Flexible Plastic Packaging Market Research, 2035

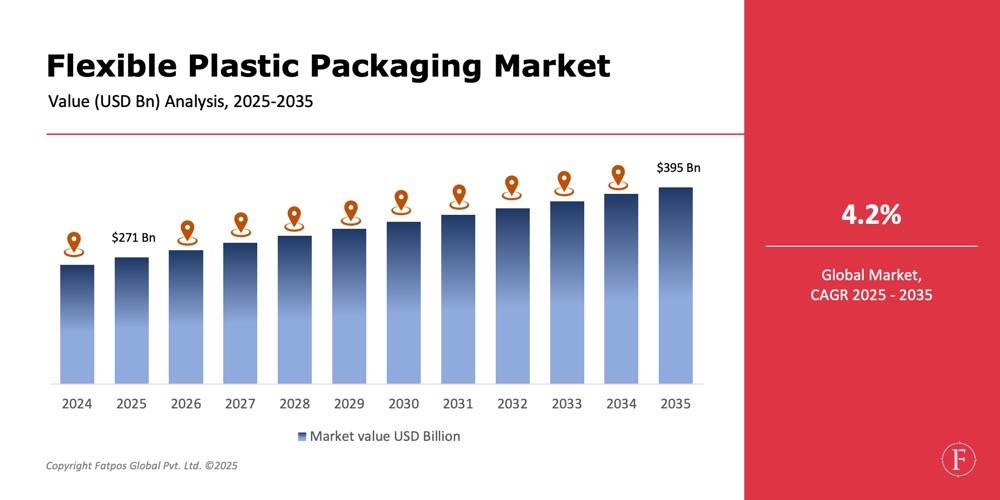

The flexible plastic packaging market is expected to grow from about USD 271 billion in 2025 to roughly USD 395 billion by 2035, at around 4.2% CAGR, driven by rising packaged food, pharma, e‑commerce, and on‑the‑go consumption. Demand is shifting toward pouches, high‑barrier films, and stand‑up packs, while Asia‑Pacific remains the largest and fastest‑growing region due to income growth, organized retail, and new converting capacity.

Product Overview

Flexible plastic packaging includes thin films, pouches, bags, wraps, and sachets made mainly from PE, PP, PET, and other engineered polymers. These formats offer strong barrier protection, reliable sealing, high-quality printing, and lower material use than rigid packs. They are widely used for snacks, dairy, beverages, frozen and pet foods, medicines, personal care, homecare, and industrial products. New pouch and film designs increasingly use mono‑material or “recycle‑ready” constructions, improving recyclability and helping brands and retailers meet circular‑economy and sustainability goals.

Key Takeaways

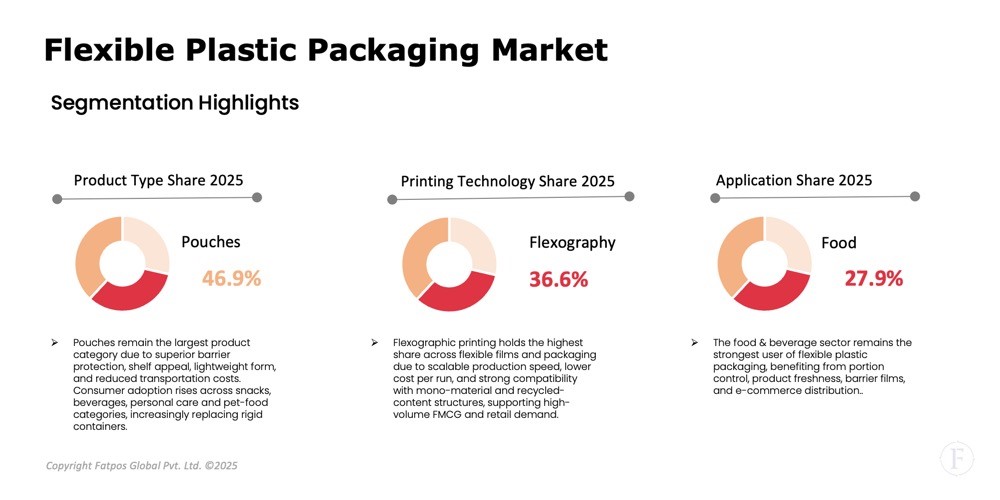

- Pouches hold the largest revenue share, driven by stand‑up and spouted formats in food, beverage, and home‑care uses.

- Food and beverages account for about half of global demand, especially snacks, ready meals, confectionery, and pet food.

- Asia‑Pacific leads both size and growth, supported by urbanization, FMCG and e‑commerce expansion

- Sustainability is reshaping product design, with recycle-ready mono-material laminates, higher recycled content and downgauged films becoming core innovation areas.

Market Dynamics

Drivers

The flexible plastic packaging market is propelled by demand for convenience foods, single-serve, and ready-to-eat products benefiting from light weight, extended shelf life, and tamper evidence. Growth in e-commerce prioritizes flexible formats for reduced shipping weight and damage. Innovations in multilayer films, reclose features, and digital printing enhance usability and customization.

