Graphene Electronics Market Research, 2035

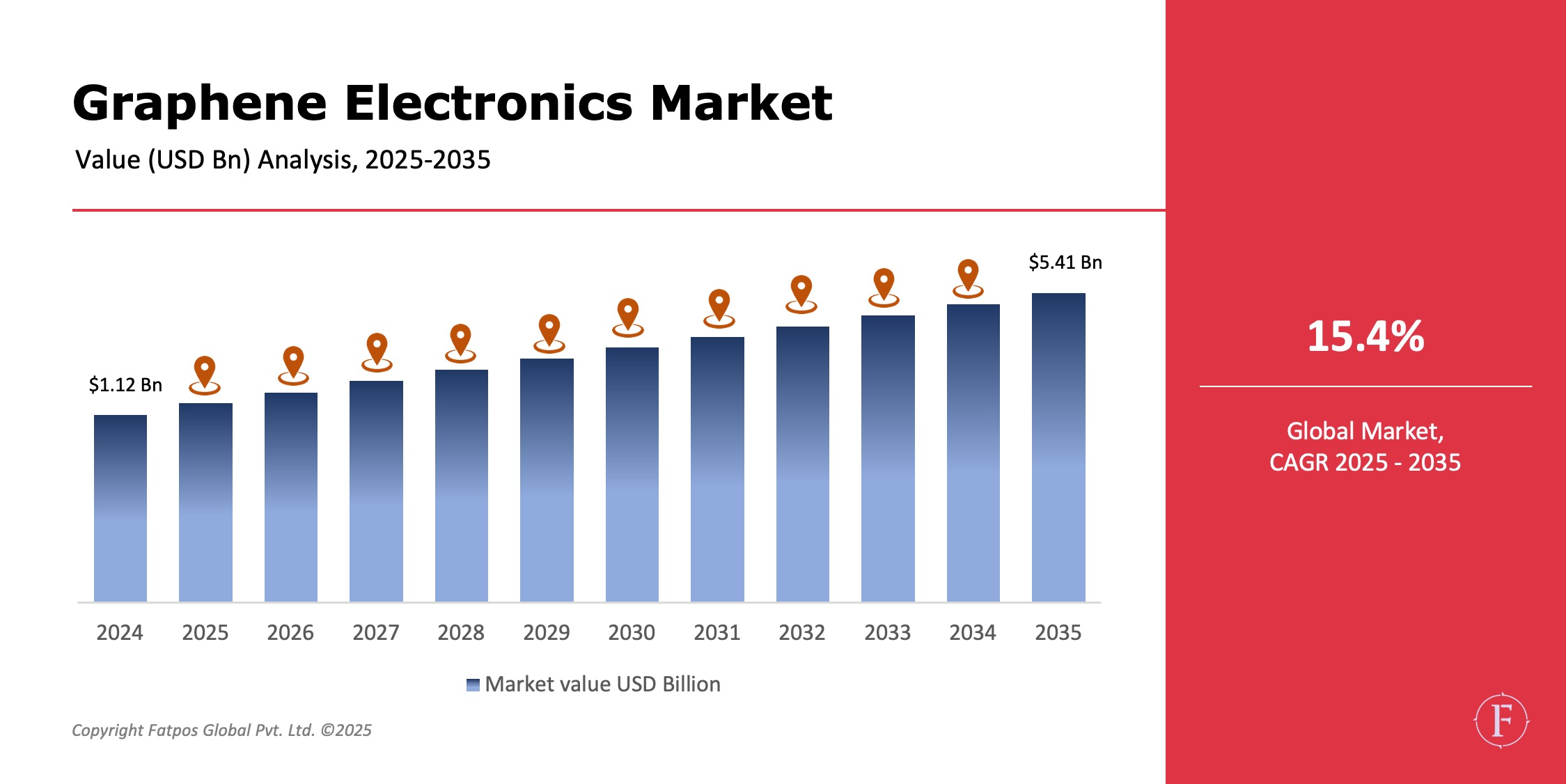

The global graphene electronics market is expected to grow from USD 1.12 billion in 2024 to USD 5.41 billion by 2035, reflecting a robust 15.4% CAGR, as industries seek materials with superior conductivity, strength, and miniaturization capabilities. The Graphene Electronics Market Growth is driven by substantial advancements in flexible electronics, fast‑charging batteries, and nano‑sensors is strengthened by advances in CVD and roll‑to‑roll production that accelerate commercialization across electronics, automotive, energy storage, and aerospace. Growth is further supported by national research funding, semiconductor modernization, EV development, and renewable energy storage programs in countries such as the U.S., China, Japan, Germany, South Korea, and the UK.

