Organic Electronics Market Research 2035

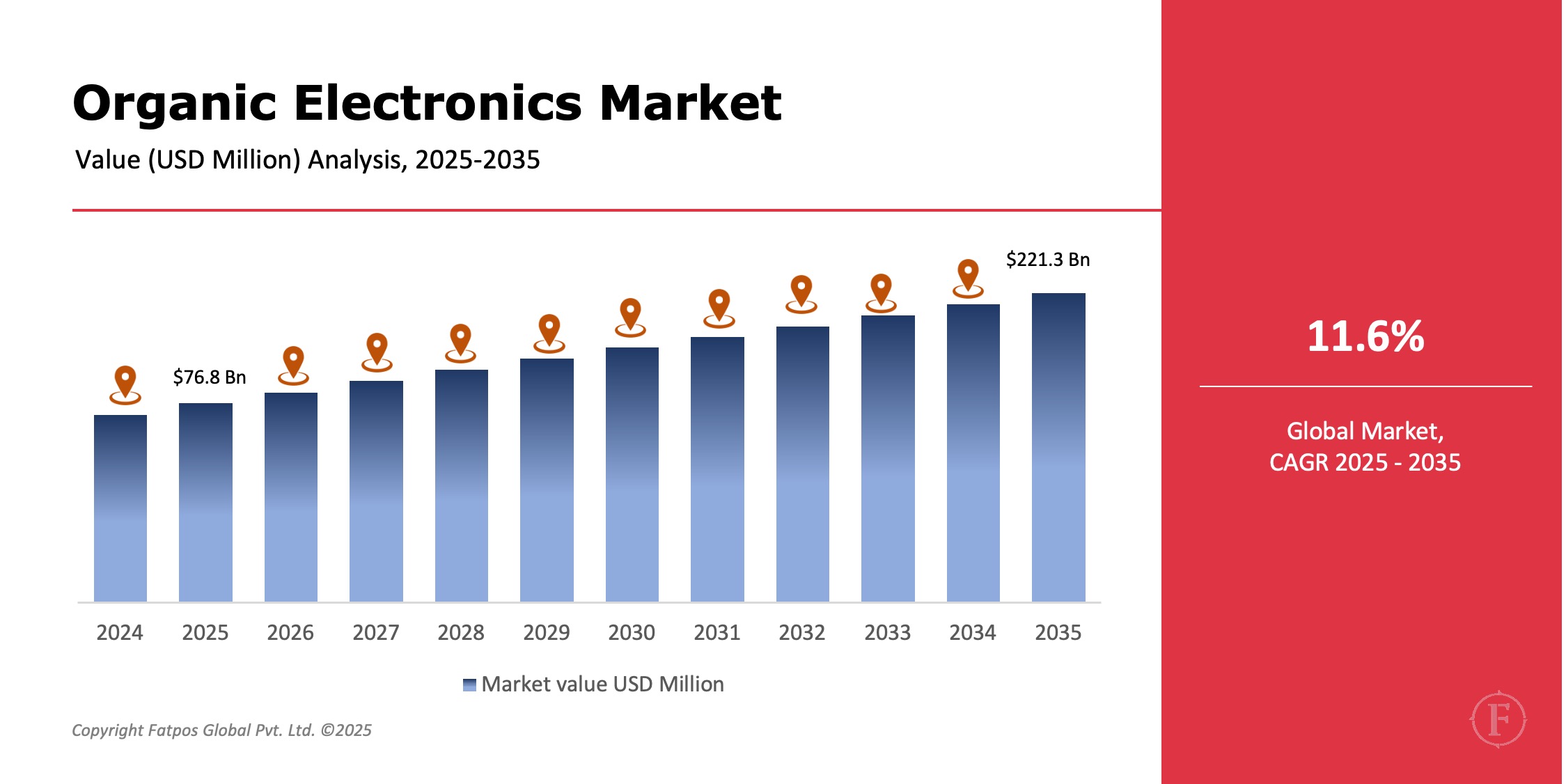

The Organic Electronics Market Size was USD 76.8 billion in 2025 and is projected to reach USD 221.3 billion by 2035, registering a CAGR of 11.6% . Demand arises for flexible, lightweight, energy-efficient devices, fueled by OLED displays, printed electronics investments, and applications in wearables, automotive, healthcare, and energy harvesting.

