Geopolymes Market Research 2035

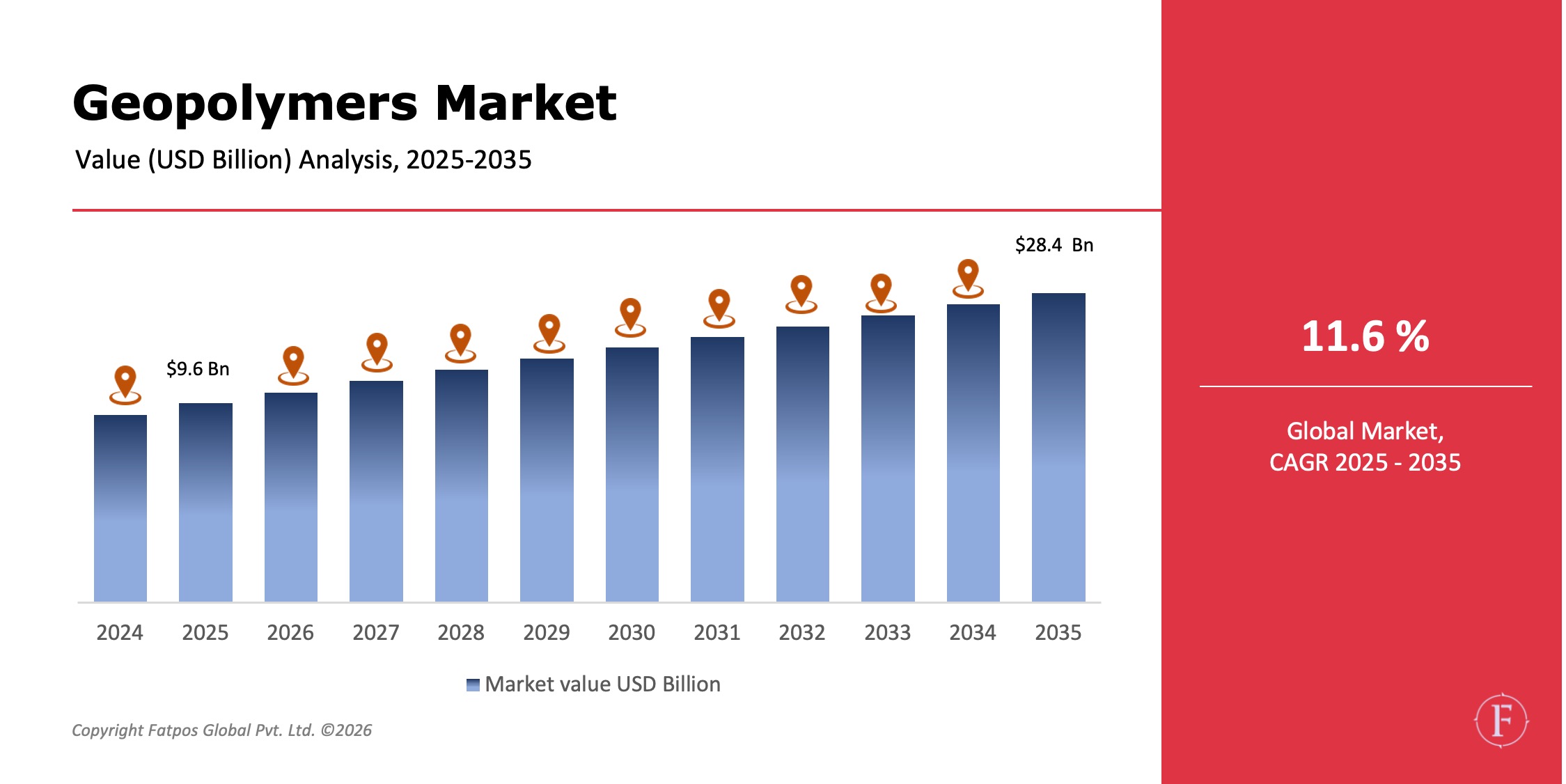

The Geopolymers Market Size was valued at USD 9.6 billion in 2025 and is projected to reach USD 28.4 billion by 2035, registering a CAGR of 11.6%. Market growth is driven by rising demand for low-carbon construction materials, increasing regulatory pressure to reduce CO₂ emissions from cement production, growing utilization of industrial by-products, and expanding infrastructure development across emerging economies. Geopolymers are inorganic, aluminosilicate-based materials synthesized from industrial waste streams such as fly ash, blast furnace slag, and metakaolin. They offer superior mechanical strength, chemical resistance, thermal stability, and significantly lower carbon footprints compared to conventional Portland cement. As global construction and infrastructure sectors transition toward sustainability and circular economy principles, geopolymers are increasingly being adopted across structural, industrial, and specialty applications.

