Polysilicon Market Research, 2034

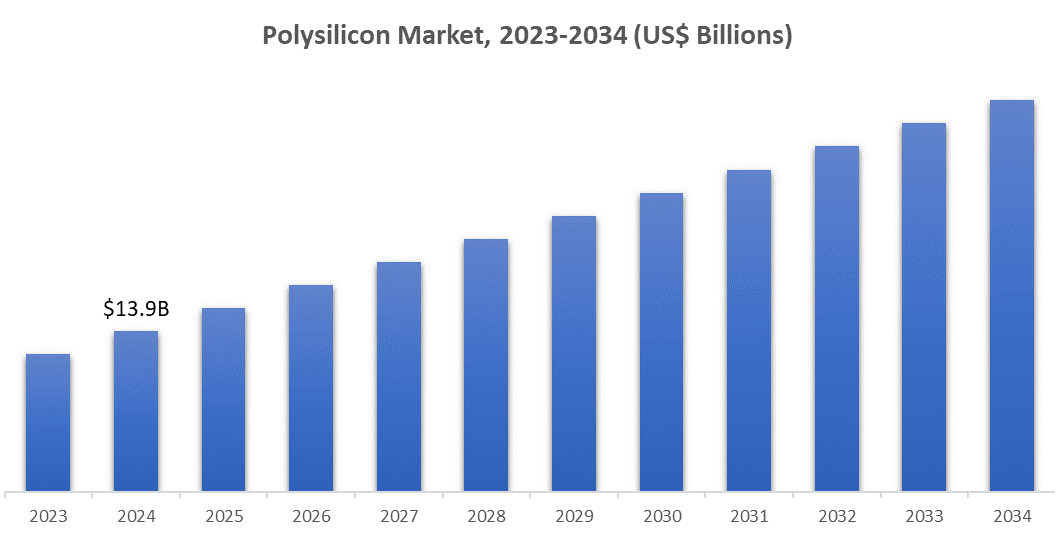

The global polysilicon market is expected to grow at a 13.1% CAGR during the forecast period (2024-2034). The market size was valued at US$ 12.3 billion in 2023 and is projected to reach US$ 47.6 billion by 2034.

Polysilicon, also known as polycrystalline silicon, is a pure type of silicon that finds its main applications in the solar and semiconductor sectors. The purification of metallurgical-grade silicon is typically done using the Siemens process, where silicon is deposited from a gas phase onto rods. Polysilicon is an essential raw material for producing solar panels' photovoltaic (PV) cells that transform sunlight into electricity.

In the semiconductor sector, it is crucial to create integrated circuits and microchips for their outstanding electrical characteristics. Polysilicon is highly sought after for its exceptional purity, necessary for efficient solar energy generation and the creation of advanced electronic devices. The manufacturing process consumes a lot of energy and necessitates sophisticated technology.

Market Highlights

The market is growing due to the rapid expansion of the solar energy industry, as global demand for renewable energy surges. Government initiatives and regulations encouraging the use of clean energy also contribute to the increasing demand for polysilicon in photovoltaic (PV) applications.

Furthermore, the growth of electronics, electric vehicles, and smart devices is driving advancement in semiconductor technology, leading to a higher demand for polysilicon. With the shift towards sustainable energy and advanced electronics, the market is projected to rise due to lower production costs, technological advancements, and the demand for sustainable energy and high-quality semiconductors.

Market Segmentation:

Solar PV dominates the market driven by rapid growth in the solar energy sector and supportive government subsidies

The market is classified based on Application into Solar PV, and Electronics (Semiconductor). Several key factors drive the global dominance of solar photovoltaic (PV) in the polysilicon industry. The rapid expansion of solar power, driven by a global shift towards sustainable energy and developments in solar cell effectiveness, has significantly enhanced the demand for solar panels that depend on polysilicon.