Unlike silicon, organic electronics use carbon-based conductive polymers and molecules, enabling flexibility, transparency, low-temperature processing, and cost-effective large-scale production. These innovations reshape next-gen electronics, enhancing portability, sustainability, and design versatility across industries.

Product Overview

Organic electronics feature diverse materials and devices based on organic semiconductors for charge transport. Key components include organic semiconductors as core functionals, conductive polymers for electrodes, antistatic layers, and sensors, organic dielectrics for low-power operation, and flexible plastic or polymer substrates enabling bendable designs.

Device types span OLED displays in smartphones, TVs, wearables, and automotive dashboards; energy-efficient OLED lighting panels; lightweight organic photovoltaics (OPV) for solar harvesting; organic sensors for biomedical, environmental, and wearable applications; and organic thin-film transistors (OTFTs) as essentials for flexible circuits. These advance flexible, efficient electronics.

Key Takeaways :

- The Organic Electronics Market is projected to grow at ~11.6% CAGR through 2035.

- OLED displays represent the largest device segment globally.

- Strong growth in wearables, automotive interiors, and healthcare electronics.

- Flexible and printed electronics are key technology enablers.

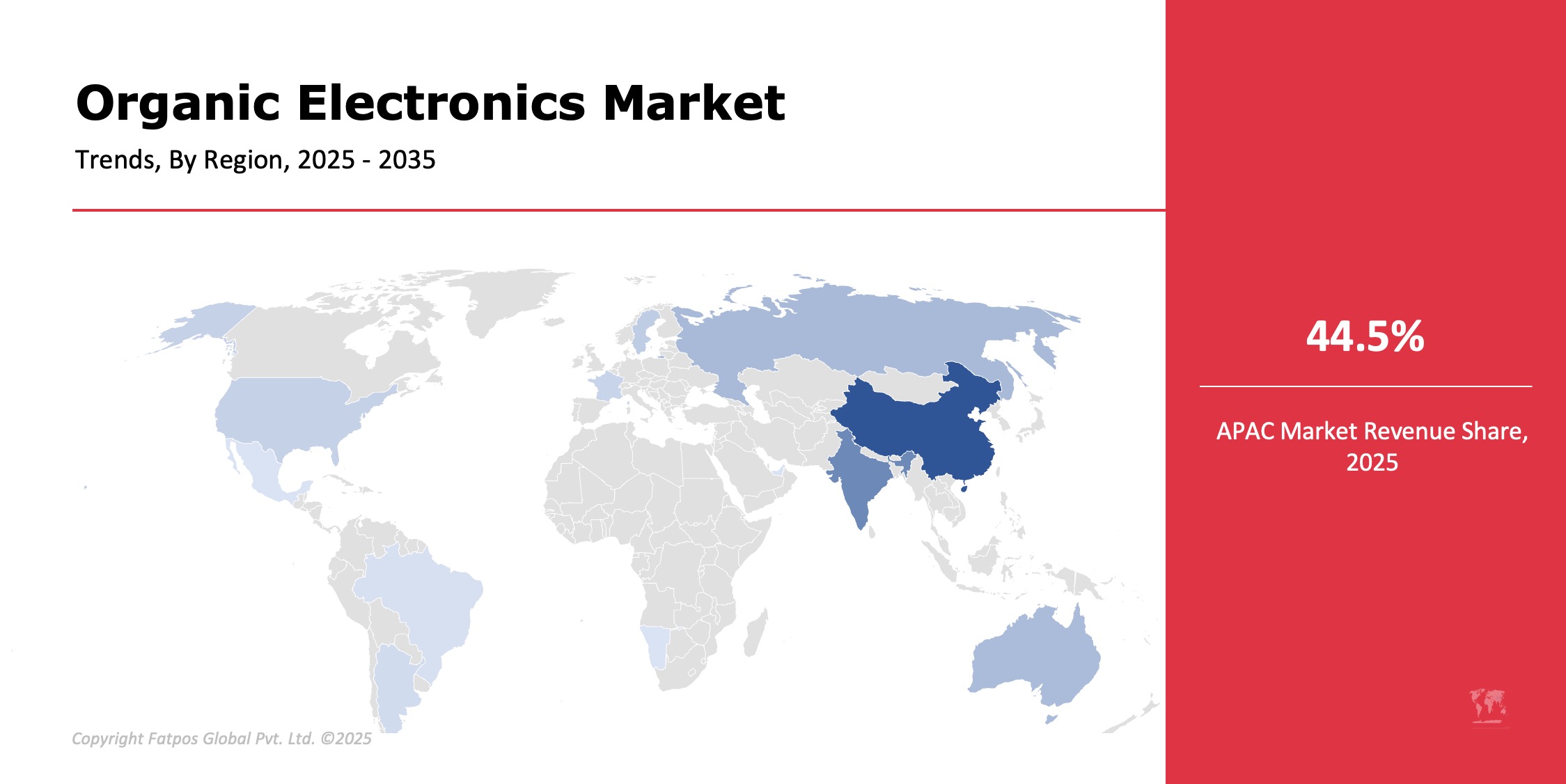

- Asia-Pacific leads in production and consumption due to electronics manufacturing hubs.

- Sustainability and low-energy processing are key long-term advantages.

Market Dynamics

Drivers

The organic electronics market thrives on rising demand for flexible, foldable, and lightweight electronics that prioritize portability and user comfort. Rapid adoption of OLED displays and lighting technologies drives growth, offering vibrant visuals, energy efficiency, and slim profiles for consumer gadgets.

Increasing integration in wearable and medical devices enables real-time health monitoring via biocompatible sensors. Advancements in printed electronics and roll-to-roll manufacturing slash costs and scale production. Automotive sectors fuel expansion with curved, flexible displays enhancing interiors and interfaces.

Restrictions