Product Overview

Graphene electronics use one-atom-thick graphene to deliver exceptional conductivity, transparency, flexibility, and thermal management for next‑generation devices. Graphene forms (GNP, GO, rGO) are used in sensors, transparent displays, flexible touchscreens, energy storage, photonics, and high‑frequency chips, enabling faster switching, higher efficiency, and lower heat. The industry is rapidly integrating graphene into EV batteries, wearables, smart textiles, thermal films, IoT hardware, and renewable‑energy systems, making it a key platform for long‑term electronic innovation.

Key Takeaways

- Market growth is rapid with ~15% CAGR forecast 2025–2035 as graphene transitions from R&D to early commercialization.

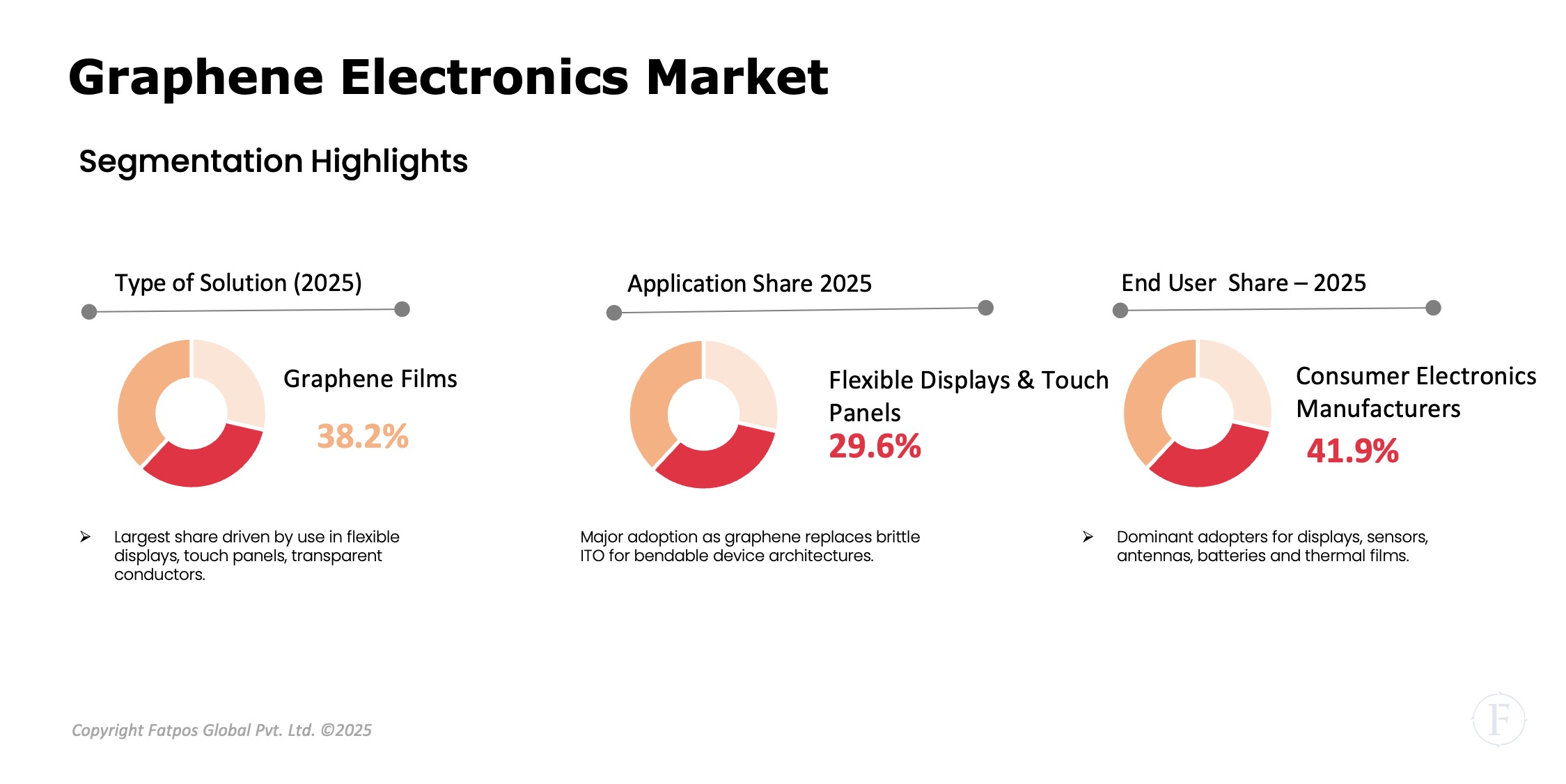

- Graphene films and printable inks command early adoption, particularly in touch panels, flexible displays and sensor interconnects.

- Wearables, flexible displays and sensors are the leading application segments due to demand for low-power, flexible, and transparent conductive layers.