Product Overview

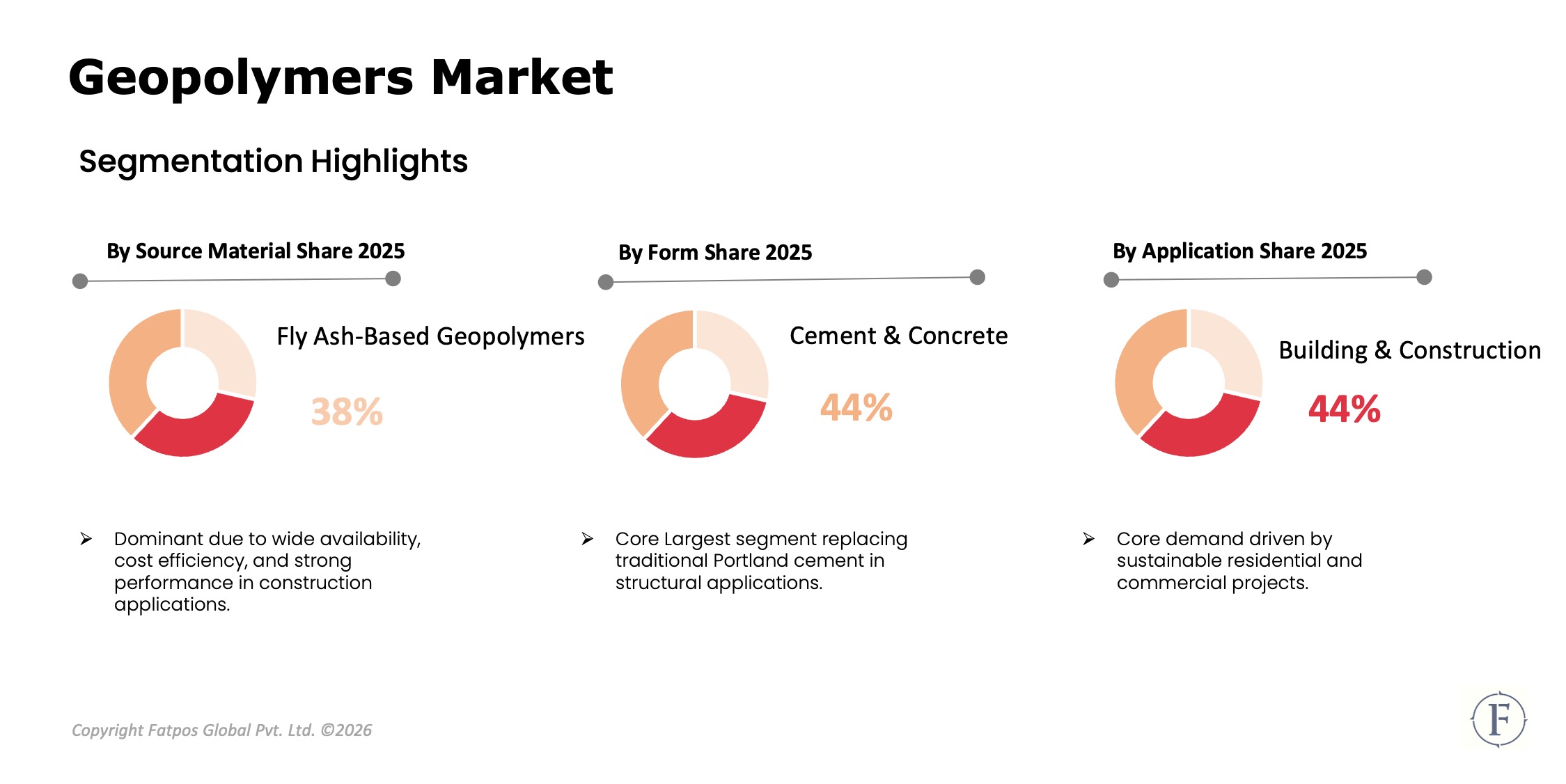

Geopolymers are engineered materials produced through alkali activation of aluminosilicate sources, forming a three-dimensional polymeric network. By source material, fly ash-based geopolymers are widely used due to abundant availability and cost efficiency, particularly in regions with coal-based power generation. Slag-based geopolymers offer high early strength and durability, making them suitable for infrastructure and precast applications. Metakaolin-based geopolymers are preferred for high-performance and specialty uses due to controlled composition and superior consistency.

By form, geopolymers are used as cement and concrete alternatives, mortars and grouts, precast elements, and composite panels. Their inherent fire resistance, chemical stability, and low shrinkage make them suitable for demanding environments.

Key Takeaways :

- The geopolymers market is expected to grow at ~11.6% CAGR through 2035.

- Fly ash- and slag-based geopolymers dominate material adoption.

- Building, construction, and infrastructure remain the largest application segments.

- Sustainability regulations strongly influence market growth.