Organic electronics face key challenges that hinder widespread adoption. They exhibit lower performance and durability versus robust silicon-based counterparts, limiting use in high-stress applications. High research and development costs, coupled with expensive material synthesis, strain scalability and commercialization efforts.

Organic materials provide highly sensitive to moisture and oxygen, leading to degradation and shortened lifespans without advanced encapsulation. These hurdles demand ongoing innovation in stability, efficiency, and cost reduction to compete effectively.

Opportunities

Emerging trends propel organic electronics forward. Organic photovoltaics expand in building-integrated solutions, enabling seamless solar energy capture on facades and windows for sustainable architecture.

Smart packaging and IoT-enabled organic sensors grow, enhancing supply chain tracking, freshness monitoring, and real-time data via low-cost, disposable tech. Integration emerges in next-gen healthcare diagnostics and wearables for non-invasive, flexible monitoring.

Adoption rises in transparent and stretchable electronics, revolutionizing displays, skins, and conformable interfaces for immersive experiences.

Challenges

Key challenges in organic electronics center on enhancing material lifetime, efficiency, and stability against environmental factors like oxygen and humidity. Scaling production demands uniform performance across large areas via roll-to-roll methods without defects.

Competing with fast-evolving inorganic semiconductors requires breakthroughs in speed, power output, and cost parity to capture broader markets. Innovations in encapsulation, doping, and hybrid designs address these for viability.

Organic Electronics Market Trends

Organic electronics are experiencing transformative trends that accelerate market adoption and innovation. Rapid penetration of flexible and foldable OLED displays revolutionizes consumer electronics, enabling smartphones, tablets, and TVs with immersive, bendable screens that enhance portability and design aesthetics without compromising visual quality.

Increased use of printed organic electronics facilitates low-cost mass production through roll-to-roll processes, slashing manufacturing expenses and enabling scalable output for disposable sensors and smart labels. Development of stretchable and wearable electronic systems advances health monitoring, fitness trackers, and smart textiles, integrating seamlessly with human skin for continuous, comfortable data collection.