- Thermal management and EMI shielding in automotive EVs and power electronics is an accelerating use-case for graphene fillers and composite films.

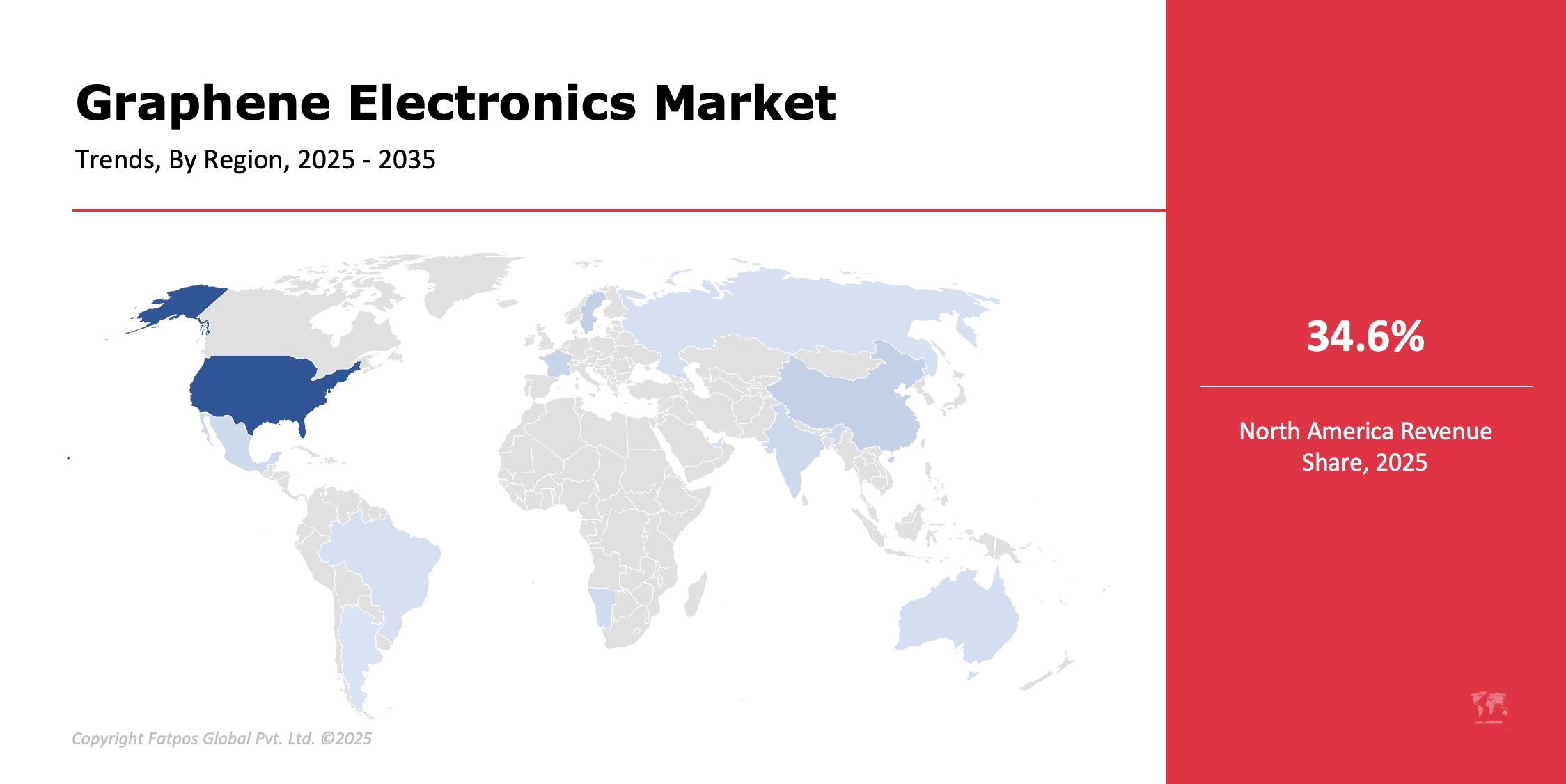

- Asia-Pacific and North America lead commercialization; Europe shows strong materials research and pilot manufacturing hubs.

Market Dynamics

Drivers:

Graphene’s ultra-high electron mobility and thermal conductivity help overcome ITO brittleness, copper interconnect heating, and limits of organic semiconductors. Its flexibility supports foldable phones, smart textiles, and wearables needing bendable conductors. In EVs, graphene-based thermal interface materials and sensors target power-electronics heat and reliability issues. Meanwhile, scalable CVD, roll-to-roll processing, printable graphene inks, and OEM–materials co-development are lowering cost, speeding qualification, and enabling production-scale adoption across multiple device platforms.