Furthermore, government support and subsidies, such as feed-in tariffs and tax benefits, have also accelerated the adoption of solar energy, leading to a greater demand for polysilicon. Additionally, significant reductions in the costs associated with solar panels in the last ten years have made solar power more cost-effective, broadening its availability and boosting demand even more. Combining these factors has strengthened the solar PV industry's control over the use of polysilicon.

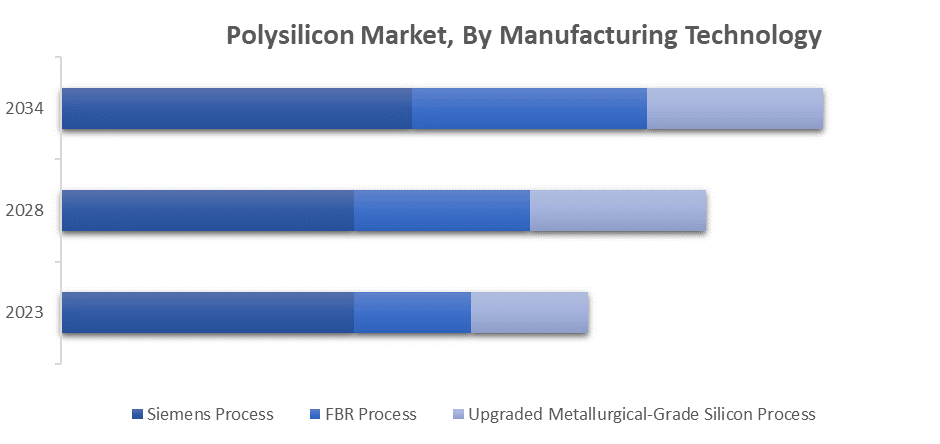

Siemens' manufacturing processes, offering higher purity and better scalability, strengthen its position as the market leader

Market is classified based on the Manufacturing Technology into Siemens Process, FBR Process, and Upgraded Metallurgical-Grade Silicon Process. The Siemens method is the most widely used technology globally for producing high-purity polysilicon, crucial for solar and semiconductor purposes. Even with newer available options, the Siemens method continues to be favoured for its ability to grow, experience, and dependability.

Factors such as a well-established supply chain for raw materials and equipment and economies of scale contribute to its dominance, allowing for efficient operations and cost savings in large facilities. Years of development have fine-tuned the process variables, guaranteeing reliable, top-notch results. The industry's deep familiarity with the Siemens process boosts its dependability, reducing operational risks and strengthening its status as the industry standard.

Market Dynamics:

Growth Drivers

Fast-Growing Solar Industry to Facilitate Market Expansion and Provide Growth Opportunities

The ever-rising demand for polysilicon is largely being fueled by the global transition to renewable energy sources, with a strong focus on solar power. As countries strive to lower carbon emissions and achieve climate targets, solar energy has become a critical answer due to sustainability and falling prices. Polysilicon is an essential substance in photovoltaic cells, which serve as the foundation of solar panels.

Continual advancements in solar technology have resulted in more effective and affordable solar panels, increasing their use. Governments around the world are putting in place strategies, financial support, and rewards to encourage the adoption of solar power, establishing a strong market for PV systems. The increase in the use of solar energy is closely connected to the growing need for polysilicon, which has become essential in the alternative energy industry.

Technological Advancement in the Semiconductor Industry to Boost Market Growth

The semiconductor industry is growing rapidly due to the rising need for high-tech gadgets, consumer products, and new technologies such as 5G, AI, and electric cars. High-quality polysilicon is vital in producing semiconductor wafers, which serve as the base for integrated circuits and microchips found in electronic devices. With advancements in technology, there is an increasing requirement for smaller, faster, and more efficient semiconductors, which is amplifying the need for top-quality polysilicon.

Moreover, the growth of the semiconductor market is being influenced by the increasing popularity of smart devices and the expansion of the Internet of Things (IoT). The increasing use of semiconductors has boosted the need for polysilicon, solidifying its importance in the electronics field.