Rising interest in eco-friendly and recyclable materials addresses sustainability concerns, reducing e-waste via biodegradable polymers and carbon-based alternatives to rare-earth metals. Strategic collaborations between material suppliers and device manufacturers, such as partnerships between chemical giants and tech firms, streamline R&D, optimize supply chains, and expedite commercialization. These synergies foster breakthroughs in performance and affordability, positioning organic electronics as pivotal in IoT, automotive interfaces, and energy-efficient lighting, ultimately reshaping electronics toward flexibility, sustainability, and accessibility.

Key Players in the Global Organic Electronics Industry

- Samsung Display

- LG Display

- Universal Display Corporation

- Sumitomo Chemical

- Merck Group

- BASF SE

- AUO Corporation

- BOE Technology Group

- Heliatek

- Novaled GmbH

- OLEDWorks

- Royale Corporation

Regional & Country Analysis

North America spearheads organic electronics innovation through its strong R&D ecosystem, early adoption of OLED lighting and medical electronics, and the presence of leading technology innovators pushing boundaries in flexible devices. Europe prioritizes sustainability, focusing on organic photovoltaics for renewable energy, advanced automotive electronics, and robust government-backed research initiatives that foster eco-friendly manufacturing. Asia-Pacific commands as the largest and fastest-growing region, driven by South Korea, China, Japan, and Taiwan's dominance in large-scale OLED production and booming consumer electronics demand. Meanwhile, Latin America exhibits emerging adoption in consumer gadgets and smart packaging solutions, while the Middle East and Africa see gradual expansion fueled by smart infrastructure developments and renewable energy projects.