Restraints

Flexible plastic packaging faces challenges from waste, litter, and recycling hurdles, particularly multi-material laminates lacking sorting infrastructure. Regulations on single-use plastics, EPR fees, and recycled content mandates raise compliance costs and spur material substitution. Petrochemical price volatility and limited high-quality PCR supply add cost and supply-chain risks

Opportunities

Sustainability drives flexible packaging innovation in mono-material PE/PP formats compatible with recycling, and chemical recycling used for food-grade applications like pet food and healthcare. Lightweight refill pouches reduce logistics costs and emissions. Smart packaging enhances product traceability, while emerging markets in South/Southeast Asia, Africa, and Latin America offer growth fueled by retail modernization and packaged goods demand.

Challenges

Key challenges include design trade-offs between recyclability, barrier and mechanical performance, particularly for oxygen- and moisture-sensitive products. Investment in new recycling technologies, EPR schemes and material standardization is still uneven across geographies.

Brand owners must balance cost, performance, sustainability claims and regulatory compliance, while converters face pressure to upgrade equipment for mono-material structures and digital printing without eroding margins

Flexible Plastic Packaging Market Trends

The flexible plastic packaging market is growing due to increasing demand for convenient, lightweight formats with extended shelf life that suit on-the-go consumption and e-commerce logistics. Innovations like multilayer barrier films, reclose features, and digital printing enhance functionality and customization. However, environmental concerns, regulatory pressures, and recycling challenges pose hurdles, especially for multi-material laminates. Sustainability trends are driving adoption of mono-material recyclable structures, chemical recycling, lightweight refill pouches, and smart packaging, while emerging markets in Asia, Africa, and Latin America offer strong expansion potential.

Key Players Featured in the Report

The global Flexible Plastic Packaging Industry includes several leading manufacturers, such as:

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Coveris

- Sonoco Products Company

- ProAmpac LLC

- UFlex Ltd

Regional Analysis

Asia-Pacific leads with 40–45% of global flexible plastic packaging share revenues, fueled by population growth, packaged food expansion, and manufacturing hubs in China, India, and Southeast Asia. North America drives innovation in sustainability and e-commerce formats, while Europe pushes recyclable mono-materials amid strict regulations. Latin America and MEA grow steadily via retail formalization, urbanization, and demand for snacks, beverages, and personal care.

Segmentation Analysis

Agricultural waste feedstock dominates due to abundance and efficiency; anaerobic digestion grows quickest for cost-effectiveness. Transportation leads end-use for low-carbon fuels, while industrial and power segments accelerate with grid integration.

Report Key Elements

|

Report Key Elements |

Details |

|

Study Period |

2025-2035 |

|

Market Size by 2035 |

USD 395 billion |

|

Market CAGR |

4.2% |

|

By Material |

PE, PP, PET, Others |

|

By Product Type |

Pouches, Films & Wraps, Bags & Sacks, Others |

|

By Printing Technology |

Flexography, Rotogravure, Digital, Others |

|

By End Use |

Food & Beverage, Pharmaceuticals, Personal Care & Cosmetics, Home Care, Industrial & Others |

|

By Region |

Europe, North America, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Market Players |

Amcor, Berry Global, Sealed Air, Mondi, Huhtamaki, Constantia Flexibles, others |

Flexible Plastic Packaging Industry Instances

- Amcor expands its AmPrima® mono-PE / mono-PP recycle-ready portfolio, compatible with chemically recycled content for food and healthcare application

- Amcor launches Liquiflex AmPrima bulk pouches in Europe, claiming up to 79% carbon footprint reduction versus some rigid formats.

- Berry Global increases the use of PCR polyethylene in European flexible films by over 30%, supporting customers’ recycled content targets.

- Berry Global & partners win a Gold Award for pet-food flexible packaging using ISCC PLUS-certified circular plastic.

- Brand owners such as Dole expand the use of recyclable stretch films and pouches to cut virgin plastic and improve recyclability in fruit supply chains

Analyst Review

As per our Flexible plastic packaging market analysis, the growth is steadily through 2035 via food security, packaged consumption, and e-commerce. Converters counter regulations with recycle-ready mono-materials and PCR, staying central to circular economy. Success demands recycling design, recycler collaboration, advanced materials, and agile digital printing

Frequently Asked Questions (FAQ):

The market is expected to grow from around USD 267.5 billion in 2025 to approximately USD 396.0 billion by 2035, reflecting a CAGR of about 4.0%, supported by demand from food, pharmaceuticals, personal care and e-commerce logistics.

Asia-Pacific is the largest and fastest-growing region, driven by population growth, urbanization, rising packaged food demand and strong converting capacity.

Pouches hold the highest revenue share among product types, with strong growth in stand-up and spouted pouch formats used across snacks, beverages, pet food and home care.

Food & beverage remains the largest and a key growth driver, while pharmaceuticals and personal care show above-average CAGR due to rising health awareness, hygiene focus and premium branding.

Converters, film and resin suppliers, FMCG and beverage brands, pharmaceutical and personal-care companies, retailers, e-commerce logistics providers, recyclers, investors, and policymakers seeking insight into material trends, sustainability pathways, competitive strategies and regional growth opportunities in flexible plastic packaging

Select License Type

Select License Type