, Sintered SiC, Nitride-Bonded SiC, Recrystallized SiC |

|

By Form |

Tubes & Pipes, Plates & Discs, Beans & Rods, Complex-Shaped Components |

|

By Application |

Semiconductors, Power Electronics, Automotive, Aerospace & Defense, Energy, Industrial Machinery, Chemical Processing |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

SiC Ceramics Market: Key Players |

CoorsTek, Inc., Saint-Gobain, Morgan Advanced Materials, CeramTec GmbH, Kyocera Corporation |

Global SiC Ceramics Industry Instances

- Semiconductor fabs in global SiC ceramics industry adopted high-purity SiC chamber components

- EV manufacturers integrated SiC-based power modules

- Chemical plants deployed SiC heat exchangers for corrosion resistance

- Energy firms used SiC ceramics in high-temperature systems

Analyst Review

As per our SiC ceramics market analysis report the market is transitioning from niche industrial usage to strategic importance across semiconductors, electrification, and advanced manufacturing. While cost and processing complexity remain challenges, technological advancements and expanding end-use applications are expected to drive market share growth through 2035.

Frequently Asked Questions (FAQ):

SiC ceramics from silicon/carbon offer top thermal conductivity (490 W/mK), hardness, oxidation resistance. Made via sintering/CVD, they excel in semiconductors, EVs, aerospace over metals.

EV/renewable electrification, 5G/6G semis, power electronics, and industrial apps drive SiC demand; green policies and miniaturization boost CAGR >10%.

Sintered (hot-pressed for purity) and reaction-bonded SiC lead, holding 60%+ share. Sintered suits electronics/semiconductors for density; reaction-bonded fits large armor/abrasives with cost-effectiveness and near-net shapes.

Asia-Pacific commands 50%+ market, driven by China's semiconductor push, Japan's auto giants (Toyota), South Korea's electronics (Samsung), and Taiwan's fabs. Abundant supply chains and R&D investments outpace North America/Europe

Robust growth (CAGR 12-15% to 2030) from EV boom (800V systems), 6G/AI chips, hydrogen tech, and AM. Cost reductions via scaled CVD, recycling, and China capacity will broaden adoption beyond premiums.

Select License Type

Select License Type