Power Metering Market Research, 2034

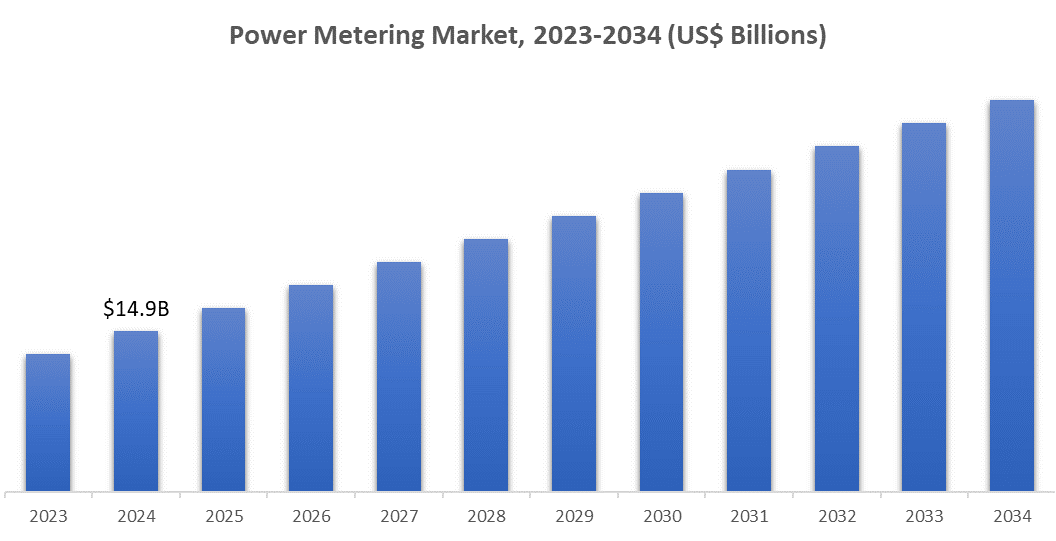

The global power metering market is expected to grow at a CAGR of 5.7% from 2024 to 2034, starting with a market size of US$ 14.1 billion in 2023 and projected to reach US$ 25.9 billion by 2034.

Power metering involves measuring and tracking electrical energy usage in real time, typically using devices such as smart, digital, and analog meters. Power meters measure energy consumption and supply information for billing, load management, and energy-saving. Modern power meters, especially smart meters, allow for interactive communication between utilities and users, promoting precise energy consumption tracking, remote supervision, and improved grid management.

Power metering is essential for energy management systems across residential, commercial, and industrial environments since it facilitates efficient energy use, lowers operational expenses, and reduces environmental impacts. The integration of digital and intelligent technologies makes power metering essential for updating power grids and improving energy efficiency.

Market Highlights:

The market is growing due to the rising demand for energy efficiency, digital infrastructure, and smart grid technology. Global regulatory policies require improved energy monitoring and conservation, promoting the application of sophisticated power meters, especially smart meters. These devices allow for real-time tracking and improve energy allocation, essential for integrating renewable energy sources such as solar and wind.

Moreover, digital transformation and IoT integration are propelling smart metering applications in industrial and commercial sectors, where efficiency and cost reductions are emphasized. The increasing demand for remote monitoring and operational effectiveness is propelling the market forward, with smart meter installations predicted to rise significantly until 2034.

Market Segmentation:

Smart meters lead the market due to their advanced functionalities and operational cost savings

The market is bifurcated based on the Type into Smart, Digital, and Analog Meters. Smart meters lead the market, holding over 60% of the total share all accredited to their advanced features, which include real-time data transmission, remote monitoring, and analytics on energy usage. These meters enable utilities and consumers to monitor energy usage, improve consumption habits, and identify several issues related to energy theft or equipment malfunction.