Segmentation Highlights

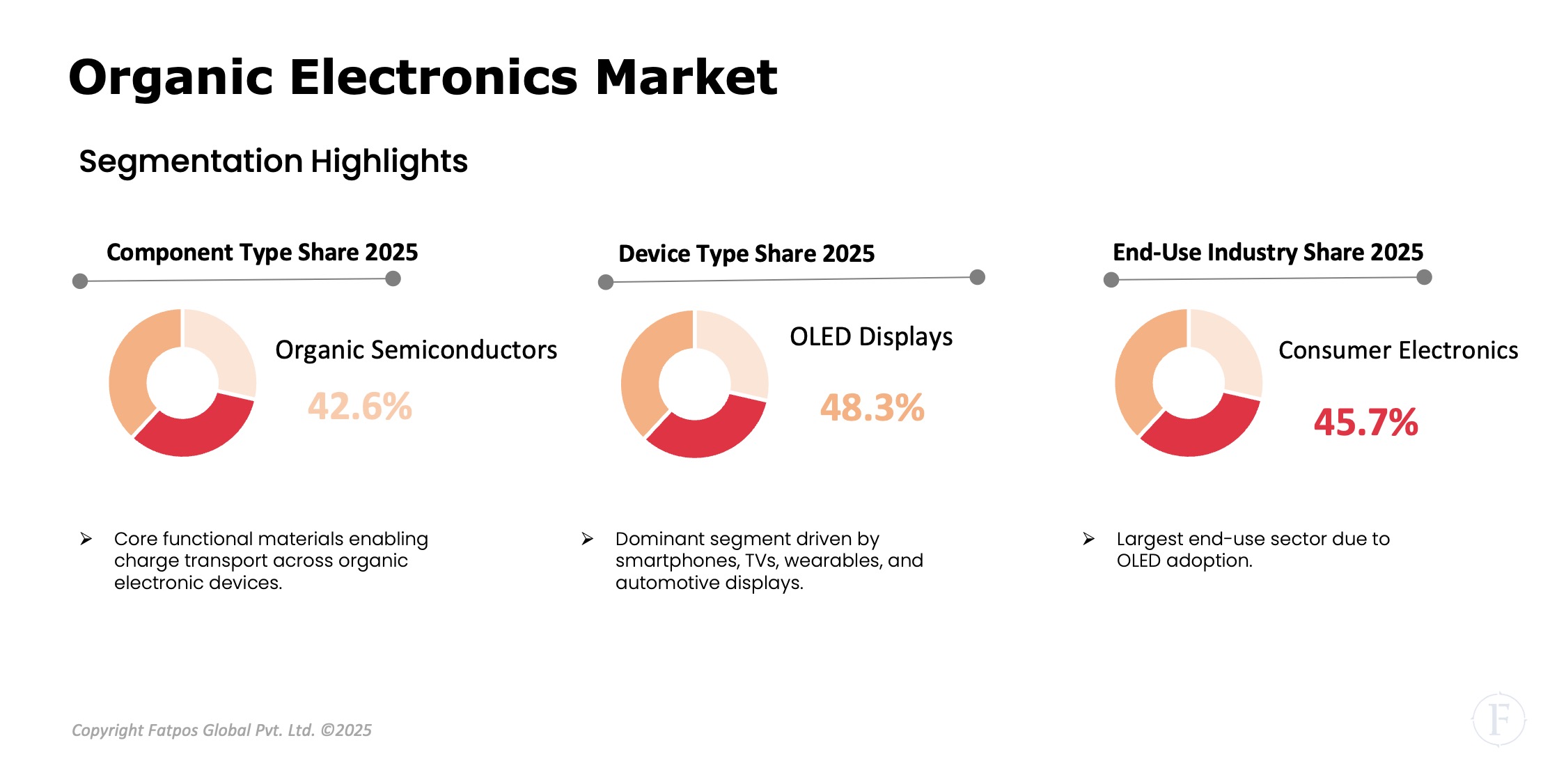

Organic semiconductors dominate the organic electronics market by component, serving as the core materials that enable charge transport and device functionality across various applications. Their versatility in conducting electricity while maintaining flexibility positions them as indispensable for next-generation electronics.

By device type, OLED displays command the largest market share, powering high-resolution screens in smartphones, TVs, and wearables, followed closely by OLED lighting for energy-efficient panels and organic photovoltaics (OPV) for lightweight solar solutions.

Applications are led by displays and consumer electronics, which account for the bulk of demand due to widespread adoption in portable gadgets. Consumer electronics remain the primary end-use sector, driven by demand for slim, vibrant devices, while healthcare exhibits robust growth potential through biocompatible sensors and diagnostic tools.

Report Key Elements

|

ATTRIBUTES |

DETAILS |

|

Study Period |

2019–2035 |

|

Base Year |

2024 |

|

Organic Electronics Market Forecast Period |

2025–2035 |

|

Organic Electronics Market Size by 2035 |

USD 221.3 Bn |

|

Market CAGR |

11.6% |

| By Component | Organic Semiconductors, Conductive Polymers, Organic Dielectrics, Substrates |

|

By Device Type |

OLED Displays, OLED Lighting, Organic Photovoltaics, Organic Sensors, Organic Thin-Film Transistors, Others |

|

By Application |

Displays, Lighting, Energy, Wearables, Healthcare, Automotive, Consumer Electronics, Others |

|

By End User |

Consumer Electronics, Automotive, Healthcare, Industrial, Energy |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Key Market Players |

Samsung Display, LG Display, Universal Display Corporation, Sumitomo Chemical, Merck Group, BASF SE |

Global Organic Electronics Industry Instances

- Smartphone manufacturers launched foldable OLED display devices.

- Automotive OEMs adopted curved OLED dashboards and interior lighting.

- Healthcare companies integrated organic sensors in wearable monitoring devices.

- Energy firms piloted organic photovoltaic panels for building-integrated solutions.

Analyst Review

As per our Organic Electronics Market analysis report, the market represents a transformative shift in electronics manufacturing toward flexibility, lightweight design, and energy efficiency. While durability and performance challenges remain, continuous innovation in materials science and manufacturing techniques is closing the gap with traditional silicon electronics. Companies investing in OLED expansion, printed electronics, and sustainable materials are expected to lead market growth through 2035

Frequently Asked Questions (FAQ):

Electronics based on carbon-based materials instead of silicon, enabling flexible and lightweight devices.

Demand for OLED displays, flexible electronics, wearables, and energy-efficient devices.

OLED displays.

Asia-Pacific.

Strong double-digit growth driven by innovation and expanding applications.

Select License Type

Select License Type