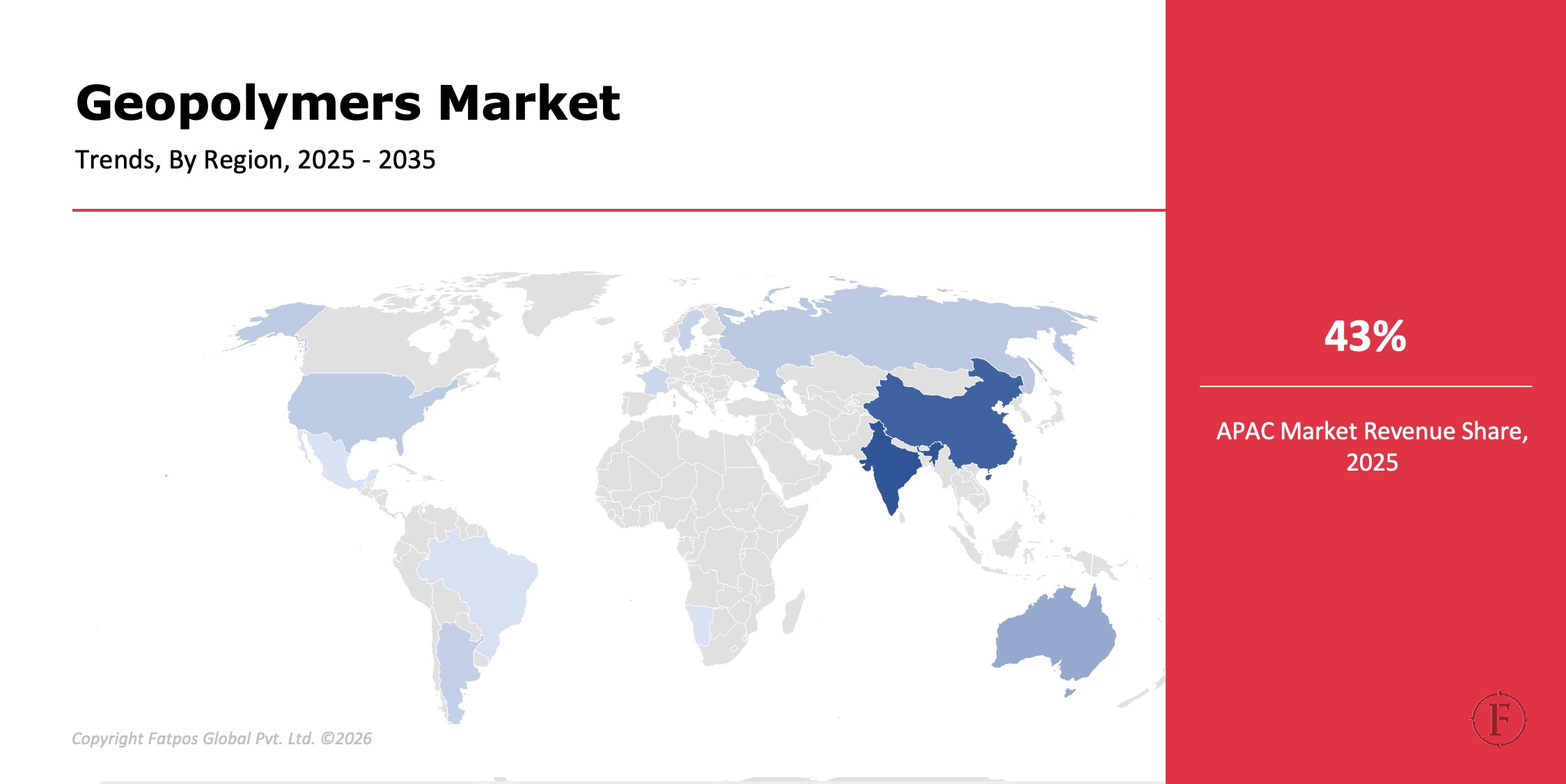

- Asia-Pacific leads global consumption and production.

- Low-carbon performance is the primary competitive differentiator.

Market Dynamics

Drivers

The primary driver of the geopolymers market is the global push to reduce carbon emissions associated with conventional cement and concrete production. Cement manufacturing accounts for a significant share of industrial CO₂ emissions, prompting governments and industry stakeholders to adopt alternative materials. Geopolymers offer up to 70–90% lower carbon emissions, making them attractive for sustainable construction initiatives.

Increasing infrastructure development, particularly in emerging economies, is driving demand for durable and cost-effective construction materials. Utilization of industrial by-products such as fly ash and slag aligns with circular economy goals while reducing landfill waste. Additionally, superior performance characteristics, including fire resistance and chemical durability, support adoption in industrial and infrastructure projects.

Restraints

Despite strong growth potential, the geopolymers market faces restraints related to limited standardization and lack of widespread regulatory acceptance. Absence of unified construction codes and standards restricts large-scale adoption in some regions. Variability in raw material quality, particularly fly ash, can affect product consistency and performance.

Higher initial development and processing costs, limited contractor familiarity, and conservative construction practices further restrain adoption. Supply chain dependence on industrial waste availability also introduces regional variability in production capacity.

Opportunities

Significant opportunities exist in green building construction, transport infrastructure, and industrial flooring, where durability and sustainability are critical. Growth in prefabricated and modular construction supports adoption of geopolymer-based precast products. Expansion of waste encapsulation and stabilization applications presents additional revenue streams, particularly for hazardous and radioactive waste management. Research advancements in hybrid geopolymer formulations, fiber reinforcement, and additive manufacturing enable new applications and performance enhancements. Government incentives for low-carbon materials and public infrastructure projects further expand market opportunities.

Challenges

Geopolymer manufacturers face challenges in scaling production while maintaining quality consistency. Limited awareness among contractors, engineers, and policymakers slows adoption. Technical challenges related to curing conditions, alkali activator handling, and long-term performance validation require continuous R&D investment.

Logistical challenges arise from sourcing and transporting industrial by-products, while fluctuating availability of fly ash due to energy transition trends impacts raw material supply. Achieving cost competitiveness with traditional cement remains a key challenge in price-sensitive market and influences in long run market forecast.