The capability to supervise and manage power distribution remotely through smart meters lowers the overall operational expenses for utility companies and improves grid efficiency. With the growth of smart grid infrastructure, smart meters have become crucial, especially in regions focusing on energy efficiency and the incorporation of renewable energy. Due to increasing demand in residential, commercial, and industrial areas, smart meters are anticipated to remain in a leading role in the years ahead.

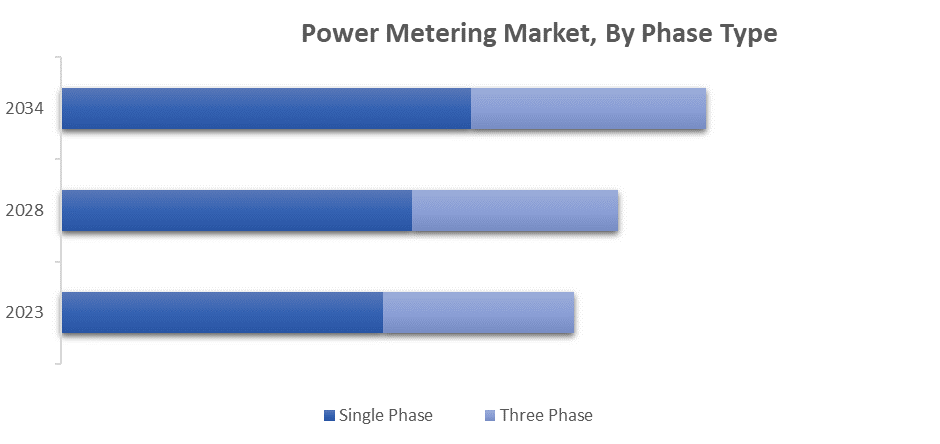

Three-phase power meters dominate due to their widespread use in high-load settings

The market is classified based on the Phase Type into Single-phase and Three-phase. Three-phase power meters are the leading segment, primarily because they are utilized in commercial and industrial environments that demand greater load capacity and stability. Three-phase meters are more suitable for heavy machinery, industrial equipment, and energy-intensive appliances, as they provide balanced power distribution and effective energy management.

Industries and sizable commercial structures frequently depend on three-phase power meters to assure dependable performance, minimize energy loss, and reduce any form of maintenance requirements. The need for three-phase meters is especially high in regions focusing industrial growth and digital advancement, as they facilitate operational efficiency and energy savings.

Market Dynamics:

Growth Drivers

Rising Demand for Smart Grids and Digital Infrastructure to Bolster Market Growth

In recent years, there has been a growing demand for smart grids and digital infrastructure, which has significantly boosted the demand for advanced power metering solutions, especially smart meters. Smart grids simplify immediate tracking, and managing, and improve the overall energy consumption, permitting utilities and users to boost energy efficiency and lower operating expenses. As countries are collectively shifting towards digital energy networks, smart meters are playing an essential role in leading this change by delivering accurate data, ensuring grid stability, and aiding decentralized energy systems.

Moreover, the combination of IoT and data analytics with power meters facilitates proactive grid control and quick fault identification, which is vital for extensive power systems and the incorporation of renewable energy, positioning smart meters as a key element in contemporary infrastructure.

Government Initiatives for Energy Efficiency to Propel Market Growth

Government policies and incentives that encourage energy efficiency and lower emissions are propelling the market forward. Several nations are implementing regulations that require the adoption of advanced metering infrastructure (AMI) to minimize energy waste and guarantee clear billing. Around the globe, governments are encouraging both consumers and businesses to embrace smart meters as part of wider sustainability and clean energy initiatives.

These policies are always focused on reducing overall electricity usage, reducing carbon footprints, and encouraging efficient energy consumption, thereby boosting the demand for digital and smart metering technologies. These initiatives not only facilitate the modernization of the grid but also enable consumers to make informed decisions based on data, thereby boosting energy conservation broadly.

