Phosphate Market Research, 2023

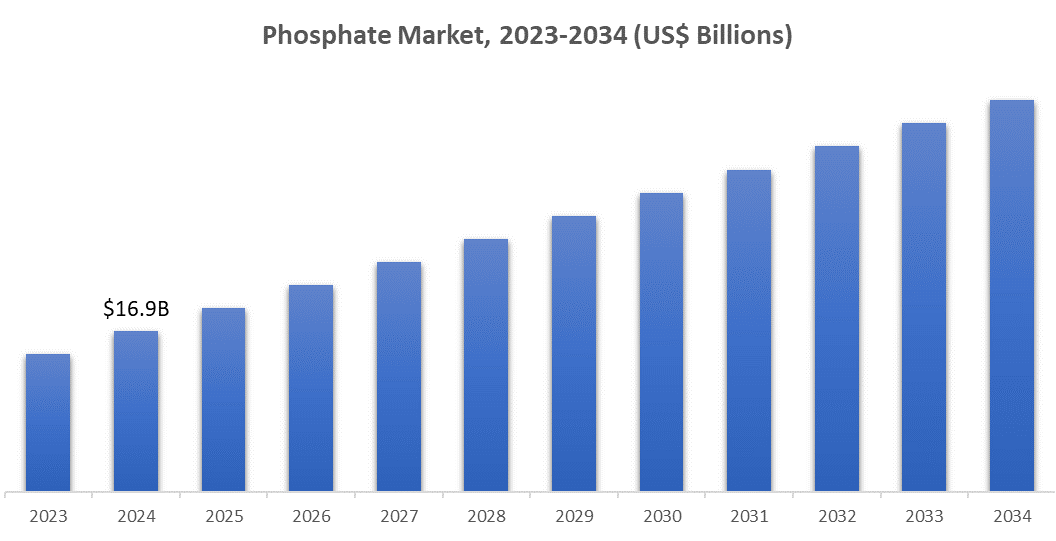

The global phosphate market is expected to grow at a CAGR of 3% during the forecast period from 2024 to 2034. The market size was valued at US$ 16.4 billion in 2023 and is projected to reach US$ 22.7 billion by 2034.

Phosphate is a vital inorganic substance composed of phosphorus and oxygen, typically obtained from naturally occurring phosphate deposits. It acts as an essential nutrient for the growth of plants and animals, significantly contributing to metabolic and energy transfer processes such as photosynthesis and ATP synthesis.

Phosphates are extensively used across diverse sectors, such as agriculture (as fertilizers), food and drink (as preservatives), water purification, and cleaning agents. General types consist of phosphoric acid, ammonium phosphate, calcium phosphate, sodium phosphate, and potassium phosphate. Attributed to their essential contribution to agricultural output, phosphates are vital for maintaining global food security, ranking them among the most traded commodities across the globe.

Market Highlights:

The market is fuelled by increased agricultural demand stemming from a growing global population and the necessity for improved crop yields. Governments and institutions are advocating for phosphate-based fertilizers to guarantee food security, while the increased use in water treatment, metal processing, and food preservation also boosts market expansion.

Moreover, improvements in mining and processing techniques, along with a rise in sustainable farming practices, are enhancing phosphate usage. Asia-Pacific and Africa's developing economies, featuring vast agricultural industries, offer profitable prospects. Future expansion will be driven by advancements in phosphate recycling and sustainable fertilizers, meeting strict environmental regulations.

Market Segmentation:

Ammonium phosphate dominates the market due to its vital role in agriculture as a high-nutrient fertilizer

The market is bifurcated based on the Type into Phosphoric Acid, Ammonium Phosphate, Calcium Phosphate, Sodium Phosphate, Potassium Phosphate, and Others. Ammonium phosphate dominates the market owing to the essential role it plays in the agriculture sector as a nutrient-rich fertilizer. Diammonium phosphate (DAP) and monoammonium phosphate (MAP) are renowned and actively used for their efficiency in improving soil fertility and boosting crop production.

Their cost-effectiveness, simplicity of use, and suitability for different soil types render them the favored option for farmers globally. The rising demand for high-yield crops to satisfy global food requirements, especially in Asia-Pacific and Africa, reinforces the prevalence of ammonium phosphate. Additionally, its use in industrial sectors, such as fire prevention agents, contributes to its market presence.