Geopolymers Market Trends

The geopolymers market prioritizes low-carbon alternatives to cement, valorizing industrial wastes like fly ash and slag to cut emissions and landfills. Adoption surges in infrastructure—roads, bridges—and precast elements, thanks to geopolymers' quick curing (hours vs. days), superior durability against acids/heat, and cost savings over time. Research spotlights hybrid binders merging geopolymers with Portland cement for versatility; fiber-reinforced variants boost tensile strength for seismic zones; ambient-cured formulas eliminate energy-intensive heat, aiding on-site use. Green certifications (LEED, BREEAM) and ESG reporting fast-track acceptance in eco-projects. Industry collaborations—e.g., universities with firms like CEMEX—drive pilots to commercialization.

Digital tools, including BIM software and AI-driven modeling, simulate and refine mixes for apps like 3D-printed structures or repairs.

Key Players in the Geopolymers Industry

- Wagners Holding Company

- Zeobond Pty Ltd.

- Banah UK Ltd.

- Geopolymer Solutions LLC

- Schlumberger Limited

- CEMEX S.A.B. de C.V.

- BASF SE

- Sika AG

- Saint-Gobain

- Holcim Group

Regional & Country Analysis

Asia-Pacific dominates the geopolymers market due to extensive infrastructure development, availability of industrial by-products, and strong government focus on sustainable construction in countries such as China, India, and Australia accounting for a significant market share. Europe shows steady adoption driven by strict environmental regulations and green building initiatives. North America experiences growing interest in infrastructure rehabilitation and low-carbon materials. Latin America records moderate growth supported by urbanization, while Middle East & Africa present emerging opportunities through large-scale infrastructure and industrial projects.

Segmentation Highlights

By source material, fly ash-based geopolymers hold the largest share due to cost efficiency and availability. By form, cement and concrete applications dominate demand, followed by precast products. Building and infrastructure applications account for the majority of consumption, while industrial and specialty applications demonstrate faster growth rates.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025–2035 |

|

Market Size by 2035 |

USD 28.4 Billion |

|

Market CAGR |

11.6% |

| By Source Material | Fly Ash, Slag, Metakaolin, Others. |

|

By Form |

Cement & Concrete, Motars & Grouts, Precast Products, Composites |

|

By Application |

Building & Construction, Infrastructure, Industrial, Fire-Resistance, Materials, Waste Encapsulation, others. |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Geopolymers Market: Key Players |

Wagners, Zeobond, Banah UK, Geopolymer Solutions |

Global Geopolymers Industry Instances

- Infrastructure projects within the global geopolymer industry adopted geopolymer concrete for reduced carbon footprints.

- Industrial facilities used geopolymers for fire-resistant flooring systems.

- Governments promoted geopolymer use in public construction projects.

- Waste management firms used geopolymers for hazardous waste encapsulation.

Analyst Review

As per our Geopolymers Market analysis, the market is transitioning from niche adoption to broader commercial deployment as sustainability mandates intensify. While regulatory gaps, awareness challenges, and supply variability persist, advancements in material science and increasing acceptance of low-carbon alternatives are driving strong long-term growth. Companies investing in scalable production, standardization, and strategic partnerships are expected to lead the market growth through 2035.

Frequently Asked Questions (FAQ):

Geopolymers are eco-friendly inorganic polymers from aluminosilicates in by-products like fly ash or slag, activated by alkalis to form low-CO₂ binders (70-90% less than Portland cement).

Sustainability rules like EU Green Deal and net-zero goals drive low-carbon geopolymers; Asia/Africa infrastructure booms need durable options.

Building & infrastructure dominate geopolymers market (60%+ share), shining in precast panels, roads, bridges with fast setting, corrosion resistance, and green credentials for megaprojects.

Asia-Pacific leads geopolymers (40%+ share) via China's infrastructure, India's housing, fly ash abundance, policies, and urbanization.

Standardization lacks global codes, hindering adoption. Raw material variability (e.g., fly ash quality) affects consistency. Limited awareness among contractors, plus higher initial costs and skill gaps for mixing/handling, slow scaling despite pilots.

Select License Type

Select License Type