Restraints:

Manufacturing consistency and cost remain major hurdles, as producing large-area, low-defect graphene is still significantly more expensive than ITO, copper, or silver inks. Integration into existing CMOS flows is complicated by transfer-induced defects, adhesion issues, and the need to prove long-term reliability, slowing use in critical IC layers. Progress is further constrained by the lack of harmonized standards for graphene quality, characterization, and device qualification, which makes OEMs cautious in large-scale procurement decisions.

Opportunities:

Rising TPN demand in oncology, neonatology, geriatrics, and GI disorders offers strong growth. Critical care expansion in developing nations boosts premium electrolytes. Ready-to-administer IVs, customized blends, and sterile products add value. Military medicine, disaster response, home infusions, manufacturing automation, and sustainability initiatives expand market reach.

Challenges:

Graphene scaling hurdles persist: lab-to-production repeatability falters at square-meter scale with uniform specs. Supply chains suffer from variable graphite sources and growth conditions, causing material inconsistency. Emerging nanoparticle safety, lifecycle, and disposal regulations pose regulatory risks as adoption grows .

Graphene Electronics Market Trends

Graphene electronics are evolving around hybrid materials, scalable manufacturing, and closer OEM collaboration. Combining graphene with silver, copper, or conductive polymers helps balance cost, conductivity, and reliability, while roll-to-roll production and printable graphene inks support large-area, flexible devices and low-cost sensors. Co-design between material suppliers and device makers, alongside emerging standards for transparent conductors, thermal pads, and sensor stability, is accelerating commercialization and interoperability in graphene-based systems.

Key Players Featured in the Report

Our Graphene Electronics Industry report includes several leading manufacturers, such as:

- Samsung Electronics

- Huawei Technologies

- IBM Corporation

- Graphenea

- Haydale Graphene Industries

- Applied Graphene Materials

- ACS Materials

- Vorbeck Materials

- XG Sciences

- Talga Group

- AMO Graphene

Regional Analysis

North America leads with over 34% graphene electronics market share, driven by strong U.S. funding, advanced semiconductors, and industry–research collaboration, especially in consumer electronics and Defence. Europe ranks second, supported by the EU Graphene Flagship and commercialization in EVs, aerospace, and industry. Asia-Pacific grows fastest, led by China, Japan, and South Korea, while Latin America and Middle East/Africa emerge in energy storage, industrial uses, and early EV systems.

Segmentation Analysis

Graphene nanoplatelets dominate due to broad use in sensors, coatings, batteries, and conductive inks. Graphene oxide is rising in biomedical and environmental sensing, while reduced graphene oxide gains traction in energy storage and flexible, transparent electronics. Energy storage, sensors, and displays drive applications, led by consumer electronics, with strong growth in automotive, aerospace, energy, healthcare, and industrial manufacturing.

Report Key Elements

|

Report Key Elements |

Details |

|

Study Period |

2024–2035 |

|

Market Size by 2035 |

USD 5.41 billion |

|

CAGR |

15.4% |

|

By Type |

GNP, GO, rGO |

|

By Application |

Sensors, Displays, Batteries, Semiconductors, Photovoltaics |

|

By End-user |

Electronics, Automotive, Energy, Healthcare, Industrial, Aerospace |

|

By Region |

NA, Europe, APAC, LATAM, MEA |

|

Key Market Players |

Samsung, IBM, XG Sciences, Graphenea, and others |

Industry Instances

- Samsung filed breakthrough patents on graphene transistors for next-generation 5G/6G devices.

- Huawei introduced graphene-enhanced batteries for improved smartphone thermal management.

- Nanoxplore expanded high-volume graphene production facilities in Canada.

- XG Sciences partnered with EV battery manufacturers to commercialize graphene anodes.

- First Graphene collaborated with industrial manufacturers to integrate graphene into composite materials.

Analyst Review

The Graphene Electronics Market Analysis indicates strong multi-industry potential driven by semiconductor innovation, EV expansion, and demand for flexible electronics. Analysts note that companies investing early in graphene-enabled batteries, high-speed photonic chips, biosensors, and thermal management solutions will secure long-term competitive advantages. The long-term Graphene Electronics Market Forecast remains robust, supported by extensive R&D pipelines and government-backed commercialization programs worldwide.

Frequently Asked Questions (FAQ):

The market will reach USD 22.7 billion by 2035, growing at a CAGR of 6.3%

North America holds the largest share due to strong semiconductor infrastructure, research capabilities, and Defense applications.

Graphene batteries and energy storage systems show the highest growth potential due to EV and renewable energy demand.

High production cost, material quality inconsistencies, and integration challenges with traditional semiconductor fabrication lines.

Electronics manufacturers, nanomaterial producers, semiconductor companies, EV battery developers, researchers, investors, and government agencies.

Select License Type

Select License Type