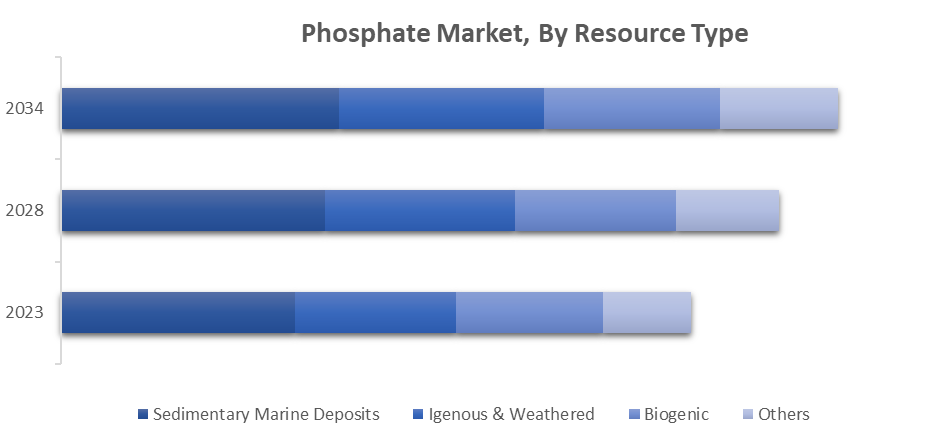

Sedimentary marine deposits are expected to dominate the market, as they account for the majority of phosphate rock reserves

The market is segmented based on the Resource Type into Sedimentary Marine Deposits, Igneous & Weathered, Biogenic, and Others. Sedimentary marine deposits have maintained a leading position in the market, constituting the bulk of global phosphate rock reserves. Widely located in regions such as Morocco, China, and the U.S., these reserves are simpler to extract and have elevated levels of phosphate minerals, resulting in cost efficiency.

These reserves are crucial for creating fertilizers such as DAP and MAP, which are important for farming. The ability of sedimentary deposits to scale up guarantees their ongoing prominence, bolstered by innovative mining methods and worldwide needs for food safety.

Source: Fatpos Global

Market Dynamics:

Growth Drivers

Growing Demand for Agricultural Productivity to Boost Market Growth

The world's population is rising rapidly, with a significant portion originating from South Asian and African nations, leading to an increased demand for greater agricultural production to satisfy food requirements, making phosphate-based fertilizers essential. These fertilizers improve soil fertility, encourage plant growth, and increase crop yields, tackling the issue of scarce arable land.

The creation of high-yield crop varieties that need extensive fertilization also accelerates phosphate usage. Developing countries in the Asia-Pacific and Africa are making significant investments in agriculture, resulting in a rise in demand. Moreover, governmental programs that encourage sustainable agricultural methods and food security enhance the utilization of phosphates, reinforcing their importance as a vital farming component.

Expansion of Industrial Applications to Create Expansion Opportunities

Phosphates are being used more often in water treatment to hinder scaling and corrosion in both municipal and industrial systems. Their involvement in producing flame retardants for textiles and construction has increased due to stricter safety regulations.

The food sector also fuels the demand for phosphates, employing them as preservatives to enhance shelf life and elevate food quality. Prepared foods and packaged items, particularly in advanced economies, have strengthened this trend. The adaptability of phosphate compounds in various industrial uses guarantees ongoing demand throughout different sectors.

Restraints

Resource Depletion and Limited Availability May Hinder Market Growth

The scarcity of high-quality phosphate rock poses a major obstacle for the market. Harvesting lower-quality deposits incurs higher costs and has a greater environmental impact, straining supply chains. Moreover, phosphate deposits are geographically centralized, with Morocco holding a significant portion, which makes global markets susceptible to geopolitical conflicts.

Concerns regarding sustainability due to extensive mining and the ecological effects of phosphate extraction have resulted in tighter regulations, raising operational expenses. These elements require advancements in recycling and the investigation of substitute resources, increasing the complexity of the phosphate sector's growth path.

Recent Developments

- Recently, The Mosaic Company launched its innovative Mosaic Biosciences platform. This global initiative integrates cutting-edge science and technology to enhance agricultural productivity. The platform's technologies focus on promoting crop health, supporting natural plant and soil biology, and maximizing yield potential.

- In 2024, Yara International announced the divestment of its fertilizer import and distribution subsidiary in Ivory Coast.

- Eurochem launched its Phosphate R&D Center in 2023. This facility enables prompt responses to site inquiries and client requests while reducing costs associated with developing and implementing new process technologies. Furthermore, Eurochem unveiled a state-of-the-art phosphate fertilizer production facility in Serra do Salitre, Brazil, in 2024.

- In 2023, Jordan Phosphate Mines Company (JPMC) signed a Memorandum of Understanding (MoU) with Sinokrot Poultry Farms and Saudi Poultry & Dairy Technology Trading Company. The partnership aims to establish a plant in Aqaba, producing phosphate feed additives with an annual capacity of 100,000 tonnes at a cost of JD 15 million.

Key Players:

- The Mosaic Company

- Yara International ASA

- EuroChem Group AG

- Jordan Phosphate Mines Company (JPMC)

- Nutrien Ltd.

- PhosAgro

- OCP Group

- ICL Group Ltd.

- Ma’aden (Saudi Arabian Mining Company)

- Innophos Holdings, Inc.

- Arianne Phosphate Inc.