Restraints

Fluctuating Raw Materials Costs to Restrict Market Growth Prospects

Fluctuating prices of raw materials, especially silicon, have a major influence on the costs of production and profitability of companies that produce polysilicon. Silicon, the main material used in making polysilicon, can fluctuate in the market due to disruptions in the supply chain, shifts in demand, and geopolitical tensions. Rising silicon prices lead to higher production costs, which in turn, reduce profit margins for polysilicon producers.

The uncertainty may cause difficulties for manufacturers to keep their operations stable due to uncertain pricing and contracts. Moreover, the expense of other necessary components such as energy, workforce, and logistics may vary, making cost control more challenging. Therefore, polysilicon producers need to carefully manage these pricing uncertainties to stay competitive and profitable in a market that is very responsive to raw material expenses.

Recent Developments

- In 2023, Wacker Chemie AG introduced a new high-purity polysilicon grade tailored for advanced semiconductor applications, focusing on ultra-pure silicon wafers required for next-generation electronics. In 2024, the company entered into a joint venture with a leading Asian solar company to expand its polysilicon production capacity, aiming to meet the rising demand from the global solar energy sector.

- In 2023, Tokuyama Corporation announced the expansion of its production facilities in Japan, aiming to increase output for high-purity polysilicon used in semiconductors. The company also launched a new line of ultra-high-purity polysilicon products specifically designed for emerging applications in 5G technology and electric vehicles.

- In 2023, CL-Poly Energy Holdings Limited completed a merger with a leading Chinese solar company, enhancing its market position and production capabilities in the polysilicon sector. In 2024, the company introduced a new low-cost, high-efficiency polysilicon product targeting the growing demand in the photovoltaic industry.

- In 2023, OCI Company Ltd. acquired a smaller polysilicon producer in Southeast Asia, boosting its production capacity and expanding its market reach in the region.

- In 2023, REC Silicon ASA introduced a new polysilicon grade optimized for use in high-efficiency solar panels, aimed at reducing the overall cost of solar energy generation. The company also entered into a joint venture with a major U.S. semiconductor company to develop advanced polysilicon materials for next-generation electronics.

Key Players:

- Wacker Chemie AG

- Tokuyama Corporation

- GCL-Poly Energy Holdings Limited

- OCI Corporation

- REC Silicon ASA

- Daqo New Energy Corp.

- Hemlock Semiconductor Corporation

- Jinko Solar

- Mitsubishi Materials Corporation

- LDK Solar Co., Ltd.

- Silicor Materials Inc.

- SunEdison, Inc.

- Sichuan Yongxiang Co., Ltd.

- KCC Corporation

- Tianwei New Energy Holdings Co., Ltd.

- Other Prominent Players (Company Overview, Business Strategy, Key Product Offerings, Financial Performance, Key Performance Indicators, Risk Analysis, Recent Development, Regional Presence, SWOT Analysis)