Restraints

Lack of Standardization Across Regions May Hinder Market Growth

The lack of standardized regulations and technical standards for power metering internationally presents a major challenge for manufacturers and utility providers. Different compliance requirements infer that metering solutions need to be tailored to satisfy various regulatory and grid standards, enriching manufacturing complexity and expenses.

This inconsistency further complicates interoperability among meters from various suppliers, obstructing seamless integration in multi-vendor settings. Furthermore, utility companies might encounter setbacks in implementing advanced metering technologies if they have to adhere to varying regional regulations. Some regions are working on standardization initiatives, but until they are broadly embraced, this variety in regulations continues to obstruct the widespread and affordable implementation of advanced metering infrastructure.

Recent Developments

- Schneider Electric SE has launched an upgraded range of smart meters featuring enhanced cybersecurity for industrial applications. At Enlit Europe 2024, the company unveiled new Smart Grid Solutions to enhance grid resiliency, flexibility, and manage net-zero demands.

- Siemens introduced a smart metering solution integrated with IoT analytics for commercial and industrial sectors. The company acquired a technology firm specializing in data management for metering, bolstering its smart grid capabilities.

- ABB Ltd. expanded its digital metering portfolio with meters capable of integrating renewable energy sources. The company announced a joint venture to develop smart meters with enhanced connectivity for residential and commercial use.

- General Electric released a smart meter with advanced predictive analytics targeting utility and industrial sectors. The company partnered with a US utility to pilot an AI-based power metering system aimed at reducing grid energy loss.

- Eaton launched a series of digital power meters for industrial facilities, optimized for high accuracy and durability.

Key Players:

- Schneider Electric SE

- Siemens AG

- ABB Ltd.

- General Electric

- Eaton

- Honeywell International Inc.

- Itron Inc.

- Landis+Gyr

- Kamstrup A/S

- Aclara Technologies LLC

- Wasion Group Holdings Ltd.

- Sensus USA Inc.

- Elster Group GmbH

- Holley Technology Ltd.

- Echelon Corporation

- Other Prominent Players (Company Overview, Business Strategy, Key Product Offerings, Financial Performance, Key Performance Indicators, Risk Analysis, Recent Development, Regional Presence, SWOT Analysis)

Regional Analysis

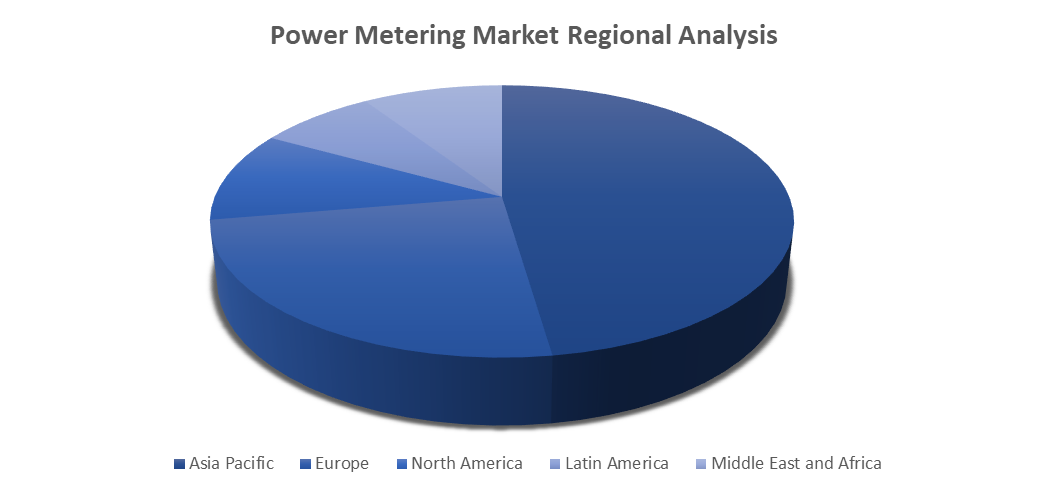

The global power metering market is segmented based on regional analysis into five major regions: North America, Latin America, Europe, Asia Pacific, and the Middle East and Africa.