- Groupe Chimique Tunisien

- Uralchem

- Sinochem Group

- KEMAPCO (Jordan-based chemical company)

- Other Prominent Players (Company Overview, Business Strategy, Key Product Offerings, Financial Performance, Key Performance Indicators, Risk Analysis, Recent Development, Regional Presence, SWOT Analysis)

Regional Analysis

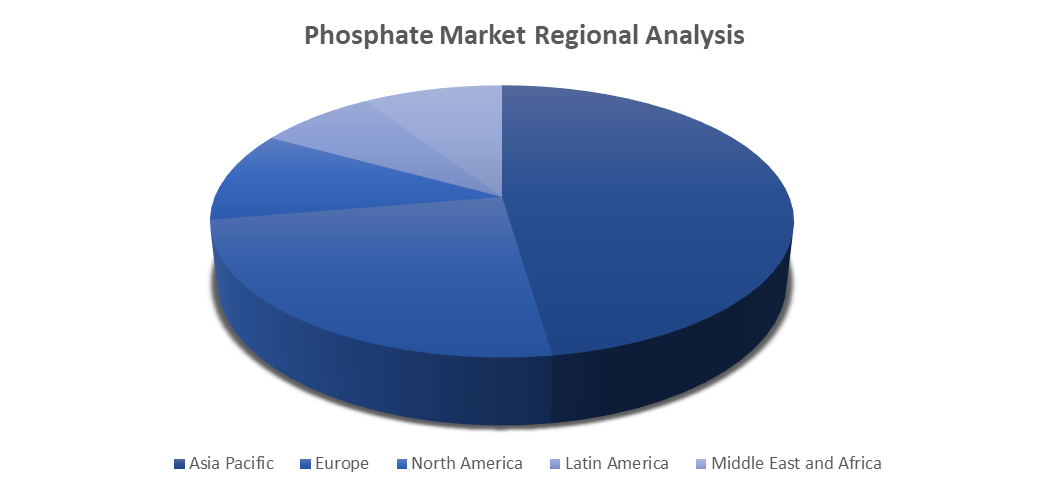

The global phosphate market is segmented based on regional analysis into five major regions: North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa.

The Asia-Pacific region leads the market attributed of its extensive agricultural foundation, swift industrial growth, and increasing fertilizer demand in nations such as China and India. Governments in the region are significantly investing in modernizing agriculture, establishing it as the top global consumer and producer of phosphates. The presence of extensive phosphate rock reserves in China enhances its dominance even more.

North America and Europe possess notable market shares owing to progressive farming techniques and strong demand for industrial phosphates. The Middle East and Africa represent growing markets, with Morocco at the forefront as a major phosphate rock provider.

Latin America has an increasing need for fertilizers in nations such as Brazil, but it remains less influential because of dependence on imports and restricted reserves.

Source: Fatpos Global

Impact of Covid-19 on the Market

The COVID-19 pandemic had a diverse impact on the market, owing to several supply chain disruptions, workforce shortages, and challenges regarding mining and production activities. Demand for fertilizer initially slumped due to logistical challenges in agriculture, but the recovery was rapid because of the sector's fundamental importance.

The use of industrial phosphate experienced a decline as sectors such as automotive and construction experienced a slowdown. Nevertheless, increased awareness of food security during the pandemic highlighted the essential role of phosphates, especially in fertilizers. Since the pandemic, the market has recovered, propelled by governments focusing on agricultural production and businesses adjusting to new supply chain frameworks.

Market is further segmented by region into:

- North America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United States and Canada

- Latin America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – Mexico, Argentina, Brazil, and Rest of Latin America

- Europe Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United Kingdom, France, Germany, Italy, Spain, Belgium, Hungary, Luxembourg, Netherlands, Poland, NORDIC, Russia, Turkey, and Rest of Europe

- Asia Pacific Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – India, China, South Korea, Japan, Malaysia, Indonesia, New Zealand, Australia, and Rest of APAC

- Middle East and Africa Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – North Africa, Israel, GCC, South Africa, and Rest of MENA

Market Scope and Segments:

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2018-2034 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2034 |

|

Historical Period |

2019-2022 |

|

Growth Rate |

CAGR of 3% from 2024-2034 |

|

Unit |

Value (US$ Billion) |

|

Segmentation |

Main Segments List |

|

By Type |

|

|

By Resource Type |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions (FAQ):

The global phosphate market size was valued at US$ 16.4 billion in 2023 and is projected to reach the value of US$ 22.7 billion in 2034, exhibiting a CAGR of 3% during the forecast period.

The phosphate industry encompasses the manufacturing, distribution, and marketing of phosphate-derived products, such as fertilizers, animal feed, and industrial uses. Phosphates are vital nutrients for plant development, and the market is fueled by rising global food needs and agricultural efficiency.

The Ammonium Phosphate and Sedimentary Marine Deposits segment accounted for the largest market share.

Key players in the global phosphate market include The Mosaic Company, Yara International ASA, EuroChem Group AG, Jordan Phosphate Mines Company (JPMC), Nutrien Ltd., PhosAgro, OCP Group, ICL Group Ltd., Ma’aden (Saudi Arabian Mining Company), Innophos Holdings, Inc., Arianne Phosphate Inc., Groupe Chimique Tunisien, Uralchem, Sinochem Group, KEMAPCO. and Other Prominent Players.

The market is driven by increasing global food demand, growing agricultural productivity, rising population, and limited availability of arable land.

Select License Type

Select License Type