Regional Analysis

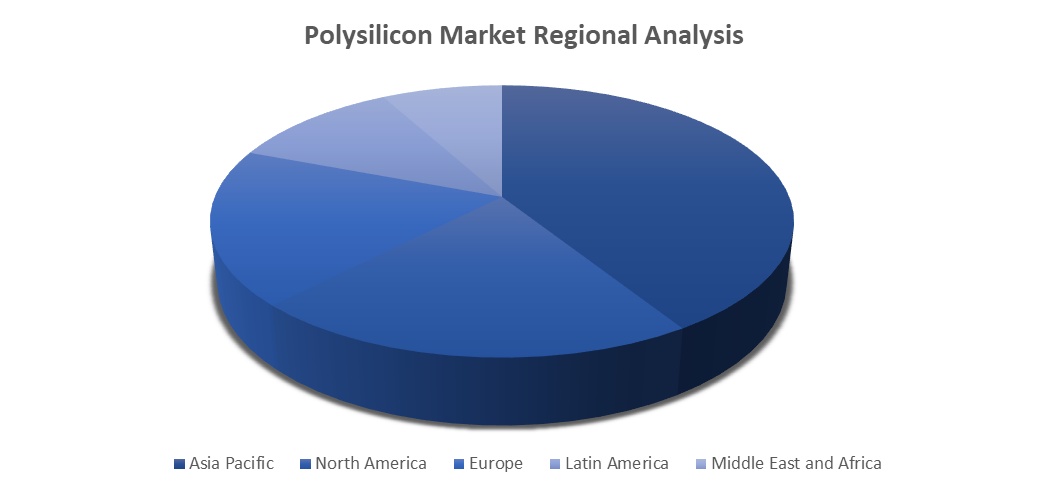

The Global polysilicon market is segmented based on regional analysis into five major regions: North America, Latin America, Europe, Asia Pacific and the Middle East and Africa.

The Asia Pacific region leads the global market, mainly due to its role as a manufacturing center for solar photovoltaic (PV) and semiconductor sectors. China, South Korea, and Japan are significant contributors, with China being the top producer of polysilicon attributed to its large solar panel manufacturing sector. Positive government actions, such as providing financial support for renewable energy and advancements in technology, continue to strengthen the market control of the region.

Asia Pacific's dominance in the market is due to the abundant raw materials, cost-efficient production, and a solid supply chain. Moreover, the semiconductor sector's growth is being driven by the rapid industrialization of the region and the rising demand for electronics, which is strengthening its position as the top global leader. Although Asia Pacific is the dominant force in the market, other regions also have had important contributions.

The advanced semiconductor industry and increasing use of solar energy make North America, especially the United States, an important market. Europe is a significant region where countries such as Germany are at the forefront of solar technology and renewable energy efforts.

Latin America is emerging solely due to the rise of solar energy projects, especially in nations such as Brazil and Chile.

The renewable energy sectors in the Middle East and Africa are increasing slowly, with a particular emphasis on solar power in the Middle East and a rising fascination with semiconductors in Africa.

Market is further segmented by region into:

- North America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United States and Canada

- Latin America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – Mexico, Argentina, Brazil, and Rest of Latin America

- Europe Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United Kingdom, France, Germany, Italy, Spain, Belgium, Hungary, Luxembourg, Netherlands, Poland, NORDIC, Russia, Turkey, and Rest of Europe

- Asia Pacific Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – India, China, South Korea, Japan, Malaysia, Indonesia, New Zealand, Australia, and Rest of APAC

- Middle East and Africa Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – North Africa, Israel, GCC, South Africa, and Rest of MENA

Market Scope and Segments:

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2018-2034 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2034 |

|

Historical Period |

2019-2022 |

|

Growth Rate |

CAGR of 13.1% from 2024-2034 |

|

Unit |

Value (US$ Billion) |

|

Segmentation |

Main Segments List |

|

By Application |

|

|

By Manufacturing Technology |

|

|

By Form |

|

|

By Region |

|

Frequently Asked Questions (FAQ):

The global polysilicon market size was values at US$ 12.3 billion in 2023 and is projected to reach the value of US$ 47.6 billion in 2034, exhibiting a CAGR of 13.1% during the forecast period.

The market is a global industry that produces high-purity silicon, a crucial component in solar panels and electronic devices. The growing demand for renewable energy and advanced electronics drives the market.

The Solar PV and Siemens Process segment accounted for the largest market share.

Key players in the polysilicon market include Wacker Chemie AG, Tokuyama Corporation, GCL-Poly Energy Holdings Limited, OCI Corporation, REC Silicon ASA, Daqo New Energy Corp., Hemlock Semiconductor Corporation, Jinko Solar, Mitsubishi Materials Corporation, LDK Solar Co., Ltd., Silicor Materials Inc., SunEdison, Inc., Sichuan Yongxiang Co., Ltd., KCC Corporation, Tianwei New Energy Holdings Co., Ltd. and Other Prominent Players.

The market is driven by the booming solar photovoltaic industry and increasing demand for semiconductors.

Select License Type

Select License Type