The Asia-Pacific region leads the market, propelled by fast urbanization, industrial expansion, and the implementation of smart grid technology. China, Japan, and India are making significant investments in smart grid initiatives, focusing on improving the overall grid stability and energy efficiency. The robust drive for renewable energy incorporation in this region also facilitates advanced metering systems to manage decentralized energy resources. Government incentives and energy efficiency laws are further propelling market expansion, positioning Asia-Pacific as the largest and quickest-growing area in power metering.

North America and Europe on the other end are witnessing consistent growth in power metering, influenced by several regulatory policies focused on lowering carbon emissions and advancing smart grid technology. Both regions have been constantly focused on upgrading their infrastructure and embracing renewable energy, enhancing the demand for smart and digital meters.

Latin America, the Middle East, and Africa are developing markets for power metering, but growth is slower due to several infrastructure-related problems and reduced market penetration. Nonetheless, efforts to enhance energy access and efficiency suggest a slow rise in demand throughout these areas.

Impact of Covid-19 on the Market

The COVID-19 pandemic had a multifaceted impact on the market which resulted in several supply chains and postponing installation projects as a result of lockdowns and decreased workforce availability. The pandemic resulted in a drop in demand from commercial and industrial sectors as activities were suspended or reduced. Nonetheless, the rise in residential energy usage led utilities to focus on the installation of digital and smart meters for remote monitoring and advertising purposes.

With the recovery of economies, the importance of robust energy infrastructure and digital transformation in the post-pandemic era renewed interest in smart meters, particularly as remote monitoring became crucial. The market is currently experiencing a robust resurgence as smart metering facilitates achieving energy efficiency and sustainability objectives in the emerging, post-COVID energy environment.

Market is further segmented by region into:

- North America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United States and Canada

- Latin America Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – Mexico, Argentina, Brazil, and Rest of Latin America

- Europe Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – United Kingdom, France, Germany, Italy, Spain, Belgium, Hungary, Luxembourg, Netherlands, Poland, NORDIC, Russia, Turkey, and Rest of Europe

- Asia Pacific Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – India, China, South Korea, Japan, Malaysia, Indonesia, New Zealand, Australia, and Rest of APAC

- Middle East and Africa Market Size, Share, Trends, Opportunities, Y-o-Y Growth, CAGR – North Africa, Israel, GCC, South Africa, and Rest of MENA

Market Scope and Segments:

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2018-2034 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2034 |

|

Historical Period |

2019-2022 |

|

Growth Rate |

CAGR of 5.7% from 2024-2034 |

|

Unit |

Value (US$ Billion) |

|

Segmentation |

Main Segments List |

|

By Type |

|

|

By Phase Type |

|

|

By Application |

|

|

By Region |

|

Frequently Asked Questions (FAQ):

The global power metering market size was valued at US$ 14.1 billion in 2023 and is projected to reach the value of US$ 25.9 billion in 2034, exhibiting a CAGR of 5.7% during the forecast period.

The market includes devices, systems, and technologies that assess, track, and control electrical energy usage. It encompasses smart meters, advanced metering infrastructure (AMI), meter data management systems (MDMS), and energy management systems (EMS). Usage covers residential, commercial, industrial, and utility fields, promoting energy efficiency, live monitoring, and grid enhancement.

The Smart Meter and Three Phase segment accounted for the largest market share.

Key players in the global power metering market include Schneider Electric SE, Siemens AG, ABB Ltd., General Electric, Eaton, Honeywell International Inc., Itron Inc., Landis+Gyr, Kamstrup A/S, Aclara Technologies LLC, Wasion Group Holdings Ltd., Sensus USA Inc., Elster Group GmbH, Holley Technology Ltd., Echelon Corporation. and Other Prominent Players.

The market is driven by energy efficiency, smart grids, renewable energy, technological advancements, government policies, and rising energy demand.

Select License Type

Select License Type